News & Insights

In 2019, we looked at all-in costs to trade on exchanges for the first time.

A lot has changed since then — we have more exchanges, and many of them have started to diversify their product revenues. So this year, we also look at industry-wide costs over the years.

The good news is average costs are down. The bad news is we also see some costs of fragmentation for the sake of venue competition.

As the charts below detail, we see:

- Average costs per trade are falling, thanks to volumes increasing, while many exchange costs remain unchanged despite inflation.

- Somewhat offsetting that trend is overall costs rising.

- We see that explicit exchange fees vary significantly – in their makeup and their totals.

- We also show that different business models contribute differently to market quality.

- We also find that exchanges with the most expensive trading costs have the highest fees. This shows that if a venue can segment markets so traders can be more profitable, they can raise explicit trading costs.

Updating our all-in costs to trade

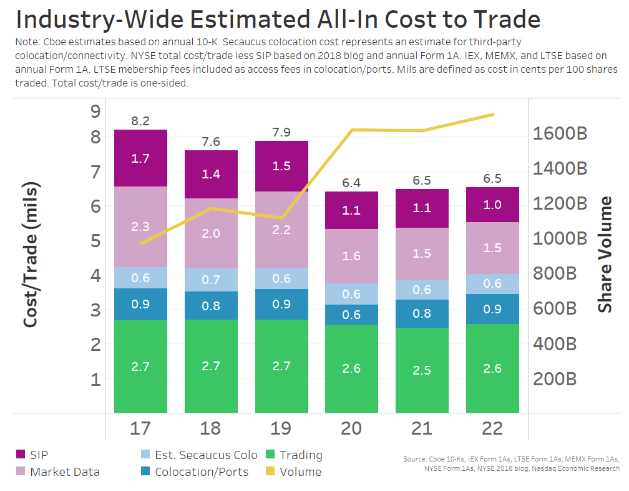

We start by looking at industry-wide all-in costs to trade from 2017 to 2022 (Chart 1).

Using Form 1 and 10-K data for each exchange, we add up the revenues earned across the market and divide by the shares traded on those exchanges (Although, again, we were unable to parse equity trading costs from MIAX regulatory filings).

Results are two-sided, as every trade has a buyer and a seller. After some accounting estimates, including separating options revenues from stock revenues, we are also able to show this broken down by revenue type.

There are two key insights:

- The all-in cost to trade today has been significantly lower since 2017. That would seem mostly due to the increase in volumes traded (yellow line), especially since Covid, while fees have mostly been unchanged.

- However, there is an underlying trend offsetting the volumes increasing. Especially since 2020, costs to trade have been edging higher — mostly due to new venues diversifying their revenue base.

Chart 1: After seeing a structural shift lower, fragmentation is pushing costs higher

New exchanges and economic realities driving costs higher

What changed in 2020 to cause underlying costs to rise?

Notably, in just the last few years, competition for venues has clearly increased. Three new exchanges have entered the already highly competitive stock market field. The Long-Term Stock Exchange launched in 2019, followed by MEMX and MIAX Pearl in 2020. We now have 16 exchanges.

All of these venues added fixed costs to the industry. In addition to the costs, we estimate above are the investments brokers need to make in routing and capacity in their own data centers.

In addition, the “free” stuff (data, membership or co-location) many offered in order to reach economies of scale led to losses. Over time, the charges are increasing for these joint products, with some realizing the economic inefficiencies “free” creates (overuse and unnecessary expenses). For example:

- MEMX initially didn’t charge for membership, connectivity or market data when it launched, though it added those fees last year.

- IEX has slowly added fees for connectivity and some market data, too.

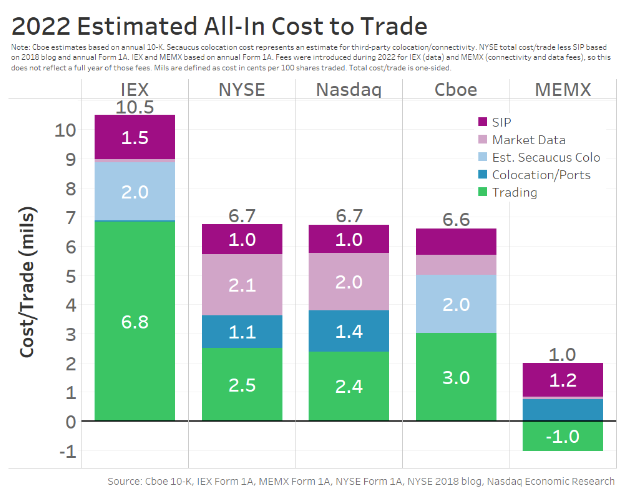

Chart 2: The mix and level of all-in costs varies significantly by exchange group

The largest exchanges have essentially equal costs to trade

Interestingly, based on our estimates, all-in costs to trade on NYSE, Nasdaq and Cboe group are close to equal.

Given these exchanges account for 89% of all exchange trades, this would seem to indicate that competitive market forces stop a large exchange from charging too much “in total” – regardless of how they decide to split trading, co-location and data costs in order to attract their preferred blend of customers.

Note that Cboe doesn’t earn co-location revenues because they don’t control their own data center. But brokers will still need to install hardware and pay rent to the data center owners in the Secaucus area, so we have added an estimated cost for that to keep things consistent for comparison purposes.

How can the most expensive exchanges compete?

In contrast, the data also shows that IEX remains the most expensive exchange, with trade costs over 55% higher than NYSE, Nasdaq or Cboe.

That raises the question – if the market is competitive on an all-in-cost basis - how can IEX hold market share when it’s been the most expensive exchange by far year after year?

The answer is that explicit costs aren’t all that matters.

As we all know, IEX has a speed bump that allows its liquidity providers to avoid filling market-wide ISO sweep orders (see Chart 3). Avoiding those executions does three things:

- Reduces actual market-wide liquidity at the NBBO, below what is quoted.

- Increases opportunity costs for spread crossing orders.

- Reduces adverse selection for IEX’s liquidity providers.

The third point is important – as it increases trading profits for customers, which helps offset the explicit exchange fees IEX charges them to trade. That has also allowed IEX to remain one of the few “fee-fee” trading venues where buyers and sellers both pay fees to trade (although, as of Sept. 1, IEX is now paying rebates).

That, in turn, attracts market makers to quote, which increases SIP revenues paid to IEX, which doesn’t necessarily add to tradable liquidity or price discovery (given those limit orders are able to reprice (fade) as the NBBO changes on other venues).

The important point here is that exchanges not only compete on all-in-explicit costs but also on the trading profits they are able to create for their customers.

Trading fees alone can be different

Of course, when we focus on just the trading costs, those costs represent the net of buyer and seller exchange fees. As many know, most exchanges rebate the buyer or seller of each trade:

- Receiving a rebate for liquidity provision (so-called maker-taker markets)

- Paying for queue priority (so-called inverted fee markets)

- Charging both sides of the trade (a fee-fee model)

The fees change the economics of trading in some important ways, as we show in Chart 3.

- Inverted markets that charge a liquidity provider to post result in less spread capture when a market maker actually trades with a buyer and a seller (as they capture spread but pay fees on both trades). However, for a spread crossing order, the rebate they earn makes those markets economically cheaper to route to. That effectively makes those limit orders more likely to trade first, which makes spread capture more likely, which can make it worth paying for queue priority for the liquidity provider.

- Maker-taker markets are often more attractive to liquidity providers, and typically have more liquidity, as they pay a rebate on top of the spread capture. However, as we see in Chart 3, they are more expensive for spread crossers to trade (because they are charged a fee to trade). That, in turn, means those markets are more likely to trade last at each price level, resulting in a higher chance the price changes after the fill (known as adverse selection). Adverse selection is a cost for a market maker, as they can no longer capture spread. However, rebates help to offset that adverse selection.

- Fee-fee models, of course, are a more expensive choice for a liquidity provider and a spread crossing order; however, when combined with a speed bump, that allows the offer to fade as the NBBO changes (due to the ISO order in Chart 3) avoiding adverse selection adds to trader profits in a different way.

Chart 3: Different exchange economics affect spread capture and adverse selection

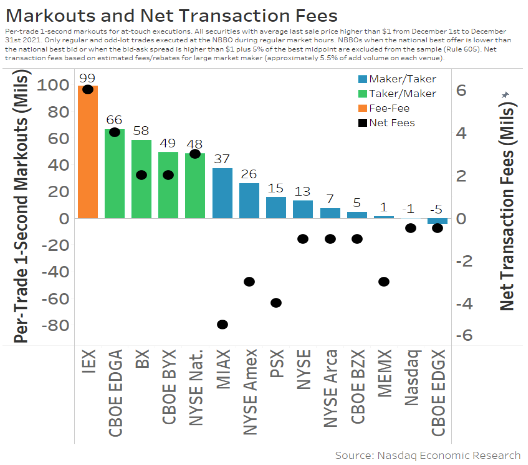

Ranking exchanges by trader profits and net fees prove profits matter

We can see the theoretical results above play out in real life, too.

In Chart 4 below, we look at theoretical market maker profits (markouts, bars) versus net trading fees (black dots). This shows three important facts:

- The expected order of profitability from trading (from Chart 3) holds – with speed bumps providing the best returns, followed by inverted markets (green), and then maker-taker markets (blue)

- The markets with the highest net trading profits also have the highest fees (black dots).

- Headline rates for maker-taker markets are negative, indicating those exchanges are contributing financially to encourage market makers to make better NBBO quotes, which creates tighter spreads (and also helps earn offsetting SIP revenues).

Importantly, this chart doesn’t show the quote quality, like the percentage of time the venues are actually on the NBBO or what the breadth of quoting and average spreads are. For that, see Table 1.

Chart 4: Higher-cost venues compete by having better markouts

Exchange trading fees impact market quality differently

As we’ve discussed before, when you take both explicit and implicit costs to trade into account, recent research shows that the all-in-execution costs are largely equalized across exchanges. The additional spread capture from inverted venues less the costs to post is roughly equal to the rebates less the adverse selection on a maker-taker limit order.

However, exchange fees matter, perhaps much more, in other ways.

As the data in Table 1 shows:

- Listing markets have a much bigger focus on market quality (time at NBBO and breadth of the market at NBBO are high, and spreads are low). This is mostly achieved via rebates for liquidity providers (Column 11) and negative capture on trading fees as a reward for those market makers setting competitive markets. As we’ve noted before, tight spreads are important for issuers, as they help reduce costs of capital – and issuers are only clients of listing exchanges.

- Other markets with good market quality tend to be maker-taker markets, too. Rebates for passive limit orders encourage tight spreads that benefit the whole market and all investors by setting lower spread costs for all venues. Data suggests tight NBBO spreads could save investors billions of dollars each year.

- Inverted venues can save investors in other ways, as we discussed above. Data shows they capture more spread (Column 9). Queue priority means they can trade faster, even on the passive side of the spread. However, the breadth of quotes is lower (Column 7) and competitive quotes at NBBO are far less reliable (Column 6), resulting in those venues contributing little to NBBO or spreads.

Table 1: Trading fees vary significantly across exchanges and result in different market quality and trader profitability

Based on this data, we could say that there are four main exchange business models in the U.S. – market quality, queue priority, speed bump, and market maker (Column 2). The market-maker exchanges also use the maker-taker pricing model; however, they are different because profits and losses are retained by the owners, who are industry participants – compared to public exchanges where investors benefit from exchange profits and dividends.

Some industry costs provide market-wide benefits

This data shows that all-in exchange fees seem to be competitively constrained, and average costs per trade keep falling. But we see that all-in-economics to trade are much more important – with customer profits due to different market engineering giving some exchanges more pricing power than others.

But this shouldn’t be all about exchange competition and their (public) costs.

Lit prices and competition for the NBBO are important, too. In fact, the positive economic benefits investors receive from tighter spreads might be even larger than the costs we’re looking at here.

Michael Normyle, U.S. Economist at Nasdaq, contributed to this article.

Latest articles

This data feed is not available at this time.

Data is currently not available

Market Makers Newsletter

Sign up for our newsletter to get the latest on the transformative forces shaping the global economy, delivered every Thursday.