Credit: Shutterstock photo

Credit: Shutterstock photoBy SA Author Experience :

Free cash flow (or FCF) is one of the best ways to measure the cash generating power and intrinsic value of a company.

A commonly accepted definition of FCF is operating cash flow (or OCF) minus capital expenditures (or capex). So for Rosetta Stone (NYSE: RST ), per the recent 10-K , there was ~$6.4M of FCF in 2017.

Best Practices

Never simply subtract investing cash flow from OCF to arrive at FCF. In most of the cases, the resulting figure will be not meaningful and/or wrong as investing cash flow includes items such as acquisitions and proceeds from sales (which could even make investing cash flow positive).

It is generally a good idea to exclude acquisitions and only consider "normal" capex (typically presented as purchases of property and equipment) to get a more accurate picture of normalized FCF. I will provide a caveat that should interdict any tomatoes headed my way for saying you should exclude acquisitions from FCF.

For companies pursuing an explicitly stated roll-up strategy or for those companies that seem to keep making one-off acquisitions every year, it is probably a good idea to include acquisitions, as without these acquisitions, arguably, the business model falls apart. This is a similar concept to a company having non-recurring charges every single year for 10 years.

EBITDA is not FCF and is rarely OCF. You can probably count the exceptions to this on one hand. Here is one:

The three primary factors to bridge EBITDA to FCF are interest, taxes and capex.

For example, Company A has:

No debt so no interest payments.

A large NOL balance so its effective cash taxes are zero.

It has no capex needs because it is in a mature industry with stable demand (think consumer non-cyclicals) or it runs all spending through the income statement in the form of SG&A or R&D.

As you can see, this is a pretty special case, and for the most part, it's important not to simply equate EBITDA with FCF or OCF.

Other Important Free Cash Flow Considerations

See how management presents FCF. In investor presentations, management will often provide historical or projected FCF figures. In the smallest font imaginable in the footnotes or on the disclosure page, they will usually say how they calculate FCF. There is nothing wrong with this - you just need to know how management's definition squares with yours.

Decide whether to include or exclude changes in working capital in OCF. A case can be made for either. Including these changes provides a more realistic view of the ultimate cash needs of the business (especially for companies with significant inventory needs or accounts receivables). However, excluding these changes (which can be "noisy" and mask true OCF) can present a more accurate view of normalized OCF.

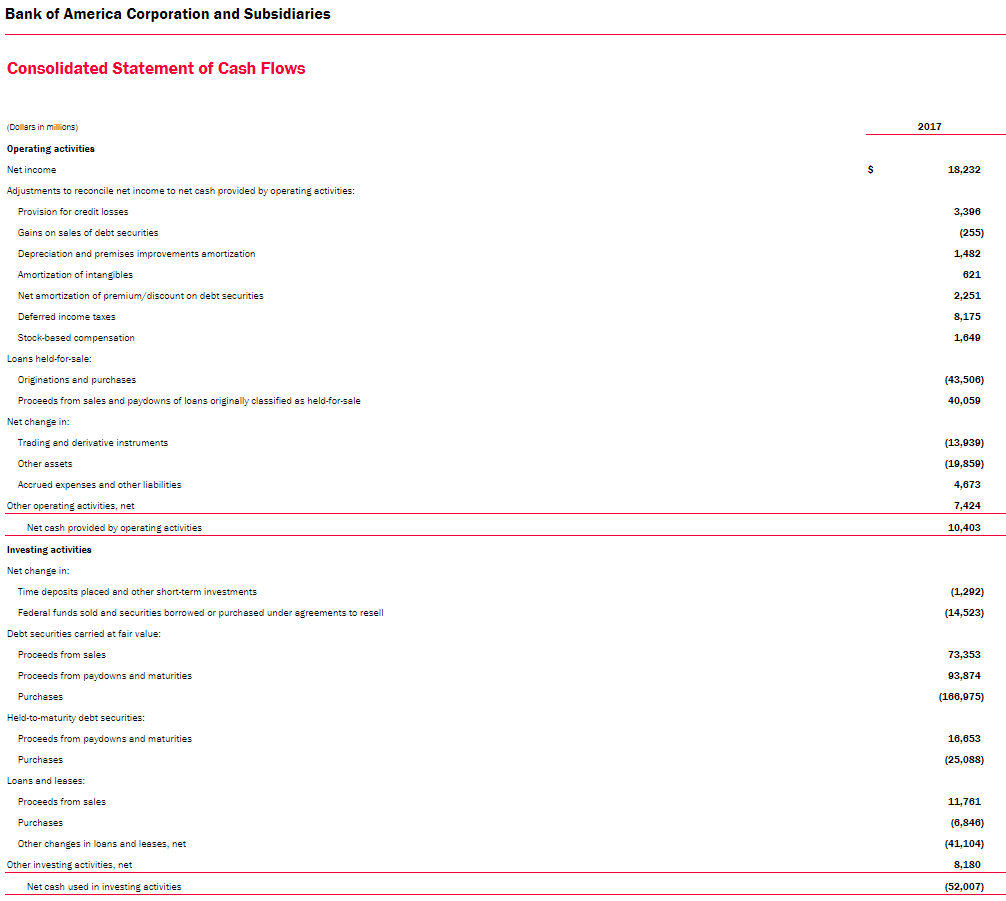

When to use P/FCF vs. P/E. FCF is not meaningful for certain industries such as financials given the nature of the business and therefore either earnings (P/E) or book value (P/B) should be used. For example, below is the most recent 10-K for Bank of America (NYSE: BAC ). As you can see, given the turnover in the balance sheet, the OCF and investing cash flow figures are not meaningful for any type of FCF analysis.

However, P/FCF is generally applicable for most companies (assuming they have positive FCF), and as stated above, this provides a better measure of the cash generating power of the business. Again, think about it this way - if you were going to purchase a business and the seller only lets you look at FCF or net income, which would you choose?

Conclusion

FCF and P/FCF are two of the best ways to measure the cash generating power and value of a company. By following these best practices, investors should have the most accurate picture of both.

See also The Theory Of Everything - Today's Editors' Picks on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}