Disney DIS marked a significant milestone in its first quarter of fiscal 2025, with its streaming division achieving profitability as Direct-to-Consumer operating income reached $293 million, a substantial improvement from a $138 million loss in the prior-year quarter. The entertainment giant posted strong overall results, with revenues climbing 5% to $24.7 billion and adjusted earnings per share surging 44% to $1.76, demonstrating the success of its strategic initiatives despite subscriber fluctuations.

The streaming segment's performance reflects Disney's successful pivot from pure subscriber growth to profitability. Although Disney+ subscriptions declined slightly by 0.7 million to 124.6 million, average monthly revenue per paid subscriber increased 4% to $7.99, validating the company's pricing strategy. Meanwhile, Hulu showed robust growth with subscriptions rising 3% to 53.6 million, suggesting effective cross-platform synergies.

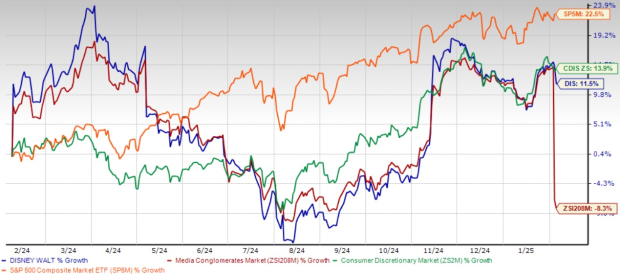

Strategic Initiatives and Growth Drivers of DIS

Disney's strategic moves, including the addition of an ESPN tile on Disney+ and various platform enhancements, demonstrate its commitment to improving user experience and content accessibility amid intensifying competition from incumbents like Netflix NFLX, Amazon AMZN-owned Amazon Prime Video and Apple AAPL-owned Apple TV+ in the streaming space. Management expects Direct-to-Consumer operating income to increase by approximately $875 million in fiscal 2025, indicating confidence in the streaming segment's continued profitability trajectory.

The Entertainment segment showed particular strength, with operating income increasing $0.8 billion to $1.7 billion, driven by improved streaming economics and strong theatrical performance from releases like Moana 2. The company's content strategy continues to resonate with audiences, as evidenced by successful theatrical releases and growing engagement across its streaming platforms.

However, the stock's 11.5% gain in the past year versus the Zacks Consumer Discretionary sector's 13.9% growth suggests much optimism may already be priced in.

1-Year Performance

Image Source: Zacks Investment Research

Near-Term Challenges and Considerations

Despite positive momentum, several factors suggest investors might benefit from patience in 2025. The company expects another modest decline in Disney+ subscribers in second-quarter fiscal 2025, while the Sports segment faces approximately $150 million in adverse impacts from college sports costs and the Venu Sports joint venture exit. The recent announcement of combining Hulu+ Live TV assets with fuboTV Inc. adds execution risk and potential integration complexities.

Additionally, the deconsolidation of Star India and the formation of a joint venture with Reliance Industries creates some uncertainty around international growth prospects. These structural changes may require time for investors to fully assess their impact on Disney's global strategy and financial performance.

Investors should carefully consider the company's substantial debt of $45.3 billion against a cash position of $5.48 billion, along with its premium valuation at 2.17X (3-year trailing 12-month P/S) compared with the Zacks Media Conglomerates industry's 0.93X.

DIS’ 3-Year P/S TTM Ratio

Image Source: Zacks Investment Research

Investment Thesis and Market Positioning

While Disney's long-term investment thesis remains compelling, current market conditions and ongoing transformational initiatives suggest better entry points may emerge throughout 2025. The company's unparalleled content library, strong brand portfolio, and improving streaming economics position it well for sustained growth, but near-term execution risks warrant careful consideration.

The company's guided high-single-digit adjusted EPS growth for fiscal 2025 and approximately $15 billion in expected cash from operations provide a solid foundation for long-term value creation. However, the ongoing evolution of the streaming landscape and competitive pressures may create opportunities for more attractive entry points.

The Zacks Consensus Estimate projects fiscal 2025 revenues of $94.78 billion, indicating 3.74% year-over-year growth, with earnings expected to increase 8.85% to $5.41 per share. These projections suggest steady but modest growth ahead.

Image Source: Zacks Investment Research

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

Strategic Recommendations for Investors

Investors considering Disney stock should focus on monitoring several critical aspects of the company's performance throughout 2025. Key attention should be paid to streaming subscriber retention and acquisition trends, which will indicate the success of Disney's pricing strategy and content appeal. Content engagement and monetization metrics will be crucial in assessing the effectiveness of Disney's programming investments and platform enhancements. The progress of integrating new strategic initiatives, particularly the Hulu+ Live TV combination with fuboTV, will be vital in evaluating execution capabilities.

Additionally, the impact of structural changes in international markets, especially following the Star India transaction, requires careful observation. While existing shareholders might maintain their positions given the company's strong fundamentals, new investors could benefit from waiting for more attractive entry points as Disney continues its transformation. The stock remains a compelling long-term investment, but timing and price discipline could enhance returns in the current environment.

Looking Ahead

Disney's strategic positioning in the entertainment landscape remains strong, with multiple growth drivers across its business segments. The company's focus on profitability over pure subscriber growth, combined with its robust content pipeline and strategic initiatives, suggests a promising future. However, investors might find better entry opportunities throughout 2025 as the company addresses near-term challenges and continues its transformation.

The key to successful investment in Disney stock may lie in patience and careful timing, allowing for a better risk-reward proposition as the company's strategic initiatives continue to materialize and the full impact of recent structural changes becomes clearer. Disney currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.3% per year. So be sure to give these hand picked 7 your immediate attention.

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Netflix, Inc. (NFLX) : Free Stock Analysis Report

The Walt Disney Company (DIS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.