We are off to a good enough start in the Q4 earnings season, though it may be hard to reach that conclusion from the seemingly ‘noisy’ big bank results. Please note that the bank results aren’t bad or weak, though most struggled to beat consensus revenue estimates.

Bank of America’s Q4 earnings declined -17.3% from the year-earlier period on -10.5% lower revenues. The bank’s Q4 earnings actually beat estimates, so the year-over-year decline, largely due to the FDIC fee, was no surprise to the market. The combined FDIC fee for the four big banks – Bank of America BAC, JPMorgan JPM, Citigroup C & Wells Fargo WFC – collectively paid $9 billion in the FDIC fee.

Bank of America continued to enjoy strong net interest earnings in the quarter, though the tally was modestly below the year-earlier period. The bank’s strong net interest earnings performance mirrored what we saw from JPMorgan, Wells Fargo, and even Citigroup C, who appeared to be following a kitchen-sink approach in its Q4 earnings release.

With respect to the 2024 outlook for this key profitability driver, JPMorgan expects its net interest earnings to be flat, Wells Fargo is projecting a high single-digit decline, and Citi expects a ‘modest’ decline. This all makes sense, given the expected decline in rates and the macro-driven moderation in credit demand.

Credit quality metrics have started weakening but remain well within ‘normal’ ranges. The commercial real estate space is particularly vulnerable in this respect, though exposure to the ‘office’ market is a much bigger issue for the regional banks than these money-center operators. The Q4 reporting cycle expands to the regional banks and brokers this week.

In terms of the Finance sector’s Q4 scorecard, we now have results from 22.8% of the sector’s total market capitalization in the S&P 500 index. Total earnings for these banks are up +6.3% from the same period last year on +2.3% higher revenues, with all of the banks beating EPS estimates (100% beats percentage) and only 50% exceeding revenue estimates. The lower revenue beats percentage for the banks is a trend we are noticing outside of the Finance sector as well.

The Earnings Big Picture

The chart below shows the earnings and revenue growth rates actually achieved in the preceding four quarters and current earnings and revenue growth expectations for the S&P 500 index for 2023 Q4 and the following three quarters.

Image Source: Zacks Investment Research

As you can see here, 2022 Q4 earnings are expected to be up +0.1% on +2.2% higher revenues. This follows the +3.8% earnings growth reading we saw in the preceding period (2023 Q3) and three back-to-back quarters of declining earnings before that.

This chart, which accurately represents current bottom-up consensus earnings expectations aggregated to the index level, does not see an earnings recession over the next three quarters. If anything, revenue growth is trending up over this period.

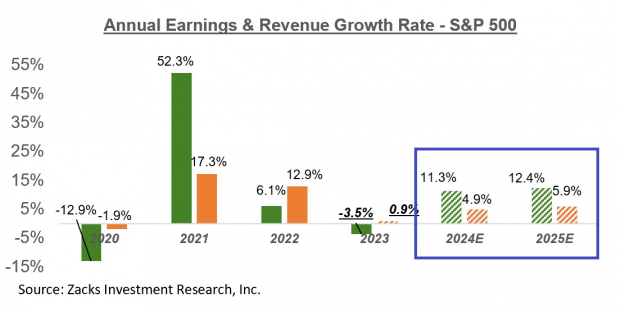

The chart below shows the earnings picture on an annual basis.

Image Source: Zacks Investment Research

It isn’t just the next three quarters where the long-feared recession is missing in action, but actually over the next two years as well, as you can see above.

The earnings recession proponents have been telling us for more than a year that earnings estimates were out-of-sync with the underlying economic reality and needed to be cut in a big way.

We did see a period of significant negative estimate revisions that started in April 2022 and lasted for about a year. During that period, estimates in the aggregate declined by about -15% from peak to trough, with the magnitude of negative revisions for several sectors exceeding -20%. These included Construction, Consumer Discretionary, Technology, and Retail.

The revisions trend stabilized in April 2023, with earnings estimates for several major sectors, including the Tech sector, starting to go up again. This favorable revisions trend remained in place until October 2023 when estimates started easing all over again.

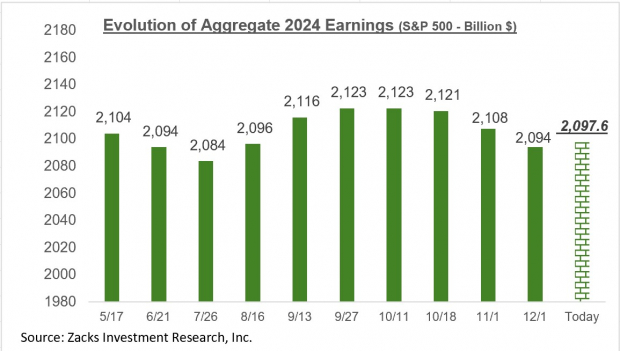

The current reading on the revisions trend is that they appear to have stabilized again, as you can see in the chart below that shows how the aggregate bottom-up earnings total for 2024 has evolved lately.

Image Source: Zacks Investment Research

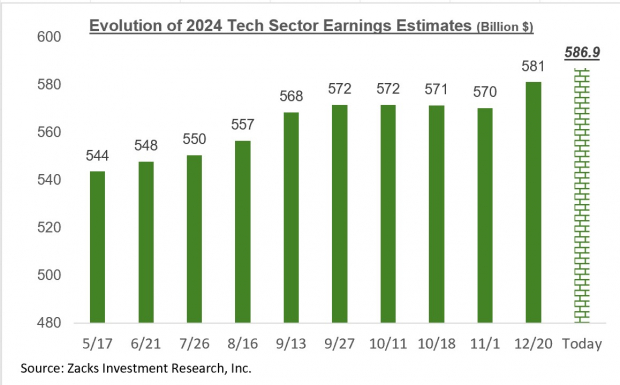

One sector whose earnings outlook appears to have notably turned around is the Tech sector. This sector has a bigger bearing on the aggregate earnings picture than any of the 15 Zacks sectors in the S&P 500 index, as it is on track to bring in more than 28% of the index’s total earnings over the coming four-quarter period.

You can see the recent uptrend in Tech sector estimates in the chart below, which shows the aggregate 2024 earnings estimates for the sector.

Image Source: Zacks Investment Research

Other sectors whose 2024 earnings estimates also appear to have inched up lately include Retail, Autos, Aerospace, and Utilities.

While estimates for all the other sectors are still under pressure, sectors facing the most pressure on estimates include Transportation, Industrial Products, and Consumer Discretionary.

The Scorecard & This Week’s Reporting Docket

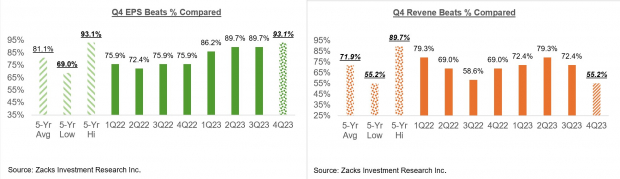

Including Friday’s results from the big banks, we now have Q4 results from 29 S&P 500 members. Total earnings for these 29 index members are up +7.6% from the same period last year on +6% higher revenues, with 93.1% beating EPS estimates and 55.2% beating revenue estimates.

We have about 50 companies on deck to report results this week, including 23 S&P 500 members. As noted earlier, this week’s reporting docket is dominated by the major regional banks and the major brokerage firms, which includes Goldman Sachs and Morgan Stanley.

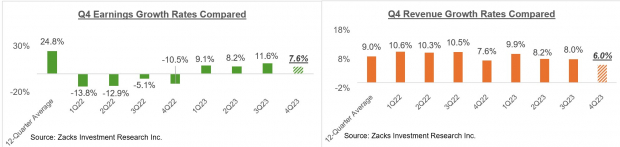

The comparison charts below put the Q4 earnings and revenue growth rates in a historical context.

Image Source: Zacks Investment Research

The comparison charts below put the Q4 EPS and revenue beats percentages in a historical context.

Image Source: Zacks Investment Research

This is way too small a sample of results to draw conclusions about the coming reporting season. But at this early stage,

- Earnings and revenue growth rates for this group of 29 index members are tracking roughly in line with what we had seen for the same group of companies in other recent periods

- Companies are beating EPS estimates comfortably, but appear to be struggling with beating revenue estimates.

For a detailed look at the overall earnings picture, including expectations for the coming periods, please check out our weekly Earnings Trends report >>>>Q4 Earnings Season Gets Underway

Zacks Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>Bank of America Corporation (BAC) : Free Stock Analysis Report

Wells Fargo & Company (WFC) : Free Stock Analysis Report

JPMorgan Chase & Co. (JPM) : Free Stock Analysis Report

Citigroup Inc. (C) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.