Fox Factory Holding Corporation designs, engineers, and manufactures performance-defining products and systems worldwide. The company provides its products for high-end bicycles and a variety of powered vehicles including on-road, off-road, all-terrain, snowmobiles, and military trucks.

In addition, Fox offers lift kits and components, rear suspension products, tuning services, as well as wheels and accessories. The company also serves aftermarket products under brands such as BDS Suspension, Zone Offroad, JKS Manufacturing, FOX, and Marzocchi.

Amid an intensifying and competitive environment, Fox faces challenges with OEM partners reducing their demand forecasts, impacting revenue. The company anticipates ongoing pressure on demand in 2025 as a difficult retail environment is expected to linger.

The Zacks Rundown

Fox Factory Holdings FOXF, a Zacks Rank #5 (Strong Sell) stock, is a component of the Zacks Automotive – Domestic industry group, which currently ranks in the bottom 48% out of approximately 250 Zacks Ranked Industries. As such, we expect this industry group as a whole to underperform the market over the next 3 to 6 months.

Stocks in the bottom tiers of industries can often be intriguing short candidates. While individual stocks have the ability to outperform even when they’re part of a lagging industry, the inclusion in a weaker group serves as a headwind for any potential rallies and the journey forward is that much more difficult.

Along with many other automotive-related stocks, FOXF shares have been underperforming this year while the general market returned to new heights. The stock is hitting a series of lower lows and represents a compelling short opportunity as we approach the New Year.

In the latest quarter, Fox stated that both its biking and powered vehicle segments were weaker than anticipated as excess inventory among manufacturers was reduced. As we’ll see, the company reported earnings below expectations and lowered full-year EPS guidance.

Recent Earnings Misses & Deteriorating Outlook

Fox Factory Holdings has fallen short of earnings estimates in three of the past five quarters. Back in October, the company reported third-quarter earnings of 35 cents per share, missing the $0.42/share Zacks Consensus Estimate by -16.7%.

Fox’s gross margin decreased to 29.9% from 32.4% in the same period last year, driven by shifts in the product offering and reduced operating leverage. Net income for the quarter plunged to $4.8 million from $35.3 million during the year-ago period. Revenues of $359.12 million also missed the Zacks Consensus Estimate by -2.02%.

Consistently falling short of earnings estimates is a recipe for underperformance, and FOXF is no exception.

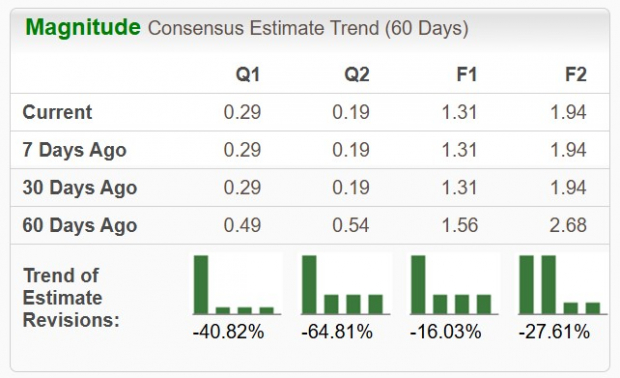

The company has been on the receiving end of negative earnings estimate revisions as of late. Looking at the current quarter, analysts have slashed estimates by a whopping -40.82% in the past 60 days. The Q4 Zacks Consensus EPS Estimate is now $0.29/share, reflecting negative growth of -39.6% relative to the same quarter in the prior year.

Image Source: Zacks Investment Research

Falling earnings estimates are a huge red flag and need to be respected. Negative growth year-over-year is the type of trend that bears like to see.

Technical Outlook

As illustrated below, FOXF stock is in a sustained downtrend. Notice how the stock has made a series of lower lows, widely underperforming the major indices. Also note that shares are trading below downward-sloping 50-day (blue line) and 200-day average (red line) moving averages – another good sign for the bears.

Image Source: StockCharts

FOXF stock has experienced what is known as a “death cross,” whereby the stock’s 50-day moving average crosses below its 200-day moving average. The stock would have to make an outsized move to the upside and show increasing earnings estimate revisions to warrant taking any long positions. Shares have fallen more than 50% this year alone.

Final Thoughts

A deteriorating fundamental and technical backdrop show that this stock is not set to make its way to new highs anytime soon. The fact that FOXF is included in one of the worst-performing industry groups provides yet another headwind to a long list of concerns. A history of earnings misses and falling future earnings estimates will likely serve as a ceiling to any potential rallies, nurturing the stock’s downtrend.

Potential investors may want to give this stock the cold shoulder, or perhaps include it as part of a short or hedge strategy. Bulls will want to steer clear of FOXF until the situation shows major signs of improvement.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Fox Factory Holding Corp. (FOXF) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.