Stanley Black & Decker (NYSE: SWK) is a tool-maker titan. It owns well-known brands DeWalt, Craftsman, Irwin, and LENOX, and, of course, Stanley and Black & Decker. But the stock has been in the doghouse. It's down 61.7% from its all-time high (reached in 2021) and up less than 21% from its 10-year low reached on March 19, 2020, during the height of the COVID-19-induced stock market plunge.

The sell-off may come as a surprise, since Stanley Black & Decker is a Dividend King with a 3.9% yield and 56 consecutive years of dividend raises. Dividend Kings tend to be reliable companies with growing earnings to justify steadily raising their payouts. Here's why the company could be under more pressure in the near term, but may ultimately be worth buying for patient investors.

Image source: Getty Images.

From record highs to a prolonged turnaround

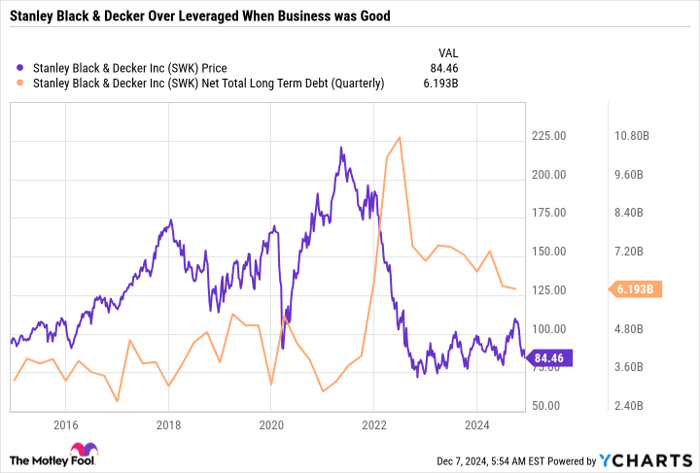

Stanley Black & Decker has been on a roller coaster in recent years. The COVID-19 pandemic caused an uptick in home improvement and do-it-yourself projects. Business soared for Stanley Black & Decker. The company got aggressive by taking on debt and making $1.9 billion in acquisitions in December 2021. As you can see in the following chart, Stanley Black & Decker's stock price and net total long-term debt peaked around the same time, highlighting the short-lived period of investor optimism.

Unfortunately, the pandemic-induced spike proved to be short-lived. In hindsight, the boom pulled forward sales in future years, rather than marking a new normal in demand. Overexpanded and overleveraged, Stanley Black & Decker was caught offsides when the cycle shifted into a downturn, resulting in negative cash flow. Over the last couple of years, the company has been implementing a cost-savings plan to get the business back on track. It even sold STANLEY Infrastructure in December 2023 to raise $760 million in cash to help pay down debt.

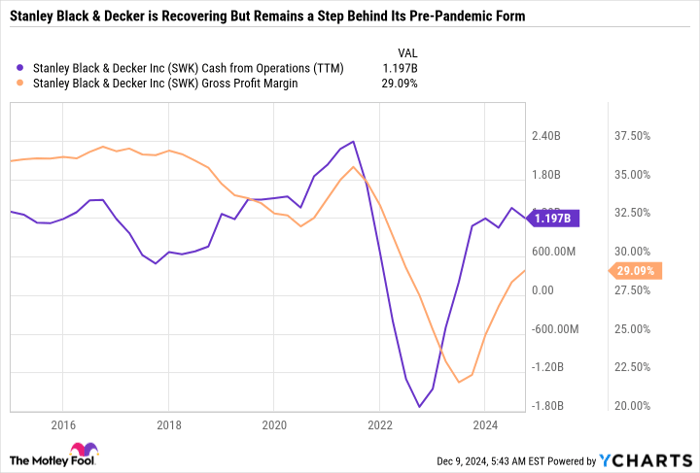

The recovery is going decently well so far. The following chart shows improvements in gross margins and operating cash flow. However, Stanley Black & Decker has fallen behind on its goal of reaching 35% gross margins, which has pressured the stock in recent months.

SWK Cash from Operations (TTM) data by YCharts.

On its third-quarter 2024earnings call the company reported 5% lower revenues than the same period in 2023, showcasing that demand remains weak. However, the company did say that it was on track for its expected $2 billion in pre-tax run-rate cost savings by the end of 2025. For context, it's currently at $1.4 billion in savings since implementing the program a couple of years ago.

Stanley Black & Decker's near-term goals may not go as planned

Stanley Black & Decker is recovering despite a difficult operating environment. But questions remain about how the company will reach its 35% gross margin by the end of 2025, even with the current cost savings plan. On the third-quarterearnings call Stanley Black & Decker CEO Donald Allan responded to an analyst question about the path toward margin improvement, highlighting the importance of lower interest rates:

I'd say what's really going to affect it probably as much or more than anything is at what pace do interest rates start taking effect. And how quickly does auto correct because that's a very profitable part of that Industrial business. And then how much fixed cost reduction activity will be able to both implement and complete in time for it to roll off the balance sheet next year.

Stanley Black & Decker is down 8.2% over the last month. A big reason for the further sell-off could be doubts about lower interest rates. During last week's Federal Reserve commentary, Chair Jerome Powell congratulated the economy's strength, but remarked that inflation was a little higher than expected. A strong economy is excellent overall news, but it could mean that the Fed will hold interest rates higher for longer or slow the pace of rate cuts. That would be bad news for rate-sensitive companies like Stanley Black & Decker.

Reasons to buy now

Despite the challenges, Stanley Black & Decker is a quality turnaround stock to buy now. The yield is 3.9%, a considerably higher yield than many other Dividend Kings'. Granted, Stanley Black & Decker has been making minimum one-cent-per-share per quarter dividend raises since 2021 just to keep its streak alive. Investors should expect Dividend Kings to raise their payouts at least 5% to 10% per year (depending on the company and whether the capital return program includes buybacks). But this is the right decision until the company gets back on track. The yield is already so high that dividend raises aren't the focus at this time.

What makes Stanley Black & Decker an exciting buy right now is the timeline of its turnaround. The stock price has gone practically nowhere for two years, and yet the company has made substantial progress on its turnaround during that time. If it hits its goals, its turnaround will be mostly complete in a year, but the company will still be far from the top of its game. Even so, its forward price-to-earnings ratio is 20.4. If Stanley Black & Decker can build upon that earnings growth in 2026, the stock could really start to look cheap.

Add it all up, and Stanley Black & Decker looks like a dividend stock worth buying -- but only for investors with at least a three- to five-year investment horizon, in case the turnaround takes longer than expected.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $356,125!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,959!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $499,141!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 9, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.