Skyworks Solutions, Inc. (SWKS), one of the largest suppliers of semiconductors to smartphone manufacturers, has been subject to criticism in the last few years because of its dependency on Apple, Inc. (AAPL).

Back in 2012, Apple accounted for less than 29% of total revenue reported by Skyworks, but in 2019, the contribution had increased to over 50%. Apple has a reputation for using its scale to reach favorable terms with its suppliers, and for this reason, many investors feared Skyworks might come under pressure from Apple, resulting in a decline in operating margins. Proving critics wrong, Skyworks has turned the tables by becoming Apple’s preferred chip supplier and is now playing an integral part in Apple’s success story.

Recent developments paint a very promising picture of what the future holds for Skyworks, and the stock remains undervalued despite reaching new highs following fiscal first-quarter earnings.

There is momentum behind the global smartphone industry

The growth rate for smartphone shipments has declined at a measured pace over the last few years, and experts seemed to agree on the fact that this industry was reaching a mature stage. The virus-induced recession dealt a massive blow on top of these structural developments, and global smartphone shipments dropped sharply in Q1 2020. Since then, however, the industry has bounced back along with the global economic recovery.

The industry received a boost from the launch of 5G-enabled devices in Q4, including the Apple iPhone 12. According to IDC estimates, Apple shipped 90.1 million iPhone devices in Q4, compared to just 73.8 million smartphones in the corresponding quarter in 2019. This stellar growth in shipments helped the company increase its market share of the global smartphone industry to 23.4% from 19.9% in Q4 2019. On cue, Apple reported a record revenue of $111.4 billion for the fiscal first quarter ended December 26, 2020, indicating the strong momentum behind its latest 5G-enabled devices.

Skyworks is well-positioned to report strong growth in earnings

Skyworks Solutions generates approximately 70% of its revenue from the mobile segment and Apple dominates this segment. Therefore, expected growth in global smartphone shipments will create a strong platform for Skyworks to report robust earnings growth.

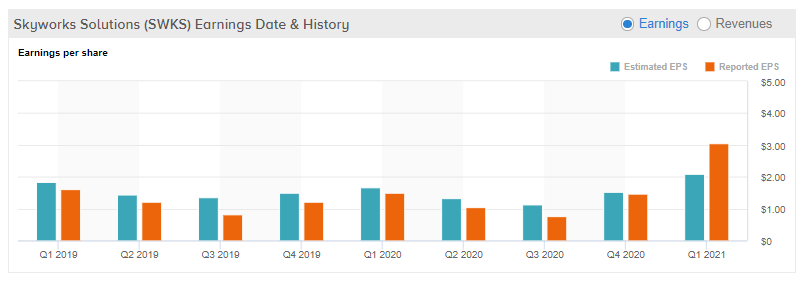

For the fiscal first quarter ended in December, the company reported record revenue of $1.51 billion, up over 69% year-over-year. This better-than-expected performance helped Skyworks beat analyst estimates by 60%, sending the stock to new highs as investors rewarded the company for its earnings momentum. This, in fact, is the most substantial earnings beat for Skyworks in recent history.

The 5G upgrade supercycle is expected to play out over the next three years, so it’s reasonable to assume that we are still in the very early stages of this macroeconomic development. Apple has already raised its forecasts for smartphone sales in 2021 because of the strong demand for its first-ever 5G device, and this is promising news for Skyworks investors. Factoring these expectations into their earnings models, Wall Street analysts have raised their earnings estimates by double-digits for the next quarter, which is a sign that the company has hit a sweet spot from an earnings perspective.

The earnings momentum will likely lift Skyworks Solutions stock to new highs in 2021, and the average analyst price target of $205.69 suggests 15% upside potential from current levels. What’s more, its Moderate Buy consensus rating breaks down into 13 Buys and 7 Holds. (See Skyworks Solutions stock analysis on TipRanks)

Positive revisions to this price target estimate are in the cards considering the company’s penetration into other high-growth business sectors.

Skyworks is expanding its horizons

The partnership with Apple is lucrative, but Skyworks remains focused on expanding its horizons to mitigate the risk of concentrating on a single large-scale smartphone manufacturer. Over the last few years, the company has successfully entered into partnerships with many other leading smartphone manufacturers including Samsung, Huawei, and Xiaomi. Additionally, all of these companies have grown exponentially as a result of their success in all-important emerging markets such as India. A diversified stream of revenue is important to secure the long-term sustainability of earnings, and Skyworks is moving in the right direction on this front.

On top of this, the company’s expansion into other business segments such as autonomous driving and Artificial Intelligence will be value accretive in the future as data-driven solutions are expected to dominate the world by 2030, leading to strong demand for the semiconductor manufacturing industry.

Takeaway

It is no secret that the 5G upgrade supercycle will help tech giants such as Apple, but the strong momentum behind semiconductor companies that are playing a vital role in this growth story remains underappreciated by the market. Skyworks Solutions, one of the leading smartphone chipmakers in the world, is trading at a forward earnings multiple of 20 in comparison to the sector average of 33.1, suggesting the stock is relatively undervalued. A careful evaluation of company prospects reveals Skyworks is well-positioned to grow along with Apple in the coming years.

Disclosure: The author is long Skyworks Solutions.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.