There are good stocks, and then there are great stocks. Good stocks can perform well for at least a while. Great stocks can be life-changing investments, often becoming a portfolio's chief growth driver. Investors will be glad to own some of the former, but ultimately, they'd rather wind up with the latter.

It's not yet clear which of those categories e-commerce platform Shopify (NYSE: SHOP) will ultimately belong to. It has been a fantastic performer since its 2015 IPO, despite its ups and downs. With the online shopping space growing ever more crowded though, can the stock continue to deliver outsized returns for long enough to set you up for life?

Shopify's a growth stock, and it's priced like one

On the off-chance you're reading this and aren't familiar, Shopify helps businesses of all sizes build and manage their own e-commerce operations.

Founded in response to merchants' and sellers' frustrations with platforms like Amazon or eBay, Shopify allows its clients to sell directly to customers rather than relying on a middleman. While Shopify charges subscription fees for access to its tech and takes a small cut of the sales it facilitates, it's often an attractive solution to business owners.

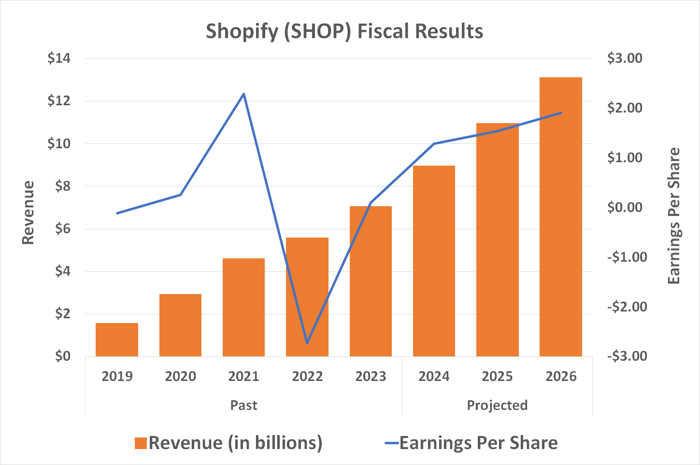

Today, the company facilitated more than $270 billion of merchandise sales through its platform in the past year, and it generated $8.2 billion of revenue for itself in the process.

Its top and bottom lines are still growing like wildfire, and they should continue doing so. The analyst community believes this year's projected top-line growth of nearly 25% will be followed by growth of more than 22% in 2025, which would boost its revenue to more than $10 billion. Earnings should nearly double to $1.32 per share this year before rising further to $1.51 in 2025.

Data source: StockAnalysis.com. Chart by author.

As impressive as this progress may be, Shopify's growth rate is slowing down -- a function of its sheer size, its previous rapid growth, and an increasingly saturated (and competitive) market. Those factors aren't apt to change, either. Meanwhile, the stock has become expensive, trading at 77 times next year's projected earnings. The stock is also trading just below the analyst community's consensus 12-month price target of $119.70. Moreover, nearly half of those analysts rate the stock as a mere "hold" at this time.

That doesn't add up to an overwhelmingly bullish sentiment.

Take a step back and look at the bigger picture, though. The company still has a massive amount of room for growth. And as the market share leader in key regions, Shopify stands ready to capture more than its fair share of e-commerce's ongoing expansion.

The rising tide is still nowhere near its peak

For all the hype and disruption that e-commerce has created here and abroad, online shopping isn't nearly as big as most investors might expect yet. The Census Bureau reports that only about 16% of U.S. retail sales are handled online. The large majority of shopping is still done in person, in brick-and-mortar stores. Similar numbers apply overseas.

For logistical and convenience reasons, some of this business will never move offline. Yet a big chunk of that 84% of retail spending could. A report from Forrester Research predicts the global e-commerce market could grow from $4.4 trillion this year to $6.8 trillion by 2028. That jibes with forecasts from the U.S. Department of Commerce. And even then, online shopping would account for a little less than one-fourth of the world's retail spending. That would still leave plenty of room for further penetration of a global retail market that should be worth $29 trillion by then. As the number of digitally native consumers continues to rise, look for online shopping to become even more mainstream.

For Shopify, any and all e-commerce market growth stands to help its results. More importantly, it should disproportionately help its bottom line.

This is a business that scales up quite well. Whether the company supplies its technology and platform to 5,000 businesses or 5 million, the cost of developing it is largely the same, while the incremental costs of deploying it to more customers are relatively small. Even though its pace of profit growth may technically be slowing down, look for the company's profit margins to continue widening as time marches on. That's why Shopify stock is apt to grow into its currently rich valuation -- and perhaps sooner than many investors might expect.

Worth the likely wild ride

Expensive stocks are inherently volatile, even if they're en route to a fairer valuation. This one is no exception. If you're convinced Shopify's future is bright, you can still bide your time just a bit to see what happens once the big run-up from August's low completely cools. You might be able to step in at a better price than the current one.

Just don't wait too long or be too stingy price-wise. More and more investors seem to be connecting the dots regarding e-commerce's long-term future while realizing Shopify's dominant place in it. Their optimism could buoy the shares.

So yes, buying Shopify stock today could help set you up for life. The world's likely to need more and more of its platform and services as consumers continue to shift their spending online. The end of this business's growth phase could be decades down the road, so an investment in it today could pay off for a lifetime.

Should you invest $1,000 in Shopify right now?

Before you buy stock in Shopify, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Shopify wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $822,755!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 9, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Shopify. The Motley Fool recommends eBay. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.