What Is Depreciation Recapture?

Depreciation recapture is the process by which the IRS reclaims tax benefits previously obtained through depreciation when an investor sells a depreciable asset for more than its depreciated value. This excess amount is typically taxed as ordinary income.

It is a significant consideration for investors, as it can impact the tax liabilities and overall returns associated with the sale of depreciable assets.

The mechanics of depreciation recapture are not always straightforward. They depend on several factors, such as the type of asset, the method of depreciation used, and the length of time the asset was held.

The concept serves as a balancing act in the tax system, ensuring that the benefits of depreciation are equitably adjusted during the sale of an asset. Investors must factor in potential recapture taxes when planning their investment strategies and financial forecasts.

This knowledge enables them to make more informed decisions about when to sell assets and how to structure their investments. It's also essential for accurate tax planning, helping to avoid unexpected tax liabilities and optimize post-sale returns.

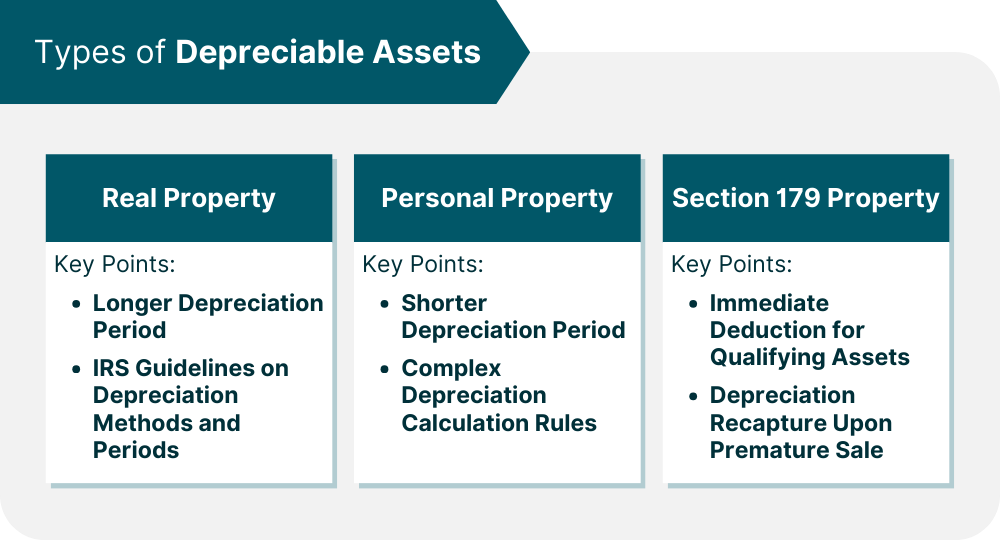

Types of Depreciable Assets

Real Property

Real property usually has a long depreciation period, reflecting its longer useful life. The IRS offers specific guidelines governing the depreciation of various real property types.

This includes recommended depreciation methods, recovery periods, distinctions between Section 1250 (real property) and Section 1245 (tangible personal property), and a mid-month convention.

Personal Property

Depreciation recapture of personal property refers to assets like equipment, machinery, and vehicles used in a business. Unlike real property, personal property usually has a shorter depreciation period, and the rules for calculating depreciation can be more complex.

Section 179 Property

Section 179 property refers to a specific category of depreciable assets subject to recapture under certain circumstances.

Traditional depreciation methods spread the cost of an asset's purchase over its useful life but Section 179 allows businesses to deduct the full cost of qualifying property in the year it is placed into service.

However, suppose a business later sells or disposes of Section 179 property before the end of its useful life and realizes a gain on the sale.

In that case, depreciation recapture rules come into play. The IRS will recapture a portion or all of the previously deducted Section 179 depreciation, and this recaptured amount is generally taxed as ordinary income.

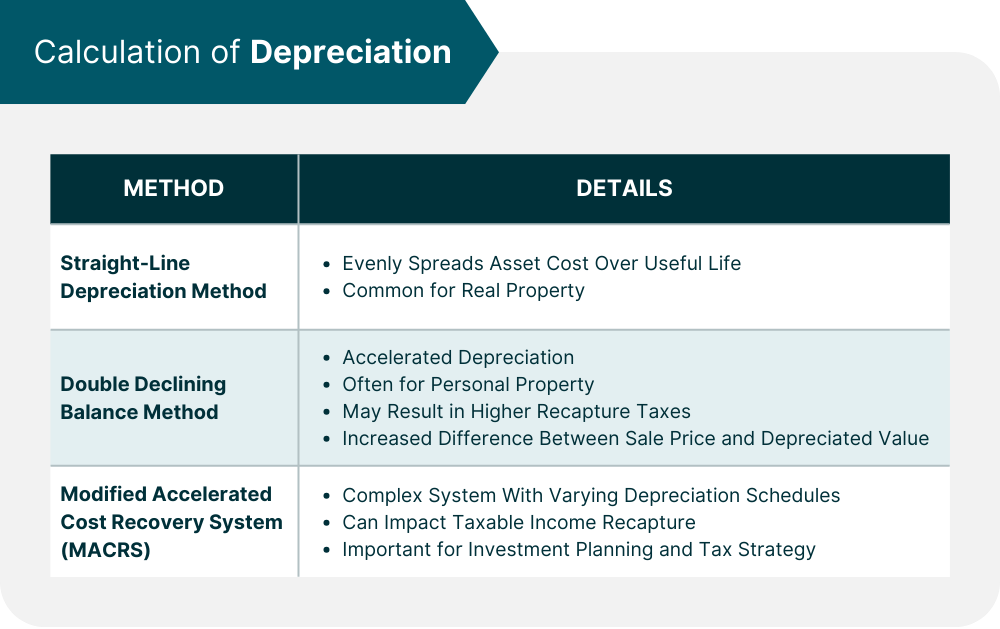

Calculation of Depreciation

Straight-Line Depreciation Method

The straight-line depreciation method evenly spreads an asset's cost over its useful life. This method is often used for real property, providing a consistent annual depreciation deduction.

However, when it comes to depreciation recapture, the simplicity of the straight-line method can lead to significant recapture taxes if the asset appreciates in value or is sold for more than its depreciated value.

Double Declining Balance Method

The double declining balance method is an accelerated depreciation technique that allows for larger depreciation deductions in the early years of an asset's life.

This method is often used for personal property, where the asset's utility and value decrease more rapidly.

While this method can provide substantial tax benefits initially, it also can lead to higher depreciation recapture taxes when the asset is sold.

The accelerated depreciation increases the difference between the sale price and the depreciated value, potentially leading to a larger taxable amount under the recapture rules.

Modified Accelerated Cost Recovery System (MACRS)

MACRS allows for greater depreciation deductions in the earlier years of an asset's life. It's a more complex system, involving different asset classes and varying depreciation schedules.

The choice of depreciation method under MACRS can significantly affect the amount of taxable income recaptured and should be considered carefully in investment planning and tax strategy.

Triggering Events for Depreciation Recapture

Sale of Depreciable Asset

When a depreciable asset such as property or equipment is sold for more than its adjusted book value (original cost minus accumulated depreciation), the IRS requires the difference to be reported as taxable income.

This process is designed to recapture some or all of the depreciation deductions the owner benefitted from during the asset’s life.

Business Asset Disposition

Disposition of business assets beyond just selling, can also trigger depreciation recapture. This includes asset trade-ins, involuntary conversions (e.g., loss due to theft or disaster), and cessation of business operations.

In such cases, the IRS treats the disposition as a sale, triggering depreciation recapture on any gains relative to the asset's depreciated value.

Conversion of Personal Property

When an asset's use changes, its depreciation calculation and tax treatment also change.

For example, if you convert a personal vehicle to business use, depreciation starts at the time of conversion, and any future vehicle sale can result in depreciation recapture.

Such conversions require meticulous record-keeping and adherence to IRS rules to track depreciation and subsequent recapture accurately. Failure to do so can lead to complex tax situations and potential disputes with tax authorities.

Depreciation Recapture Rates

Ordinary Income Tax Rate

The ordinary income tax rate is typically applied to depreciation recapture on most properties. This rate can be as high as 37%, depending on the taxpayer's income bracket.

It applies to the portion of the gain on the sale of a depreciated asset that's equivalent to the amount of depreciation claimed or claimable.

Applying the ordinary income tax rate to depreciation recapture can result in significant tax liabilities, especially for assets that have been substantially depreciated.

Investors and business owners must consider this potential tax burden when deciding to sell or dispose of assets.

Section 1250 Recapture Rate

Section 1250 of the IRS tax code pertains specifically to depreciation recapture on real estate properties, such as buildings or structures.

If a property depreciated using an accelerated method is sold for more than its depreciated value, the gain is taxed as ordinary income under Section 1250.

However, if the straight-line method was used, the recapture may be capped, potentially resulting in lower tax liabilities.

Section 1245 Recapture Rate

Section 1245 applies to the depreciation recapture on personal property, such as equipment, machinery, or vehicles used in a business.

Under this section, any gain from the sale of such assets is recaptured as ordinary income up to the total amount of depreciation taken.

Any gain exceeding the depreciated value is taxed as capital gains.

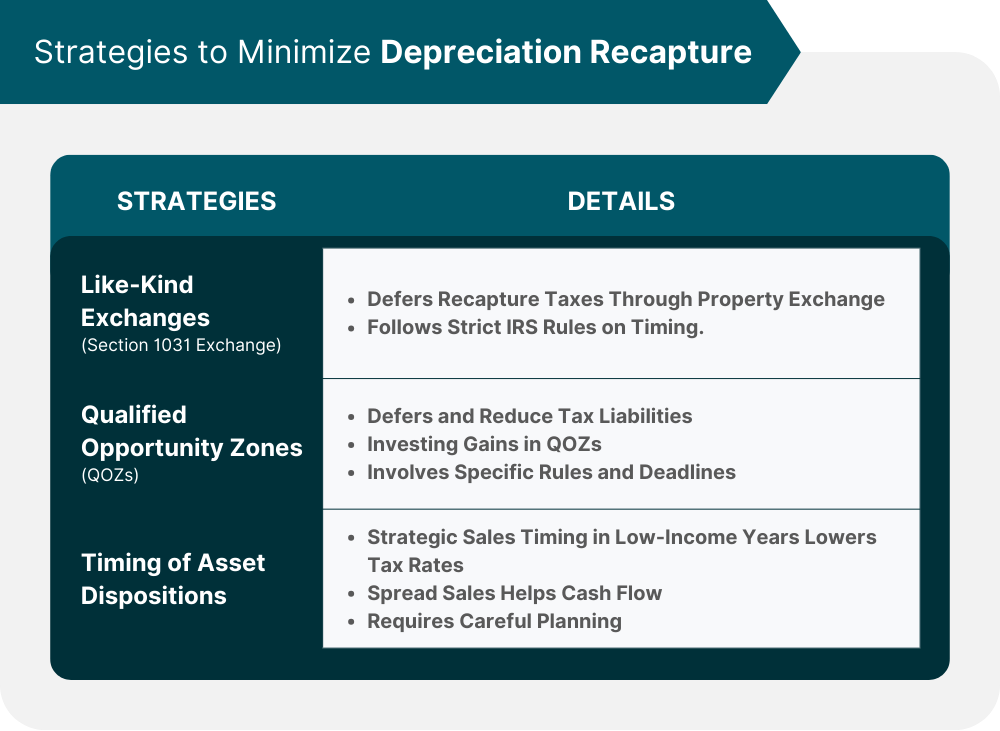

Strategies to Minimize Depreciation Recapture

Like-Kind Exchanges (Section 1031 Exchange)

Like-kind exchanges, also known as Section 1031 exchanges, offer a strategy to defer depreciation recapture taxes.

This provision allows an investor to exchange a property for another similar property without immediately incurring tax on the gain.

The deferred taxes, including any potential depreciation recapture, are rolled into the new property's cost basis. This strategy requires strict adherence to IRS rules and timelines.

Investors considering a 1031 exchange must identify the replacement property within 45 days and complete the exchange within 180 days of the sale of the original property.

Qualified Opportunity Zones (QOZs)

Investing in Qualified Opportunity Zones (QOZs) can also provide tax benefits that may help in minimizing depreciation recapture.

By reinvesting capital gains, including those from the sale of depreciated assets, into QOZs, investors can defer and potentially reduce their tax liabilities on those gains.

The QOZ program encourages long-term investments in economically distressed communities, offering staggered tax benefits over a period of up to ten years.

This strategy requires careful planning and understanding of the specific rules and deadlines associated with QOZ investments.

Timing of Asset Dispositions

Strategic timing of asset dispositions is another effective approach to manage potential depreciation recapture liabilities.

By planning the sale or disposition of assets in a year with lower overall income, investors and business owners can potentially benefit from lower tax rates.

Additionally, spreading out the sale of multiple depreciated assets over several years can help manage cash flows and tax liabilities more effectively.

This approach requires foresight and careful tax planning to align with broader financial goals and market conditions.

Conclusion

Depreciation recapture requires taxpayers to pay tax on the gain realized from the sale of a depreciable asset to the extent of prior depreciation deductions taken on that asset.

This mechanism is designed to recover the tax benefits individuals or businesses gain from depreciation deductions when they sell the asset for a profit.

Key triggering events for depreciation recapture include the sale of a depreciable asset, business asset disposition, and conversion of property.

The applicable recapture rates, determined by factors like the type of asset and the depreciation method used, can significantly impact tax liabilities.

Adopting strategies such as like-kind exchanges, investing in Qualified Opportunity Zones, and timing asset dispositions can help minimize the impact of depreciation recapture.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.