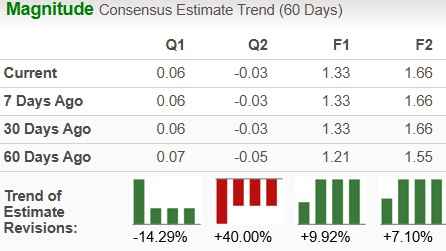

Carnival Corporation & plc CCL, a cruise and vacation company, witnessed 9.9% and 7.1% growth in its fiscal 2024 and 2025 earnings per share (EPS) estimates over the past 60 days. Considering the break-even EPS reported in fiscal 2023, the estimate for fiscal 2024 indicates notable year-over-year growth. Fiscal 2025 earnings estimates reflect 25.2% year-over-year growth.

Image Source: Zacks Investment Research

The company’s performance is driven by notable cost-saving opportunities, a tone down in inflationary pressures, benefits from one-time items and the timing of expenses between the quarters. Also, benefits realized from increased top-line growth, backed by sustained demand strength and increased booking volumes, add to the uptick.

The 60-day earnings estimate growth trend for Carnival remains higher for fiscal 2024 compared with other significant industry players, including Royal Caribbean Cruises Ltd. RCL, Norwegian Cruise Line Holdings Ltd. NCLH and Lindblad Expeditions Holdings, Inc. LIND. Over the past 60 days, 2024 earnings estimates for RCL and NCLH grew 1% and 5.1%, while the same declined 13.9% for LIND.

Moreover, shares of Carnival have gained 50% over the past three months, outperforming the Zacks Leisure and Recreation Services industry, the Zacks Consumer Discretionary sector and the S&P 500. The detailed price performance is shown in the chart below.

Image Source: Zacks Investment Research

Factors Aiding CCL Stock

Solid Demand Trend: Carnival has been witnessing solid demand for its services throughout its global fleet offerings. The uptrend is backed by increased booking trends, enhanced commercial execution and diversified fleet offerings with enhanced onboard services. During the first nine months of fiscal 2024, consolidated revenues increased 17.8% year over year to $19.08 billion, driven by 19% growth in Passenger Ticket revenues and 15% growth in Onboard and other revenues.

Notably, CCL’s strategic investment in advertising is yielding significant returns, thereby stimulating demand across its portfolio with the launch of several new campaigns during the peak season. The company’s marketing efforts, along with support from travel agents and the narrowing of the unjustified price gap with land-based vacations, have helped attract newer and existing guests, leading to market share gains.

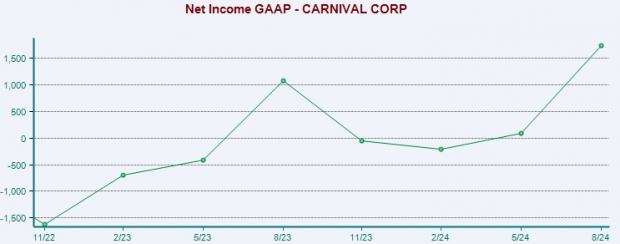

Expectations for Net Income: Having reported a $74 net loss in fiscal 2023, Carnival is currently expecting a $1.76 billion net income in fiscal 2024. The improvement is backed by three essential factors, including growth in net yields (which is a measure of revenue per available passenger cruise day after subtracting direct costs and expenses), improvement in cruise cost per ALBD (available lower berth day) and benefit from fuel pricing.

The improvements mentioned above are also backed by higher ticket prices, increased onboard spending and higher occupancy across the Atlantic brands and somewhat in the European brands. The net income (loss) trend for the past year can be observed in the chart below.

Image Source: Zacks Investment Research

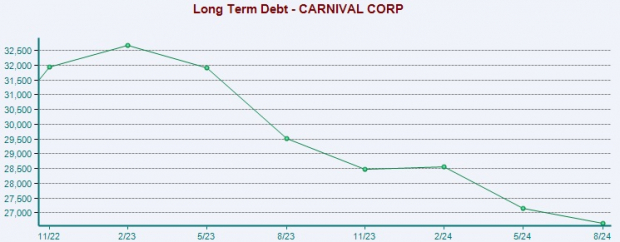

Declining Debt Levels: Since the beginning of fiscal 2024, Carnival has been managing its cash position while reducing its long-term debt levels. The company has been focusing on its refinancing and deleveraging efforts, which have undoubtedly helped it in managing its debt profile. Since the beginning of fiscal 2024, the quarter-wise long-term debt levels were $28.544 billion, $27.154 billion and $26.642 billion. This compares with $28.483 billion at the fiscal 2023-end. Also, the company is likely to benefit from decreased interest rates. If Carnival can refinance a portion of this debt at more favorable rates, it could see a reduction in interest costs, thereby boosting its financial performance. The quarterly trend of long-term debt for the past year is given below.

Image Source: Zacks Investment Research

The company aims to continue searching for more opportunistic re-financings over time, thus reducing debt further and improving adjusted EBITDA. At the end of the nine months of fiscal 2024, adjusted EBITDA improved 48.9% year over year to $4.89 billion.

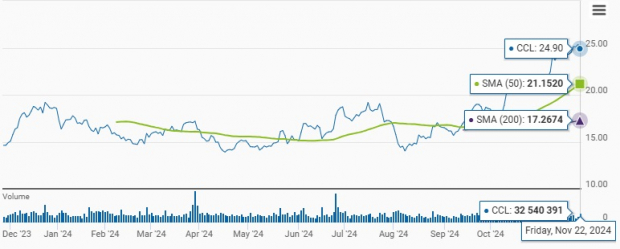

CCL Stock Trading Above 50 & 200-Day SMA

Technical indicators suggest a continued strong performance for Carnival. From the graphical representation given below, it can be observed that CCL stock is trading above both the 50-day simple moving average (SMA) and 200-day SMA, signaling a bullish trend. The technical strength underscores positive market sentiment and confidence in CCL’s financial health and prospects.

50 & 200-day Moving Average

Image Source: Zacks Investment Research

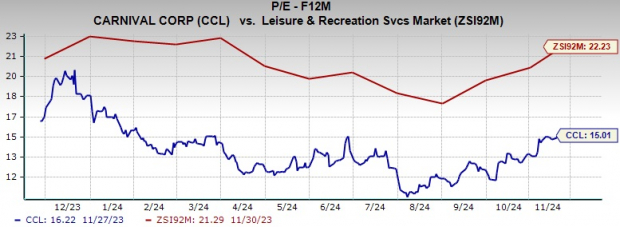

CCL Trading at a Discount

Carnival is currently trading at a discount compared with the industry peers on a forward 12-month price-to-earnings (P/E) ratio basis. The discounted valuation indicates that despite the recent stock price increase in the past three months, it remains an attractive option for investors looking for a suitable entry point.

Image Source: Zacks Investment Research

Should You Consider CCL Stock: Yay or Nay?

As discussed above, Carnival is benefiting from its cost-saving initiatives, favorable pricing, demand-boosting strategies and the objective of reducing its debt level. Its focus on realizing benefits from increased top-line growth by reducing debt levels and ensuring shareholder value is encouraging. Such motives of the company must be considered by investors when undertaking any decisions in favor of the stock.

Thus, based on the overall discussion and the favorable trends of technical indicators, investors can consider adding this Zacks Rank #1 (Strong Buy) stock to their portfolio for now. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is among the most innovative financial firms. With a fast-growing customer base (already 50+ million) and a diverse set of cutting edge solutions, this stock is poised for big gains. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpCarnival Corporation (CCL) : Free Stock Analysis Report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH) : Free Stock Analysis Report

Lindblad Expeditions (LIND) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.