It seems like a long time ago when a faulty CrowdStrike Holdings (NASDAQ: CRWD) update caused a worldwide computer outage that gave one of the hottest cybersecurity companies a huge black eye. Since the outage occurred in July, the company's fiscal 2025 third quarter will be the first full quarter since the incident, giving the market a proper look at how much it impacted CrowdStrike's business.

Time has allowed CrowdStrike to recover, though the stock hasn't quite reclaimed its price at the time of the outage (an all-time high). It sits about 12% away as of this writing.

If you're sitting here, reading this, and wondering whether you should buy CrowdStrike before earnings drop on Nov. 26, buckle up.

Here are three burning questions CrowdStrike's third-quarter earnings will answer. Then, I'll offer my take on whether the stock is a buy today.

1. Did CrowdStrike lose business in Q3?

Looking beyond the outage, it's clear CrowdStrike is a fantastic growth stock. The company has consistently grown revenue by 30% or more while generating massive free cash flow and posting a GAAP profit.

The incident was shocking and probably the biggest challenge the company has faced since going public in 2019, but news coverage has gone pretty quiet. Because CrowdStrike's upcoming report is for the first full quarter since the outage, investors should be focused on any headwinds stemming from the outage given the highly competitive cybersecurity space.

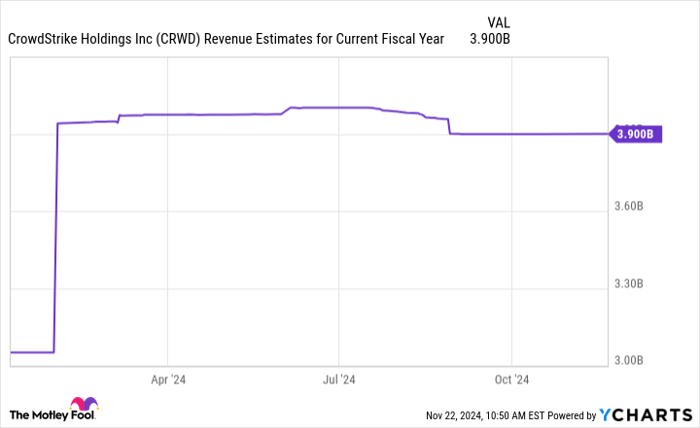

Perhaps the clearest indicator will be whether CrowdStrike meets Q3 revenue estimates. In late August, management guided for $979.2 million to $984.7 million of revenue, and the analyst consensus of $983.1 million falls neatly within that range.

Data by YCharts.

Management slightly lowered its full-year fiscal 2025 revenue outlook last quarter, and analysts followed suit. A miss next week could hint at customer losses following the outage.

2. Has the outage impacted profit margins?

In CrowdStrike's previous earnings call, management emphasized that sales momentum seemed strong immediately following the incident, pointing to some eight and nine-figure deals it won shortly after. But revenue doesn't tell the entire story. There's little doubt CrowdStrike's competitors ramped up their efforts following the outage.

Did CrowdStrike have to lower its pricing or offer other incentives to retain or win business? Investors should look at CrowdStrike's gross profit margin to see if there's any margin erosion. If there is, management will probably discuss it during the upcoming call, which could help paint a clearer picture of how the competitive landscape is shaping up. The company earned a 78% gross margin on subscriptions in Q2 and the year-ago quarter.

3. What does guidance look like?

Lastly, investors should review CrowdStrike's full-year guidance to help them see the bigger picture. Updated guidance will reveal a trend that will tell one of two stories:

- If management lowers guidance, it signals that the outage could have a longer-lasting impact than initially hoped. Remember, CrowdStrike already lowered its full-year guidance by approximately 2.6% in Q2.

- It would be a good sign for investors if management maintains or raises guidance. It could signal that the outage's impact is contained, and the market can move on.

CrowdStrike's guidance will likely shape the short-term narrative surrounding the stock. That's important because of its rally over the past few months and current valuation.

Is CrowdStrike a buy?

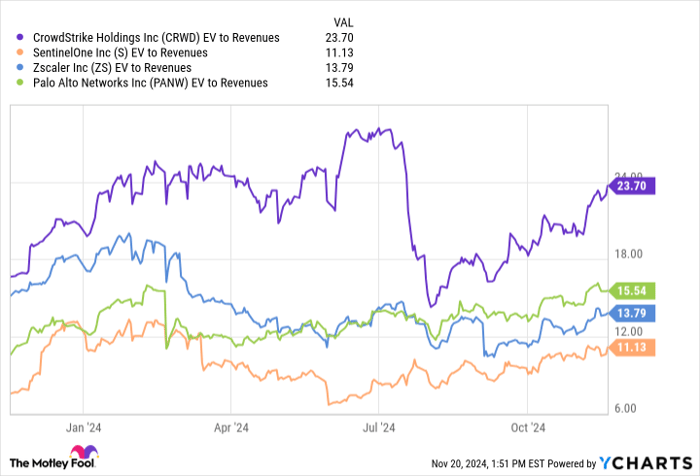

CrowdStrike's strong growth and margins have helped the stock earn a premium valuation over its peers. Just look at how CrowdStrike trades versus other cybersecurity stocks on an enterprise value-to-sales basis:

Data by YCharts.

The outage initially shrank the valuation gap between CrowdStrike and its competitors. Now that it's widened again, the company must deliver the results to back it up. A miss on revenue, shrinking margins, or tepid guidance are all examples of news that could threaten that valuation premium again.

So, is the stock a buy? It's hard to call CrowdStrike a buy given this uncertainty. I see it as an unfavorable risk-to-reward scenario, and investors should wait to see what the third quarter looked like before putting any money into the stock at these prices.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $368,053!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,533!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $484,170!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 18, 2024

Justin Pope has positions in SentinelOne. The Motley Fool has positions in and recommends CrowdStrike and Zscaler. The Motley Fool recommends Palo Alto Networks. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.