Credit: Shutterstock photo

Credit: Shutterstock photoBy BlackRock :

Written byBruce Wolfe, CFA&Russ Koesterich, CFA, JD

Today we are living through a profound shift in demography. Developed markets, along with China, are experiencing an unprecedented aging in their respective societies. This shift is impacting multiple dimensions of the global economy. In particular, aging populations are contributing to two of the defining characteristics of the current economic environment: slow growth and low interest rates.

Over the long term, economic growth is driven by two factors: increases in the labor force and productivity. Today, both are decelerating. While the drop in productivity is somewhat of a mystery, slow growth in the labor force is a direct result of demographic changes. Older individuals are less likely to be engaged in the labor force and today there are more of them.

Demographics are also contributing to the low interest rate environment. This is in part a side effect of slow growth, but demographics also affect rates through changes in consumption patterns. Older individuals borrow less and save more. As households approach retirement, they also tend to shift towards more conservative investments, in the process increasing demand for bonds and other income-producing assets. The net effect is that older populations tend to be associated with a lower real-interest rate environment.

For investors and policy makers, these changes represent both a challenge and an opportunity. Arguably, the biggest policy debate today is how to accelerate economic growth. Indeed, after the U.S. election , investors began anticipating a significant uptick in growth stemming from new U.S. fiscal policies along with tax and regulatory reform initiatives. Whether the growth occurs remains to be seen, but regardless, it is important to note that the dynamic of the changes brought by an aging population is a long term - and global - phenomenon that will maintain critical importance for some time.

In the meantime, much of the debate over growth focuses on productivity, arguably a more difficult problem to solve. Conversely, accelerating the rate of growth in the labor force is relatively straightforward. At a time when immigration is becoming an increasingly contentious topic, getting more older citizens to extend their working life, along with increasing female participation, may be the single, simplest prescription for addressing the problem of slow global growth.

The elderly shall inherit the earth

Recent economic and market history has been distinguished by extraordinary events: the Great Recession, the bursting of the housing bubble and record low interest rates. But while these events are unusual, they are not without precedent; there have been other housing bubbles and economic contractions. However, one of the underlying causes of recent economic conditions is truly unique: a rapidly aging population, a result of increased longevity, slowing birth rates and lower childhood mortality.

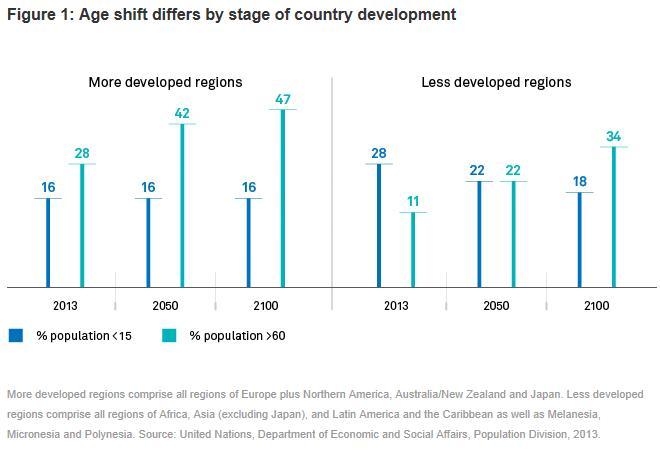

The graying of the population in developed countries is without precedent in human history. While most developing countries outside of China can look forward to a demographic tailwind for many years, developed countries are rapidly aging (see Figure 1). According to estimates by the United Nations, between 2015 and 2030, the number of people in the world aged 60 years or over is projected to grow by 56%, from 901 million to 1.4 billion. The number of people aged 80 years or over, the "oldestold" persons, is growing even faster. Projections indicate that in 2050 the oldestold will number 434 million, having more than tripled in number since 2015, when there were 125 million people over age 80. 1

Economic atrophy

In addition to longevity, there are other trends driving demographic changes. More people are remaining unmarried and living alone. According to the U.S. census bureau, the percentage of one-person households in the U.S. increased from less than 15% in 1960 to nearly 30% today. Those that do decide to get married are having smaller families. Average children per U.S. household for married couples has fallen from roughly 2.5 in 1965 to under 2 today.

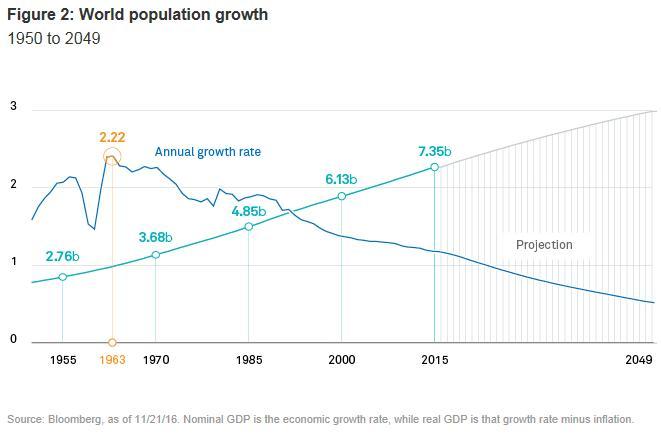

Nor is this simply a U.S. phenomenon. In other parts of the developed world, particularly Europe, the trend towards fewer and later marriages coupled with a declining birthrate is even more pronounced. The net effect is a dramatic drop in population growth, a trend that has been in place for many decades. In 1963, global population growth peaked at 2.22%. At current projections, by 2100, the rate is expected to decline to 0.1% (see Figure 2). 2

While changes in birthrates and household formation are a slow-moving phenomenon, in recent years, these trends have started to catch up with the labor market. The delayed effect of slower population growth is now contributing to a secular decline in labor force growth. This trend, along with a decade-long slide in productivity, explains much of the economic stagnation that has bedeviled policy makers, politicians and investors.

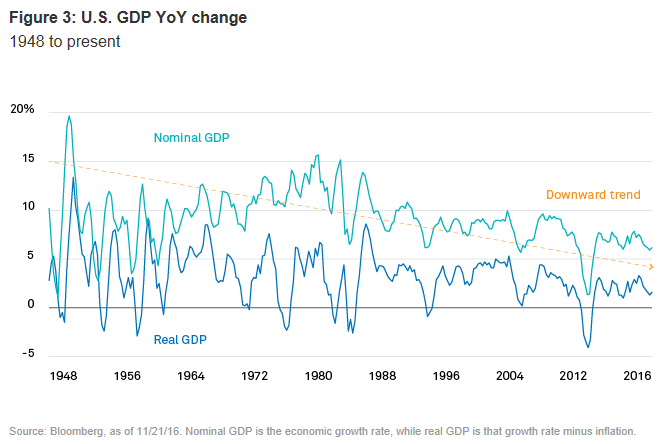

The trend towards slower growth in the labor force is not only a function of fewer individuals entering the labor force but also of more individuals retiring. The drop in work force participation, measured as the percentage of the population engaged in the labor force, has closely mirrored the aging in the population. Relative to the 1960s and 1970s, when baby boomers were starting to enter the work force in significant numbers, and the 1980s and 1990s, when female participation was on the rise, labor force growth has slowed dramatically. This slowdown has coincided with the general deceleration in economic growth (see Figure 3).

Lend more, borrow less

Beyond slow growth, the other defining characteristic of the post-crisis environment is the persistence of historically low interest rates. This is partly a function of central bank policy, but it is important to highlight that central banks are reacting to as much as driving the rate environment.

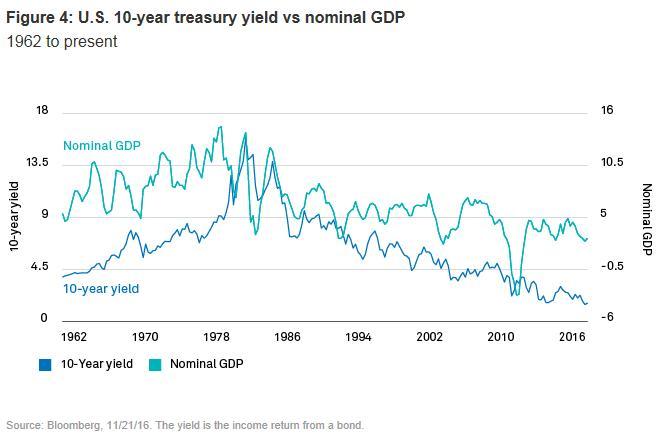

The low rate environment makes more sense when viewed through the prism of nominal growth (NGDP). Since 1962, the level of nominal GDP has explained roughly 35% of the variation in U.S. long-term rates, with each additional point of NGDP associated with roughly a 0.50% increase in interest rates (see Figure 4). To the extent an aging population has contributed to slower growth in the work force, which in turn has coincided with a slowdown in overall growth, low rates are a natural extension of this trend.

However, while low NGDP suggests a low rate regime, it cannot fully explain why interest rates remain above but not far off multi-decade lows. There are several contributing causes, including the aforementioned central banks, a dearth of bonds and growing institutional demand for income. But aside from these factors, demographics are most likely impacting rates through changing household consumption patterns, also partly a function of an aging population.

As individuals age, their economic behavior changes. Younger households smooth lifelong consumption by borrowing more. In comparison, older individuals borrow less as they pay down debt and downsize their homes. In addition, as individuals approach retirement, they tend to shift their asset allocation towards bonds, which pushes prices higher and yields lower.

While these behaviors have been evident for many decades, today there is still another reason why older individuals are saving more: rising longevity, or the expectation thereof. A recent paper by the San Francisco Federal Reserve documented the downward pressure on real rates as households build up their savings in anticipation of longer retirements. 3

In theory, at least, an increase in longevity should mean investors make a greater allocation to equities in their retirement years than traditional practices dictated. This, in turn, would reduce some of the demand for bonds and take some pressure off of prices. But that either has not occurred, or it is not showing up in the data so far.

Not dead yet

Persistent slow growth has already contributed to political upheaval and the rise in populism in both Europe and the United States. Combating this trend is a growing concern for both politicians and policy makers. To date much of the policy debate has focused on productivity. The hard truth is that raising productivity is difficult.

Given the long-term shift towards a service-, and now sharing-, based economy, it is not even clear that we are measuring productivity correctly. Given that growth potential is both a function of productivity and growth in the labor force, it may be more fruitful to shift the debate towards mechanisms that will accelerate growth in the labor force.

Unfortunately, the rate of new workers was set decades before by the birth rate. That said, governments can still influence work force growth through several channels, including immigration as well as raising the participation rate among existing citizens.

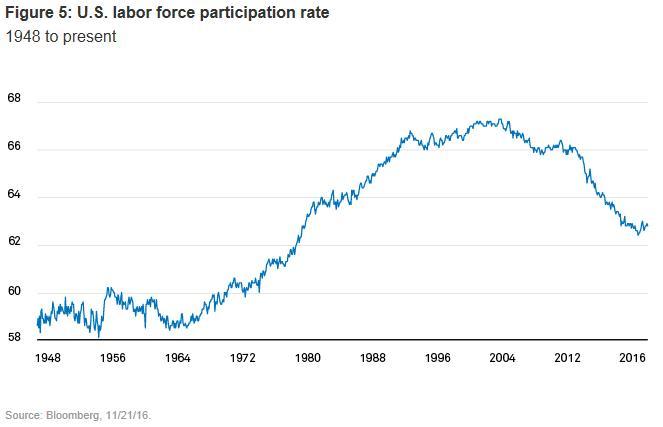

But with the exception of a few countries such as Canada and Australia, immigration is increasingly a non-starter for political reasons. That leaves raising the participation rate. This is a crucial challenge; in many countries, notably the United States, where labor force participation has been falling for years (see Figure 5).

Stemming the long-term decline in the participation rate is complicated, in part because there are several overlapping trends driving the decline. Partly it is a function of difficult labor market conditions following the financial crisis. The Great Recession (2007-09) resulted in a sharp contraction in the employment rate, from 63% in 2007 to 58% in 2011. 4 Much of that decline stemmed from the long-term unemployed leaving the labor force. But the decline in labor force participation has not been driven exclusively by frustrated job seekers. Demographics have also played a part.

In fact, the decline in the U.S. participation rate began in 2000, long before the financial crisis. Even as labor market conditions have improved over the past couple of years, labor force participation remains near the historically low levels of the late 1970s. This is partly a function of atrophying skills, but it also reflects downwards pressure from an aging population.

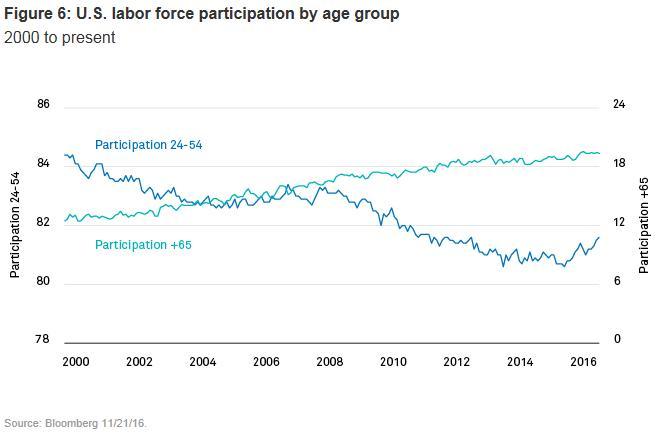

Thankfully, there is some room for optimism, as well as an opportunity for policy makers to lean into. While the overall percentage of working Americans is in decline, the participation rate for older Americans has been climbing (see Figure 6). To the extent this trend continues, it will help mitigate the myriad of headwinds facing the economy.

The Bureau of Labor Statistics forecasts that labor force participation for over-55 workers will rise from 41.6% in 2013 to over 43% in 2020. Recent research suggests those numbers could go even higher as more of these workers find they either are not financially prepared for retirement or simply wish to continue to work for non-financial reasons.

Should these additional workers over age 55 continue to work, and their labor force participation exceed the baseline forecast by 2.5 percentage points, this would result in an additional $103 billion in potential economic output in 2020. If older Americans' participation rate were to exceed the BLS forecast by five percentage points, this would yield an additional $203 billion in potential economic output in 2020. 5

Conclusion

While there is some evidence of a cyclical bounce, along with anticipation of stronger growth ahead, global output remains disappointing. Unfortunately, there is little agreement on the cause or cure.

Arguably, the bursting of the credit bubble is still exerting a drag on growth. That said, it is worth highlighting that the deceleration in growth predated the financial crisis. In the U.S., real growth has been slipping since 2000, coincident to the peak in labor force participation.

Increasing the rate of labor-force participation is not a panacea. This leaves unresolved the mystery of what happened to global productivity. But as policy prescriptions go, it is straightforward, intuitive and less contentious than other options. The math is simple. Over the long term, faster growth in the labor force equates with faster overall growth. To get there, societies must deploy all available resources. The elderly are one of the most underused resources. It is time to change that.

This post originally appeared on the BlackRock Retirement Institute .

Footnotes

- World Population Ageing, United Nations, Department of Economic and Social Affairs Population Division, 2015.

- Our World in Data , accessed 12/23/16.

- Demographics and Real Interest Rates: Inspecting the Mechanism, Carlos Carvalho, Andrea Ferrero, Fernanda Nechio, Federal Reserve Bank of San Francisco, March 2016.

- The State of American Jobs, How the shifting economic landscape is reshaping work and society and affecting the way people think about skills and training they need to get ahead, Pew Research Center, October 2016.

- The Longevity Economy: Generating Economic Growth and New Opportunities for Business, Oxford Economics, 2013.

See also Covestro Benefiting From A Cyclical Surge, But Trouble May Be Looming on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}