Masimo MSA, a medical device company, has seen significant downward pressure on its earnings estimates over the last two months, downgrading the stock to a Zacks Rank #5 (Strong Sell), and indicating near-term weakness for the stock price.

Masimo is a medical technology company specializing in non-invasive patient monitoring solutions. Known for its innovative Signal Extraction Technology (SET), Masimo develops and manufactures a range of devices for monitoring vital signs, including pulse oximeters and continuous monitoring systems.

These technologies are widely used in healthcare settings to enhance patient safety by providing real-time and accurate data on parameters such as oxygen saturation, pulse rate, and other physiological indicators.

Although MASI stock has been a strong performer over the last decade, with a CAGR of 14.6%, there are numerous headwinds that leave the stock vulnerable to a sell-off in the near future. In addition to falling earnings estimates, the company also expects nearly flat sales growth over the next year, while also having a relatively high valuation.

Furthermore, stiff industry competition which is constantly creating comparable products as well as product reimbursement uncertainty compounds the risk in the stock going forward.

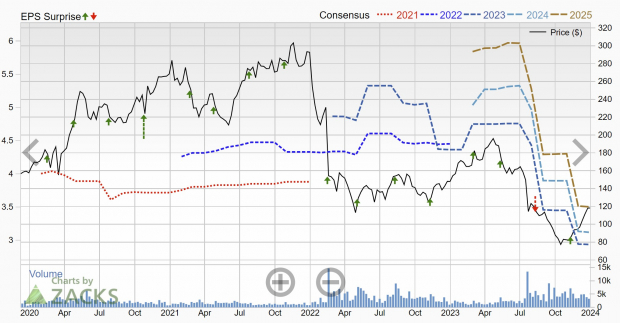

Cratering Earnings Estimates

The headwinds listed above have not been overlooked by analysts, as they have significantly lowered earnings estimates. In the chart below we can see just how severely earnings projections have been lowered since this summer, especially in FY25.

In just the last two months, current quarterly earnings estimates have declined by -40%, and are expected to fall -38% YoY to $0.82 per share. FY23 earnings estimates have been lowered by -14.8% and are forecast to decrease by -36% YoY to $2.94.

Image Source: Zacks Investment Research

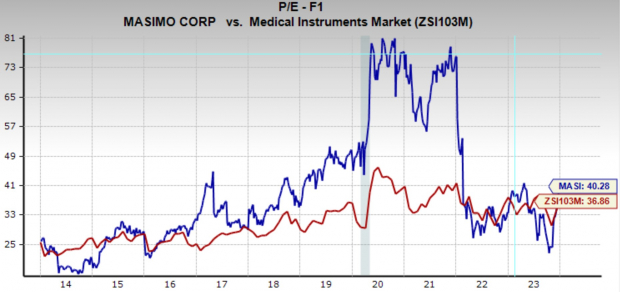

Premium Valuation

Even with these bearish catalysts, Masimo still boasts a relatively high earnings multiple. MASI is trading at a one year forward earnings multiple of 40.3x, which is above the industry average, market average, and its 10-year median of 33.8x.

Image Source: Zacks Investment Research

Bottom Line

Unfortunately for Masimo the current outlook is both not promising, and only worsened by its rich valuation. However, as patient monitoring is more important than ever, and with positive studies coming out for its products coming out there is still a potentially promising future for the company.

Nonetheless, until these near-term risk can current, investors should avoid Masimo stock, and look for opportunities elsewhere in the market.

Zacks Naming Top 10 Stocks for 2024

Want to be tipped off early to our 10 top picks for the entirety of 2024?

History suggests their performance could be sensational.

From 2012 (when our Director of Research, Sheraz Mian assumed responsibility for the portfolio) through November, 2023, the Zacks Top 10 Stocks gained +974.1%, nearly TRIPLING the S&P 500’s +340.1%. Now Sheraz is combing through 4,400 companies to handpick the best 10 tickers to buy and hold in 2024. Don’t miss your chance to get in on these stocks when they’re released on January 2.

Be First to New Top 10 Stocks >>MSA Safety Incorporporated (MSA) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.