Canadian pipeline giant, Enbridge (NYSE: ENB), dropped big news on Sept. 5 when it announced the $14 billion acquisition (including debt) of three natural gas utilities from Dominion Energy (NYSE: D). The deal makes Enbridge North America's largest natural gas utility franchise.

Enbridge believes the deal is a win for shareholders, but investors didn't react favorably, sending the stock down 5.9% to a two-year low. The sell-off pole-vaulted Enbridge's dividend yield to 7.9%, making it an intriguing high-yield dividend stock. Let's look at the impact of the deal, what it means for Enbridge, and if the stock is worth buying now.

Image source: Getty Images.

A bold bet on oil and natural gas

Today, the oil and gas industry is at a crossroads. There are some companies that are diversifying their businesses by selling fossil fuel assets and investing in renewable energy. Many companies have set carbon reduction or even net-zero goals that depend on either working outside of oil and gas through renewables; exploring burgeoning ideas like hydrogen, renewable natural gas, renewable diesel, etc.; investing in technologies like carbon capture to offset emissions; and more.

Pipeline companies that transport natural gas and liquids (oil, diesel, natural gas liquids, etc.) can either continue investing in those industries and/or invest in new infrastructure assets like hydrogen pipelines; retrofitting natural gas pipelines to be ready for hydrogen; or investing in new infrastructure assets altogether.

Dominion Energy, a utility, is shifting its focus away from fossil fuel assets toward renewable energy. It is aggressively investing in offshore wind to produce electricity from renewable energy. In 2020, it sold several oil and gas assets to Warren Buffett's Berkshire Hathaway (NYSE: BRK.A) (NYSE: BRK.B) Energy for a bargain-bin price. And now, it's selling a swath of gas utilities to Enbridge for 16.5 times 2023 estimated earnings.

Enbridge claims that this valuation is a good deal and that it is on the short list of companies that could even afford a deal of this size. But all because a large company can do a deal doesn't mean it should, especially at the expense of its balance sheet. The price is decent, but it's not great. 16.7 times 2024 estimated operating earnings for a zero growth to low-growth business is a steep jump from the 10.8 times estimated 2025 EBITDA that Berkshire Hathaway Energy agreed to pay for the remaining 50% non-controlling interest in Cove Point LNG. And that agreement was made just two months ago.

Enbridge is taking a unique approach. It is betting big on North American natural gas and oil production and export. And in the process, it's ready to go toe-to-toe with regulators and stakeholders that oppose investing in oil and gas. It's not just a play on the prevalence of fossil fuels in North America but also the need for infrastructure to support the transportation and distribution of these fuels from areas of production to areas of consumption or export. "We think the future of oil is through and out of North America," said Enbridge CEO Greg Ebel in an interview with CNBC's Squawk Box. He added:

The future of natural gas is through North America and exports. But without a doubt, as you see population growth and you see sustainability and you see the need for that consumer choice, we're going to do all of those things.

In other words, Ebel recognizes the importance of sustainability but also believes that North American oil and gas is a growth industry that won't get displaced by renewables. Again, the issue is that natural gas distribution utilities are not a growth industry. So Enbridge isn't benefiting from the growth of fossil fuels with this investment, but rather, the sustained relevance of fossil fuels

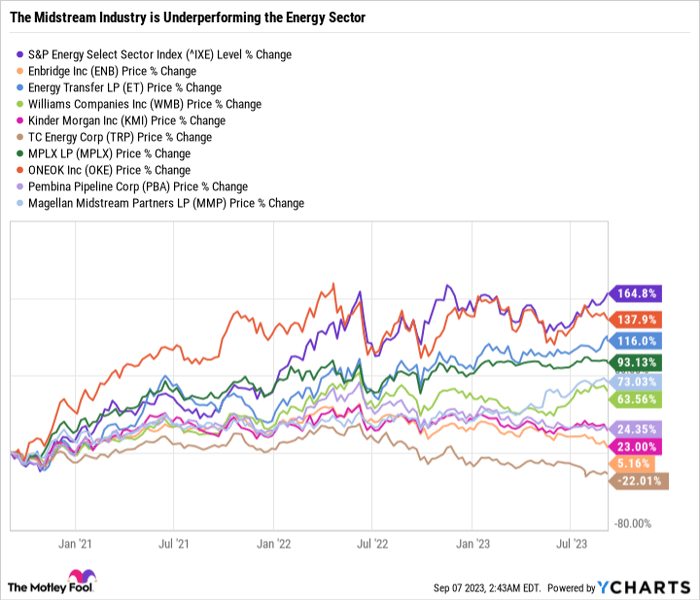

The midstream industry is out of favor

The oil and gas industry is split into three subcategories -- upstream (exploration and production), midstream (pipelines and storage), and downstream (refining and marketing). The upstream industry, and to a lesser extent the downstream industry, have been contributing the bulk of the gains in oil and gas stocks, while the midstream industry has been sitting on the sidelines.

The energy sector has been on a tear for the last three years and is up 164.8% over that period. However, the largest North American midstream stocks by market cap have all underperformed the energy sector. Enbridge stock is up just 5.2% over the last three years, making it a major loser during an otherwise decent time for the midstream industry and an excellent time for the energy sector.

To some extent, this is expected. Due to fixed contracts and less dependence on oil and gas prices, the midstream industry typically outperforms the broader energy sector during downturns and underperforms it during growth cycles. At least that's how the dynamic played out historically. But companies built out so much infrastructure in the 2010s that there hasn't been as much opportunity for growth aside from assets related to natural gas exports. Additionally, many midstream companies have a lot of debt, making them particularly sensitive to interest rate changes. Add it all up, and it's not too surprising to see extreme underperformance from companies like Enbridge in recent years.

Understanding the Canadian energy market

Part of the reason Enbridge has underperformed the midstream industry as a whole may be due to its concentration in Canada. Enbridge, TC Energy, and Pembina Pipeline -- three Canadian pipeline giants, have drastically underperformed their peers over the last three years. Canada doesn't have the oil and natural gas export infrastructure that the U.S. has. And Canada's liquefied natural gas (LNG) industry has been largely stalled compared to a booming U.S. LNG industry, which supports infrastructure investments. More natural gas exports means more natural gas production and thus, more pipelines. Canada also has an aggressive goal to reduce emissions by 40% to 45% relative to 2005 levels by 2030 and then achieve net-zero emissions by 2050. Betting big on LNG is a step in the wrong direction toward achieving that goal.

Enbridge moves about 20% of all natural gas consumed in the U.S. and serves around 15% of U.S. Gulf Coast LNG export capacity. It also exports natural gas to Mexico. So assuming Enbridge is just a Canadian pipeline player and overlooking its U.S. assets would be a mistake.

The company has a leading position in Alberta and British Columbia (B.C.). And it hopes that B.C. will become an LNG export hub to Asia. But the export hub just hasn't really taken off yet after many Canadian LNG projects were shelved during the COVID-19 pandemic.

Enbridge is a good value

All told, Enbridge's strategy is going against Canada's emission-reduction targets. And buying Enbridge stock is a bet on the sustained relevance of oil and natural gas. The good news is that Enbridge isn't an expensive stock. And it has the cash flow and balance sheet to support dividend raises. Enbridge is taking a contrarian approach to the energy transition. But at least for now, the economy runs on oil and gas. Enbridge is providing essential services and getting good deals on its acquisitions. From a business perspective, the execution is there. And if Enbridge is right, it could pay off big time.

The biggest criticism for Enbridge is the price it paid for Dominion's gas utility assets and if that capital could have been better spent simply buying back its own stock. Buybacks benefit existing shareholders by reducing the outstanding share count and boosting earnings per share -- making the stock a better value. But they also benefit Dominion by reducing its dividend expense. Taking on the debt of Dominion's assets boosts Enbridge's interest expense. So even though the assets are stable and will boost cash flow, there is an added expense and an opportunity cost associated with the purchase.

It's not the perfect deal. But Enbridge's 7.9% dividend yield is reason alone to own the stock. And given how far the stock has fallen and how out of favor the midstream industry is, now looks like a great time to take a closer look at Enbridge.

10 stocks we like better than Enbridge

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Enbridge wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of September 5, 2023

Daniel Foelber has the following options: long October 2023 $45 calls on Dominion Energy. The Motley Fool recommends Berkshire Hathaway, Dominion Energy, Enbridge, Kinder Morgan, Magellan Midstream Partners, ONEOK, Pembina Pipeline, and Tc Energy. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.