By Kylie Purcell

A few years ago, robo-advisors were the talk of the investment industry. Billed as the answer to costly financial advice, robo-advice platforms use standardized risk assessment tools to pair you with an investment portfolio — typically composed of ETFs.

By removing the human advisor component, they promised to revolutionize the industry by making long-term investing and financial planning cheaper and more accessible to the masses.

Now, there are signs the robo-advice industry might be losing steam — at least in its current form.

Around 35% of adults in the U.S. have used a robo-advisor, according to new survey data from Finder.com. But of those, slightly more than half have chosen to opt-out — 17% who actively use a robo-advisor v.s. 18% who no longer do.

The reasons are unclear, but some experts believe the lack of human engagement is a bigger barrier than many had perceived.

Losing Steam?

Last year, the sale of BlackRock's robo-advisor platform FutureAdvisor to Ritholtz Wealth Management sent ripples through the industry.

Hailed as a promising venture in 2015, the sale of FutureAdvisor by one of the world’s biggest asset managers brings to question the role and profitability of the sector.

The growth numbers seem to support this picture.

Robo-advisor funds under management are projected to reach $2.76 trillion globally by the end of 2023. But growth has been on a largely downward trend for half a decade — and is expected to slow substantially in the next few years, according to a new report by Statista.

In 2021, assets under management grew by over 65% — in 2023, growth is predicted to fall to 12.5% and just 8% by 2027.

Australia, which has around half a dozen robo-advisors today, has seen at least five robo-advisors close doors in as many years

And in July this year, one of the country’s earliest and most popular robo-advisors, Six Park, announced it was winding down after just 8 years in business due to difficult market conditions.

Still a Need

Patrick Garrett, cofounder and CEO of the recently defunct Six Park, believes unclear regulation around advice services, rather than changing consumer demand, has hindered the growth of robo-advice.

“There remains an enormous unmet need for the mass market that cannot afford full-scale financial advice to be able to access an affordable investment management service.”

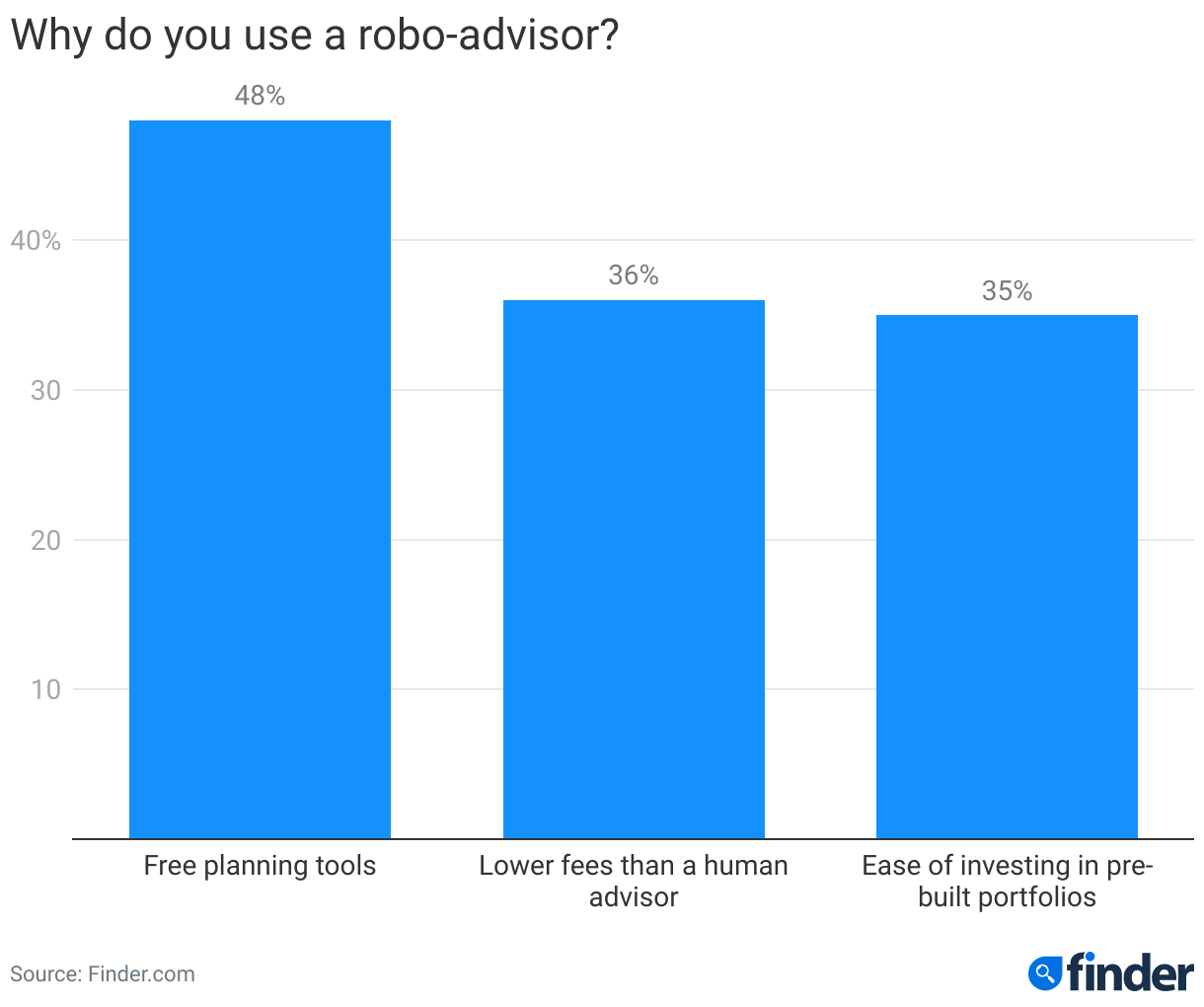

Of those who actively use Robo-Advisors in the U.S., 36% say they do so because they’re cheaper than a human advisor, while 35% say it’s the ease of investing in pre-made portfolios, according to Finder’s survey results.

“With investing, simpler is typically more effective than “tinkering,” and robo-advice utilizes the combination of technology and the simplicity of ETFs (exchange-traded funds) along with proven methods of portfolio management.”

Six Park’s closure came once it was unclear that the adoption of robo-advice would reach levels needed to scale, according to Garrett. The robo-advisor had attempted to partner with larger wealth and financial advice services to reach new clientele in the lead-up to its closure, but this did not materialize.

“The combination of a challenging funding environment and incumbents’ lack of willingness to work with fintechs (robo-advice in particular) to accelerate scale remains a headwind,” said Garrett.

Are Hybrid Advice Models the Future?

Despite the lack of uptake, the future of robo-advice might lie somewhere in the middle of full automation and conventional wealth management.

Banking goliath JP Morgan seems to think so — in November last year, it launched its own hybrid robo-advisor that gives investors access to digitally-led portfolios alongside human financial advice via video conferencing.

Customers get at least one session with a human advisor who recommends a portfolio. However, the portfolio is automatically rebalanced going forward — unless further personal advice is requested.

The idea is by partnering robo-advice technology with full-service advisors — in other words, firms that offer human advisors — investors can get the best of both worlds: low-cost financial advice paired with human interaction.

At the same time, both sectors get access to a bigger client pool.

Speaking at a wealth conference last year, JP Morgan’s then head of product Kelli Keough said the wealth sector had overestimated the demand for purely digital advice, as reported by the Financial Review.

“I think we forgot for a moment how emotional and important money is to individuals and how [important it is] having somebody to speak with,” said Keough.

Instead, she believes the answer lies in the hybrid advice model — which she says has seen an uptick in the US, even as traditional robo-advice growth has slowed.

JPMorgan isn’t the first to trial the hybrid-type model.

Popular robo-advisor Betterment added a human advice component back in 2017. To access the ongoing personal planning services, you need a balance of $100,000 and are charged 0.40 percent of your portfolio.

Similarly, Vanguard Personal Advisor customers can opt for a fully digital advice service, a hybrid model or get a dedicated personal advisor. Like Betterment, fees are charged as a percentage of your funds — with the minimum balance starting from $3,000 to $500,000 for a dedicated advisor.

While the personal advice options through these hybrid platforms may still be out of reach for many, they create a pathway that could feasibly support an investor’s lifespan.

Pure play low-cost robo-advisors might be attractive to a certain point, but once a certain level of wealth has been accumulated, it’s understandable they’ll want a more nuanced approach that considers their personal circumstances.

“Consolidation can be a very good thing,” Garrett explained. “When a fintech has built a proven service to solve a problem — investment help for the mass market — and aligns with a larger entity that can put such a service in front of a much larger audience in need.”

About the author:

Kylie Purcell is an Investments Analyst at Finder and a leading investments commentator. Kylie has over a decade of experience in analyzing and presenting market updates, with expertise in all areas of investments, while specializing in financial products, including online trading platforms, robo advisors, stocks and ETFs, as well as digital assets and cryptocurrencies such as Bitcoin.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Finder

Finder is a global financial technology platform which allows members to save, invest and spend via the Finder mobile app and website. Finder’s mission is to help people make better financial decisions and work with partners to connect via API into the Finder platform to offer saving and investment services and products. Finder was founded in Australia in 2006 and now operates in 50+ countries with 2,600+ product partners and 10+ million visits every month, serviced by 500+ crew passionate about helping our members achieve their full financial potential.

Read Finder's Bio