I recently purchased shares of one of the most critical companies in the chip supply chain. ASML (NASDAQ: ASML) provides high-end machines that nobody else makes to the chip producers, making it a technological monopoly. With companies like Taiwan Semiconductor Manufacturing (NYSE: TSM) seeing massive chip demand, you'd be forgiven for assuming that ASML's business is booming.

However, it's facing some struggles and after the company reported its third-quarter results, the stock tumbled by more than 20%. I saw this as a buying opportunity, and I think long-term investors should also use this chance to scoop up shares of one of the most important companies on the market.

ASML's machines are caught up in a chip war with China

ASML makes lithography machines, which are responsible for putting the microscopic traces on a chip. The company makes two types of machines: extreme ultraviolet (EUV) and deep ultraviolet (DUV). EUV machines are its most advanced, and Western governments (especially the U.S.) pressured ASML not to sell them to China. The Netherlands (where ASML is based) agreed and has placed an export ban on them.

However, it's still free to ship some of its less technologically advanced DUV machines. But ASML plans to stop servicing some DUV machines installed in China at the end of the year due to more pressure from the U.S. This could cause China to look elsewhere for similar technology or develop its own. This presents a problem, as 47% of Q3 sales went to China.

Competition is still far from replicating ASML's machines, forcing China to continue buying less advanced machines from ASML. Historically, China hasn't been as large a part of its business, and management expects this to return to a more normal percentage in 2025. So, investors' fears of China's impacts can be dampened.

Still, another piece of information caused the stock to tumble, and it's one investors must pay attention to.

ASML's stock is priced at attractive levels

Bookings are an important metric for ASML, as they tell investors what sales are in the pipeline. For Q3, net bookings came in at 2.6 billion euros ($2.81 billion), far below the 5.6 billion analysts were expecting. However, its backlog totals more than 36 billion euros, so there is still massive demand for its machines; it's just not seeing many new orders. There could be many reasons for this, but this lack of new orders may point to chip companies seeing how their capacity holds up to the latest chip demand.

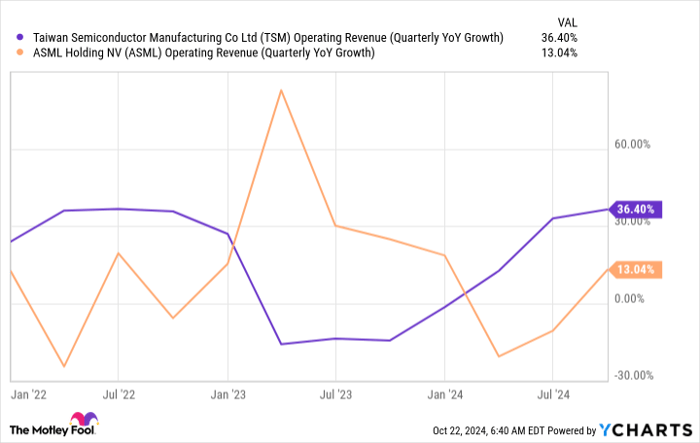

This raises a critical note about ASML's business: It is on a different cycle than chip companies. Because these machines are ordered years in advance of when chip companies anticipate demand, the waves of ASML's business are offset by a chip manufacturer like Taiwan Semiconductor.

TSMC Operating Revenue (Quarterly YoY Growth) data by YCharts

Still, investors had to adjust 2025 expectations as management reduced its revenue outlook from 30 billion to 35 billion euros from the previous range of 32.6 billion to 38.1 billion euros.

As a result, the stock plummeted. But if you have a long-term outlook that lasts past 2025, this could be a great buying opportunity. All things considered, I'd expect more chips to be needed in the future due to the movement of more digital devices in our lives. This requires more ASML machines, which will drive sales growth over the long term.

Additionally, this is the first time in a long time that you can buy shares of ASML at a reasonable price.

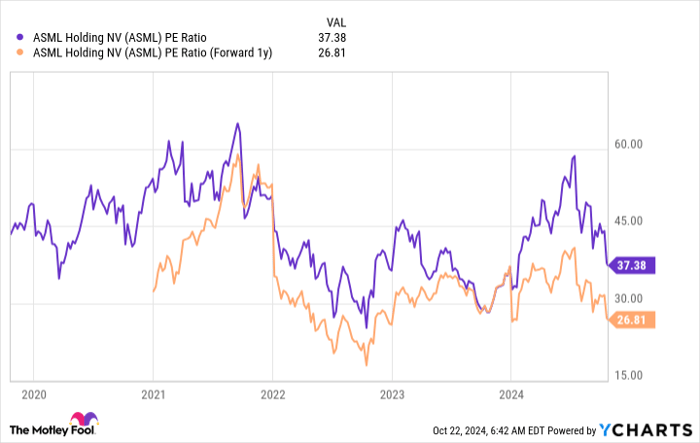

ASML PE Ratio data by YCharts

With the stock trading for 27 times 2025 earnings, I think it's a fantastic buy, as it's a critical supplier in the chip supply chain.

If business ramps up in 2026, then the price you pay today will likely look like a steal in the back half of 2025. I'm willing to wait a few years to watch ASML's business boom, which will likely allow my position to generate a solid profit. While ASML isn't without its challenges, its product is too critical to stay down for long.

Should you invest $1,000 in ASML right now?

Before you buy stock in ASML, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ASML wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $860,447!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 21, 2024

Keithen Drury has positions in ASML and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends ASML and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.