In the battle of wireless provider powerhouses, the stock market appears to have a new clear-cut favorite in AT&T (NYSE: T). This earnings season, its stock once again separated from rival Verizon Communications (NYSE: VZ), as investors cheered AT&T results while sending shares of Verizon lower. AT&T's stock is now up about 32% on the year compared to only about a 11% gain for Verizon.

Let's take a closer look at AT&T's Q3 results to see if the momentum can continue or if it is time to switch to Verizon.

Robust subscriber additions

AT&T continues to see strong subscriber growth both in its wireless and broadband businesses.

In the third quarter, the company added 429,000 retail postpaid subscribers, including 403,000 retail postpaid phone additions. This helped power a 4% increase in Mobility service revenue to $16.5 billion. Overall Mobility revenue rose 1.7% to $21.1 billion as equipment sales fell 5.7% to $4.5 billion. Postpaid phone average revenue per subscriber (ARPU), meanwhile, increased 1.9% to $57.07.

Broadband growth was also strong, with AT&T adding 226,000 fiber subscribers and 135,000 Internet Air subscribers additions. The company lost 198,000 non-fiber subscribers as they continued to switch to faster options. Overall, the company ended the quarter with 9 million fiber subscribers, up from 8 million a year ago.

Meanwhile, broadband ARPU increased by 5.1% to $68.25, while fiber APRU rose 3.2% to $70.36. This led to fiber revenue jumping 16.9% in the quarter to $1.8 billion, while total consumer broadband revenue rose 6.4% to $2.8 billion.

Not every business was performing well for AT&T. Its prepaid wireless business was hurt by the end of the Affordable Connectivity Program (ACP) this spring, as it lost 45,000 prepaid subscribers. The government program helped subsidize internet services to lower-income households. AT&T's wireline business, meanwhile, saw its revenue sink 11.8% year over year to $4.6 billion.

Total revenue fell 0.5% to $30.4 billion, while adjusted EPS dropped from $0.64 to $0.60.

AT&T produced $5.1 billion in free cash flow in the quarter, which is more than double the $2 billion in dividends it paid out. AT&T held its $0.2775 quarterly dividend steady since May 2022. The stock currently has a forward dividend yield of about 5%.

Looking ahead, AT&T maintained its full-year guidance. It is looking for full-year wireless revenue growth of approximately 3% and broadband revenue growth of 7% or more. It continues to expect adjusted EPS in the $2.15 and $2.25 range, with adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) growth of about 3%. Free cash flow is projected to come in between $17 billion to $18 billion for the year.

Image source: Getty Images.

Can AT&T's momentum continue?

The divergence between AT&T and Verizon's stocks this year and the investor reactions to their earnings is actually quite puzzling, as the companies are seeing very similar tailwinds and headwinds in their businesses. Both companies have been seeing strong postpaid wireless and broadband subscriber growth, while prepaid and wireline have is dragging. For example, Verizon added 349,000 retail postpaid net subscribers this past quarter and 389,000 broadband subscribers.

Meanwhile, Verizon slightly increased overall revenue thus far this year, while AT&T saw small declines. Nonetheless, the latter's stock has performed much better. At the same time, Verizon has continued to increase its dividend, while AT&T continues to keep it unchanged.

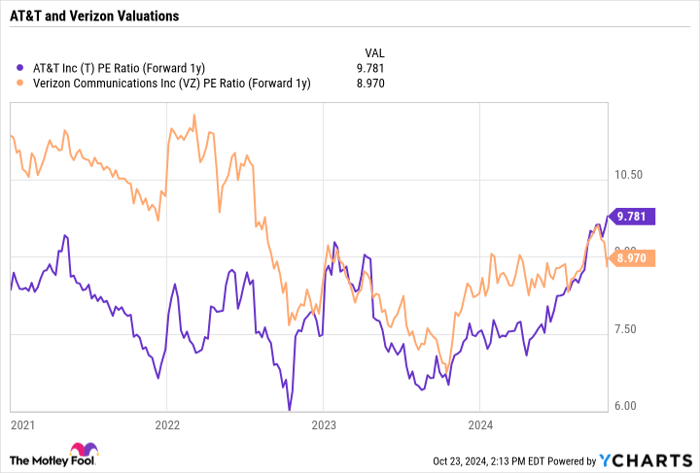

AT&T's strong stock performance now leaves it with a forward price-to-earnings (P/E) multiple of about 9.8 based on 2025 earnings estimates, which is above the under 9 times multiple of Verizon. Until recently, Verizon has historically commanded the higher multiple.

T PE Ratio (Forward 1y) data by YCharts

With both companies producing very similar results and Verizon's valuation now cheaper, I would prefer its stock over AT&T at the moment. I think both companies are doing good jobs with their core wireless and broadband businesses, but I see no reason why AT&T's stock has outperformed Verizon's by such a wide margin this year.

As such, I'd consider AT&T more of a hold after its big move and Verizon a buy.

Should you invest $1,000 in AT&T right now?

Before you buy stock in AT&T, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and AT&T wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $860,447!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 21, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool recommends Verizon Communications. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.