IPG Photonics (IPGP) is a leading global manufacturer of high-performance fiber lasers and amplifiers, primarily used in materials processing, communications, medical, and advanced applications. The company is recognized for its innovation in fiber laser technology, which provides advantages such as higher efficiency, precision, and reliability compared to traditional lasers.

Founded in 1990 and headquartered in Oxford, Massachusetts, IPG Photonics serves a wide range of industries, including automotive, aerospace, electronics, and healthcare. Its products are used in applications such as welding, cutting, marking, and engraving, as well as in medical procedures and communications infrastructure. IPG Photonics has grown to become a dominant player in the fiber laser market, driven by its technological leadership and global reach.

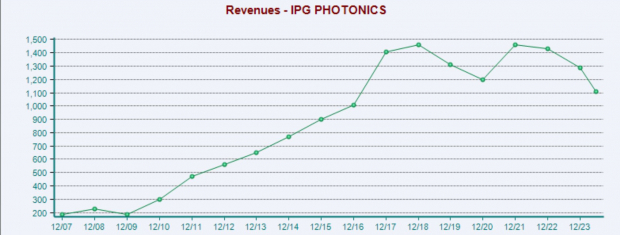

Despite its leading position in the market, IPG Photonics’ core business has struggled in recent years. Sales have been flat to contracting for six years now, while the stock performance is flat over that period as well. Furthermore, analysts have downgraded earnings expectations at IPGP, giving it a Zacks Rank #5 (Strong Sell) rating and the stock price is plunging to new lows. The downside risk is further complicated by its premium valuation, which may no longer be appropriate for a business with falling sales.

Based on these factors, it seems investors may want to avoid IPG Photonics stock until one or more of the variables turn more positive.

Image Source: Zacks Investment Research

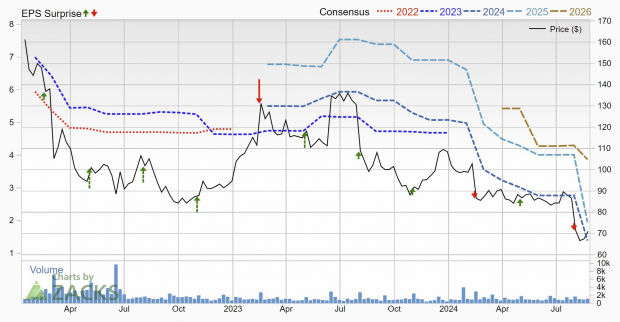

Photonics IPG Shares Down on Falling Earnings Estimates

The earnings revision trend at IPGP has absolutely plunged over the last month, reflecting analysts' concern for the business performance and giving it a Zacks Rank #5 (Strong Sell) rating. Analysts have unanimously lowered estimates across timeframes and by a significant margin.

Current quarter earnings estimates have been lowered by 76.2%, next quarter by 76.3%, FY24 by 50% and FY25 by 51.4%. Sales are also expected to fall 24.4% this year and then rebound by 5.8% next year.

Image Source: Zacks Investment Research

Photonics IPG Shares Trade at a Premium Valuation

Because of the collapse in earnings over the last few years, Photonics IPG’s earnings multiple has rocketed higher. However, it seems that the market has not yet discounted the low growth rates expected in the company, as this premium valuation appears unreasonable.

Today, IPGP is trading at a one year forward earnings multiple of 51.2x, well above its five-year median of 29.4x and the broad market average.

Image Source: Zacks Investment Research

Should Investors Buy Photonics IPG Stock?

Given IPG Photonics' struggles with flat-to-contracting sales and declining earnings, the stock faces significant headwinds. Analysts have sharply reduced earnings estimates and despite these challenges, the stock's premium valuation is difficult to justify for a business with declining growth.

For potential investors, the combination of deteriorating financial performance and an elevated valuation presents a high level of risk. Until the company can demonstrate a clear turnaround in sales growth and profitability, the stock may continue to face downward pressure.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>IPG Photonics Corporation (IPGP) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.