Two rival stocks that typically resonate with investors because of their value and steady expansion are Coca-Cola (KO) and PepsiCo (PEP). Now is a good time to see if this resonation is holding with both reporting their Q4 results for fiscal 2023 within the last week.

Let’s take a look at the quarterly reviews for these beverage giants along with their guidance, recent performance, and valuations to see if now is a good time to buy.

Coca-Cola Q4 Review

Reporting Q4 results this morning Coca-Cola was able to beat top and bottom-line expectations attributed to higher sales prices despite volume falling -1% in its core North American segment. Fourth quarter earnings of $0.49 a share topped the Zacks Consensus by 2% and rose 9% year over year. On the top line, Q4 sales of $10.84 billion surpassed estimates by 2% as well and were up 7% from the comparative quarter.

Coca-Cola has beaten earnings expectations in each of its last four quarterly reports and has now topped sales estimates for 12 consecutive quarters. Overall, Coca-Cola’s total sales grew 6% in FY23 to $45.8 billion with annual earnings rising 8% to $2.69 per share.

Image Source: Zacks Investment Research

Pepsi Q4 Review

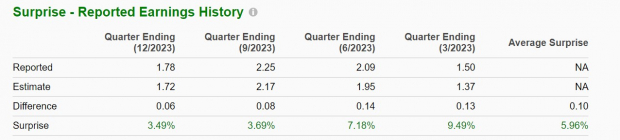

Pepsi also attested to slower U.S. sales when it reported its Q4 results last Friday and stated its North American beverage volume was down -6%. However, Pepsi was able to beat earnings expectations despite missing top line estimates for the first time since 2018. Quarterly sales of $27.85 billion missed estimates of $28.24 billion by -1% and were slightly down from $27.99 billion a year ago which was Pepsi’s first revenue decline in almost four years.

In regards to Pepsi’s snack business which separates the company’s offerings from Coca-Cola, its Quaker Foods and Frito-Lay North American segments also saw lower volumes of -8% and -2% respectively. Still, Q4 earnings of $1.78 per share came in 3% better than expected and was up 6% YoY. Despite an end to an unprecedented streak of surpassing sales expectations, Pepsi has now topped earnings estimates for eight consecutive quarters. Furthermore, total sales were up 6% in FY23 to $91.47 billion with annual EPS spiking 12% to $7.62 per share.

Image Source: Zacks Investment Research

Fiscal 2024 Guidance

In their guidance for FY24, Coca-Cola forecasts revenue growth of 6-7% and a 4-5% increase in EPS while Pepsi expects a 4% increase in revenue and EPS growth of at least 8%.

Recent Performance & Valuation

Pepsi shares are down -1% in the last year while Coca-Cola’s stock is down -5% with both underperforming the S&P 500’s +22% and their Zacks Beverages-Soft Drinks Market’s +7%. With that being said, over the last three years, Pepsi’s +25% has roughly matched the benchmark although this has trailed its Zack Subindustry’s +33% while Coca-Cola’s +16% has lagged further behind.

Image Source: Zacks Investment Research

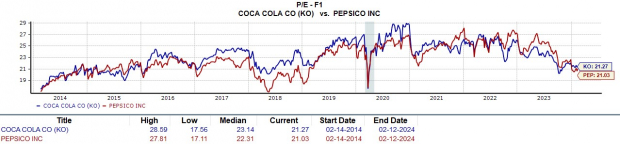

Notably, Coca-Cola and Pepsi's stock trade at around 21X forward earnings which is on par with the S&P 500 and near their industry average of 19.6X with both being historical leaders in the space.

Image Source: Zacks Investment Research

Exceptional Dividend Growth

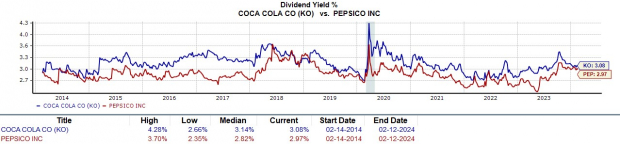

Being “dividend kings” and increasing their payouts for at least 50 consecutive years has continued to bolster the value of Coca-Cola and Pepsi stock. Coca-Cola has raised its dividend for 62 consecutive years with Pepsi at 52 years and counting. At the moment Coca-Cola’s 3.08% annual dividend yield slightly tops Pepsi’s 2.97%.

Image Source: Zacks Investment Research

Bottom Line

Although Coca-Cola and Pepsi are dealing with lower volumes attributed to consumers being more conservative on their budgets both stocks land a Zacks Rank #3 (Hold). To that point, longer-term investors may be rewarded from current levels with Coca-Cola and Pepsi still expecting steady growth in FY24 while offering generous and safe dividends to shareholders.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>CocaCola Company (The) (KO) : Free Stock Analysis Report

PepsiCo, Inc. (PEP) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.