Even though Halloween is over, I can't help but take note of some spooky themes still around me. No, I'm not talking about ghosts or monsters. Rather, I'm talking about all the red I'm seeing in the markets lately.

Third-quarter earnings season kicked off, and the presidential election is at hand. All of this uncertainty is manifesting through a series of sell-offs in the stock market, and I don't like it!

But one stock that's been holding up quite well is artificial intelligence (AI) giant and "Magnificent Seven" member Alphabet (NASDAQ: GOOGL) (NASDAQ: GOOG). Following an impressive earnings report on Oct. 29, shares of Alphabet popped as much as 10%.

Below, I'm going to explore key areas of the company's third-quarter earnings and assess if now is a good time to scoop up shares.

What is fueling Alphabet stock?

For the three months ended Sept. 30, Alphabet reported $88.3 billion in revenue -- representing an increase of 16% year over year on a constant currency basis. What's even better is that Alphabet's operating income grew by 32% year over year to $28.5 billion, while the company generated $17.6 billion of free cash flow.

Alphabet's largest source of revenue and operating profits stem from the company's enormous advertising business-underscored by Internet search tool Google and video-sharing platform YouTube. While sales from both Google and YouTube each grew 12% year over year during the third quarter, it's important to note that advertising spending in general is up across social media platforms because of the presidential election.

The more subtle winners for Alphabet over the last few months are the company's progress in subscription services as well as cloud computing. Google Cloud Platform (GCP) was Alphabet's fastest-growing business -- increasing sales by 35% year over year to $11.4 billion.

Naturally, management attributed Google Cloud's growth to progress in generative AI. Alphabet CEO Sundar Pichai stated that the company's "technology leadership and AI portfolio are helping us attract new customers, win larger deals, and drive 30% deeper product adoption with existing customers."

Alphabet is integrating AI across its entire suite of services -- from search, video content, productivity tools, cybersecurity, and more. This approach is helping Alphabet build a stickier platform overall as customers embrace using the company's AI-powered products and services as a major part of their broader infrastructure.

Image source: Getty Images.

Looking at Alphabet's valuation

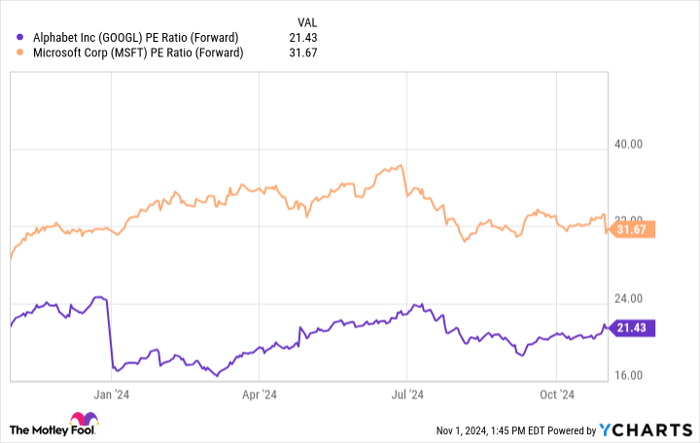

The chart below benchmarks Alphabet against one of its biggest rivals, Microsoft, on a forward price-to-earnings basis (P/E). In case you are wondering, I purposely omitted Amazon from this cohort. Amazon's earnings and profitability are far more volatile than those of Microsoft or Alphabet, and I don't personally see much competitive overlap between Amazon and Alphabet besides cloud computing.

GOOGL PE Ratio (Forward) data by YCharts

It's easy to see that investors are placing a significant premium on Microsoft compared to Alphabet. Furthermore, Alphabet's forward P/E of 21.4 is actually nominally below the average estimate of the S&P 500 index, which cites around 23. This disparity could suggest that investors believe Alphabet's near-term returns are actually less attractive to that of the broader market.

Considering Alphabet's current growth and its rising position in the AI landscape, these valuation discounts might seem out of place. However, there are reasons why these disparities among valuation multiples might make some sense.

Some things to consider

Although Google and YouTube remain two of the world's most visited platforms, Alphabet is not without competition.

Meta Platforms boasts 3.3 billion daily active people (DAP) across Instagram, Facebook, and WhatsApp. This surface area is enormous, and each platform represents a lucrative alternative to Google or YouTube for advertisers. Moreover, TikTok rose in popularity in recent years -- especially among younger demographics.

In addition, ChatGPT recently launched a new search tool that could wind up being a headwind for Alphabet in the long run. If ChatGPT manages to lure users away from Google, it could be detrimental to the company's advertising value proposition. Furthermore, considering Microsoft has an equity stake in ChatGPT, the company could potentially benefit from its own search functionality, Bing, if users start to abandon Google.

Even though Alphabet stock might appear like a bargain, there are actually quite a few unknowns surrounding the company's long-run potential. This uncertainty is playing a role in Alphabet stock's discounted valuation compared to peers'.

Should you invest in Alphabet? On the one hand, the company is showing notable strides across core product offerings supported by investment in AI. But on the other hand, the competitive landscape is intensifying across the company's biggest sources of sales and profits.

For these reasons, I think I would pass on Alphabet for now but continue monitoring the stock as the AI narrative continues to unfold.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,050!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,999!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $407,440!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 4, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.