The past few years have witnessed an unprecedented expansion of artificial intelligence (AI) into various aspects of life. Cashing in on this expansion, companies involved in this space are most certainly at the forefront of the next big thing in AI applications.

Of all the key players, Nvidia (NASDAQ: NVDA) has clearly been the one to watch, gaining a jaw-dropping 2,300% increase over the past five years (at the time of this writing), cementing its position as one of the most remarkable growth stories in the technology space. Importantly, investors have been eager to capitalize on its success as the company rides the AI wave with chips for data centers and graphics.

The stock's 199% one-year return is a testament to its continued relevance in the artificial intelligence space, fueled by the explosive demand for GPUs (graphics processing units) that help power AI models. These are now integral to industries ranging from cloud computing to finance and healthcare. With companies scrambling to integrate AI into their operations, Nvidia's products are in high demand, and the company has positioned itself well to be the key supplier for the graphics side of infrastructure.

But with its stock now trading near all-time highs, and at a decent premium, the question is whether Nvidia stock's rally is done for a while, or is there still plenty of room left to run?

Supply versus demand equation

As fellow Fool writer Adria Cimino pointed out, Nvidia is sitting on 80% market share for its products. That's a pretty pleasant spot to be in.

Nvidia's graphics cards are the backbone of many AI systems, and as demand for AI technology surges, the need for these graphics cards becomes even more useful. Digitaltrends.com has warned that there is likely to be a GPU shortage, especially for gamers. This supply and demand imbalance creates a unique opportunity for Nvidia. As long as the demand for AI and machine learning chips continues to grow and supply remains constrained, this stock should remain strong. This is heavily demonstrated by how quickly Nvidia's revenues took off in fiscal 2024 compared to fiscal 2023. Companies need their GPUs.

Financials continue to impress

The company's most recent stats are what you dream of in a growth stock. On a GAAP basis, Nvidia's most recent quarter saw year-over-year revenue growth of 94% to $35.08 billion. Nvidia also had earnings growth of 111% year over year to $0.78 per diluted share, equal to roughly $19.3 billion.

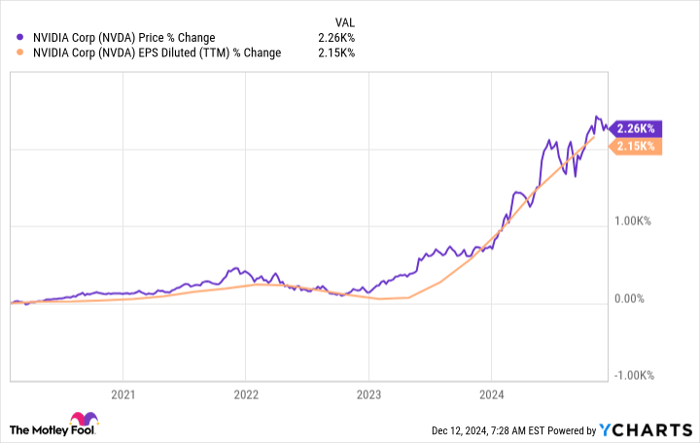

I often put a big emphasis on earnings, and rightfully so, as they are the backbone of long-term stock performance. In the instance of Nvidia, I certainly still care about the earnings potential and overall revenue growth potential, as the two coincide over the long term. The below chart confirms that: Over the last five years, Nvidia's stock price actually grew almost lock step with its GAAP earnings per share.

But one of the big things I loved about Nvidia's third-quarter results was its fourth-quarter GAAP estimates on margins, which the company anticipates to be 73%. This is a high-margin business, and I love it!

Is Nvidia's ride done?

The short answer? No way. To reiterate my earlier point, the unprecedented expansion of AI means it's not going anywhere.

The factors here are many. If you look in Nvidia's third quarter press release, you'll see announcements in new areas of growth including launching a supercomputer in Denmark that run on over 1,500 Nvidia GPUs, the introduction of an AI aerial platform that has already begun working with T-Mobile, Ericsson and Nokia, along with Nvidia computing being used in things like new Volvo SUVs. That's just to name a few of a very broad list of areas in which Nvidia's resources are being allocated.

Looking ahead, Wall Street analysts are expecting Nvidia to finish fiscal 2025 with $2.95 per share. That would give it a forward P/E ratio of 47.2 times fiscal 2025 earnings. Now, when you consider that something like Tesla trades at almost 100 times earnings, or Cava, a stock I love by the way, trades at over 300 times earnings, a premium of 47 times earnings for Nvidia shares doesn't seem that extreme given the long-term potential and its current dominance within its space.

This is a company that is far from done. In fact, the best years for Nvidia are very likely in the future. My recommendation is to not be afraid to buy at current levels.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $348,112!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,992!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $495,539!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 9, 2024

David Butler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Tesla. The Motley Fool recommends Cava Group and T-Mobile US. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.