While Nvidia has been the biggest semiconductor stock winner from the artificial intelligence (AI) infrastructure buildout, Broadcom (NASDAQ: AVGO) could be poised to be the next big winner in the space. The stock is trading up about 47% on the year as of this writing, but down about 12% from its recent highs.

Let's dig into Broadcom's AI opportunity and whether now is a good time to buy the stock.

Is Broadcom the next big AI winner?

Broadcom participates in the AI infrastructure buildout in two primary ways. The first is through its networking portfolio, where it provides such components as switches and NICs (network interface cards). Switches are used for communication between two or more devices, while NICs provide network connections.

The company contends that as AI clusters grow in size, there will be distributed computing challenges, and networking will become an increasingly more important piece of the infrastructure buildout. The reason is that it will cause a distributed computing challenge that needs to be solved. Currently, there are competing switching technologies in the space trying to solve this issue.

While Intel has a switching technology called Omni-Path, the two most prevalent switching technologies are Nvidia's InfiniBand, which it acquired with its acquisition of Mellanox, and Ethernet. Broadcom is at the forefront of advanced Ethernet switching. The company believes all hyperscalers will be using the technology by the first half of 2025, as it thinks the technology is superior in handling AI workloads and transferring data between GPUs.

Thus far, different cloud computing companies have preferred employing different technologies, with Microsoft opting for InfiniBand while Amazon has leaned more into Ethernet. Nonetheless, the market appears to be large enough for multiple winners, with Broadcom seeing its Ethernet switching revenue quadruple in the third quarter.

The bigger opportunity for Broadcom, however, is helping customers develop custom chips (application-specific integrated circuits, or ASICs) for their AI workloads. For its part, the company argues that custom ASICs are superior to Nvidia's mass merchant graphics processing units (GPUs) in a hyperscale cloud environment, although that certainly does not show up in the two companies' revenue numbers.

That said, there is certainly a place for custom AI silicon, and a number of companies are working with Broadcom to develop custom chips designed for specific computing and power needs.

Alphabet was Broadcom's first big ASIC customer, as it helped the company create its tensor-processing unit for AI workloads. The chipmaker has said it added two new customers this year, which are widely believed to be Meta Platforms and TikTok owner ByteDance. Meanwhile, major news outlets have reported that OpenAI has been working with Broadcom on its own custom chips, although neither company has confirmed this.

Broadcom continually raised its expectations for AI revenue throughout the year. It originally forecast approximately $7.5 billion in AI revenue for 2024, while that guidance has risen steadily to currently be at $12 billion. With its new customers, I would expect that revenue to continue to grow nicely in 2025. However, with so few customers, custom ASIC revenue growth can be lumpier than the type of growth Nvidia generates.

Image source: Getty Images.

Is it time to buy Broadcom stock?

While Broadcom's AI-related businesses have been performing strongly, its non-AI semiconductor businesses have struggled. Last quarter, its server storage connectivity revenue dropped 25% year over year while its broadband revenue sank 49%. Meanwhile, its wireless revenue only edged up 1%.

However, there are certainly signs that these more cyclical businesses have found a bottom in recent quarters. Server storage connectivity revenue grew sequentially, while it expects broadband revenue to recover early in 2025. Meanwhile, it is looking for wireless revenue to jump 20% sequentially in the fourth quarter.

A recovery in its non-AI semiconductor businesses, plus its AI growth, should bode well for 2025. Meanwhile, the company continues to integrate and transition its VMWare software business to a more recurring subscription model. This strategy has been seeing solid momentum, with annualized bookings up 32% last quarter compared to the preceding quarter.

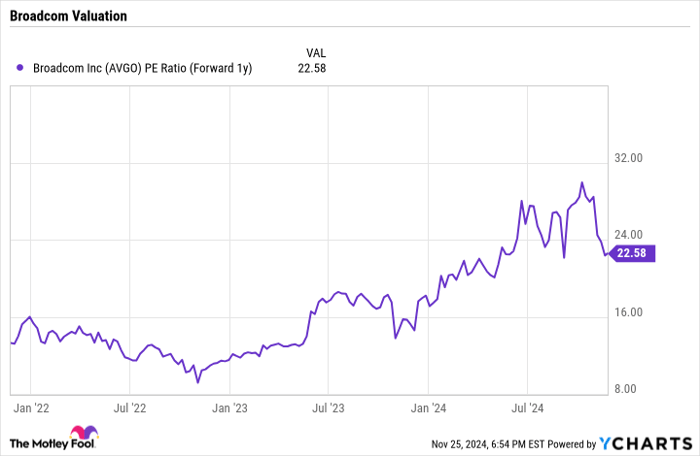

From a valuation perspective, Broadcom now trades at a forward price-to-earnings (P/E) ratio of around 22.6 times next year's analyst estimates.

AVGO PE Ratio (Forward 1y) data by YCharts.

Given that many of its cyclical businesses appear to be near their bottoms and the AI opportunity in front it, Broadcom looks like a solid option for investors to consider buying at current levels. If custom AI chips are the next big wave, Broadcom will be very well-positioned.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $350,915!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,492!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $473,142!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 25, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Geoffrey Seiler has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Amazon, Intel, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft, short February 2025 $27 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.