News & Insights

Short selling is one of those features of the market that companies tend to dislike, but for arbitrageurs and market makers, it is an absolute necessity.

The fear for companies and investors is that short sellers make stock prices go down. That, in turn, makes it harder for companies to raise capital if they need it in the future and harms existing investors’ returns.

However, as we discuss today, U.S. regulators have put a number of rules in place to limit short selling — from disclosures to trading limitations.

Today, we look at those rules, what the data shows and how short selling really works.

What is short selling?

Quite simply, short selling is selling a stock that you don’t already own.

There are rules in place to require a stock to be borrowed so settlement can occur without fail. That also adds ongoing finance and borrowing costs to investors holding short positions.

Who is short selling?

There are a number of reasons to short, which starts to teach us about “who” is short selling.

Data from an earlier report (Chart 1) showed that the majority of investors in the market are mostly “long only” investors. However, the same report estimated that the majority of trading was being done by intermediaries – despite their net assets appearing to be small.

The stock market ecosystem needs both to be efficient.

Chart 1: A high proportion of market liquidity is intermediaries keeping markets efficient

For example:

- Market makers, who are continuously providing bids and offers on stocks, may trade with a buyer first, leaving them short. This makes it easier for a buyer to find a seller and keeps bid-offer spreads tighter.

- Statistical arbitrageurs typically buy and sell related stocks due to short-term relative performance. These strategies can help mutual funds buy large orders, as statistical arbitrage transfers liquidity from similar stocks into the stock the mutual fund is trying to buy.

- Futures or ETF arbitrage helps keep ETF prices in line with underlying stock values, ensuring investors pay a fair value when they buy an ETF or Future for stock exposure.

- Options market makers for both on-exchange options and OTC derivatives that use ISDAs need to dynamically hedge their positions, increasing or decreasing hedges in underlying stocks over time.

The fact that most of these strategies hold small net positions means they are buying offsetting positions quickly – not building large short positions.

In short (pun intended), a lot of short selling is done by liquidity providers, arbitrageurs and market makers. In most cases, their strategies keep markets more efficient and spreads tighter – without having a directional or long-term view on the stock. That, in turn, translates into a lower cost of capital for companies.

What about longer-term holders, like hedge funds?

Of course, longer-term investors who think a stock is overvalued can also short the stock, hoping to buy it back later once the price has fallen. Based on Chart 1, that is most likely done by hedge funds.

Based on industry data, we estimate hedge funds trading U.S. stocks have net assets of around $1.5 trillion. Of course, hedge fund positions are hedged and usually levered. The leverage ranges depend on the strategy.

Based on a variety of sources, we guesstimate that hedge fund gross U.S. stock exposures may be around $3.6 trillion, of which short positions would add to $1.0 trillion. That also means that although hedge funds do short stocks, they are typically net-long (that’s why the left circle in Chart 2 below is larger).

Chart 2: Estimated hedge fund assets — long and short — by strategy

Only dedicated short funds are focused on only shorting companies based on a view that those companies have weak fundamentals. Our estimates suggest they account for less than 1.3% of all hedge fund positions.

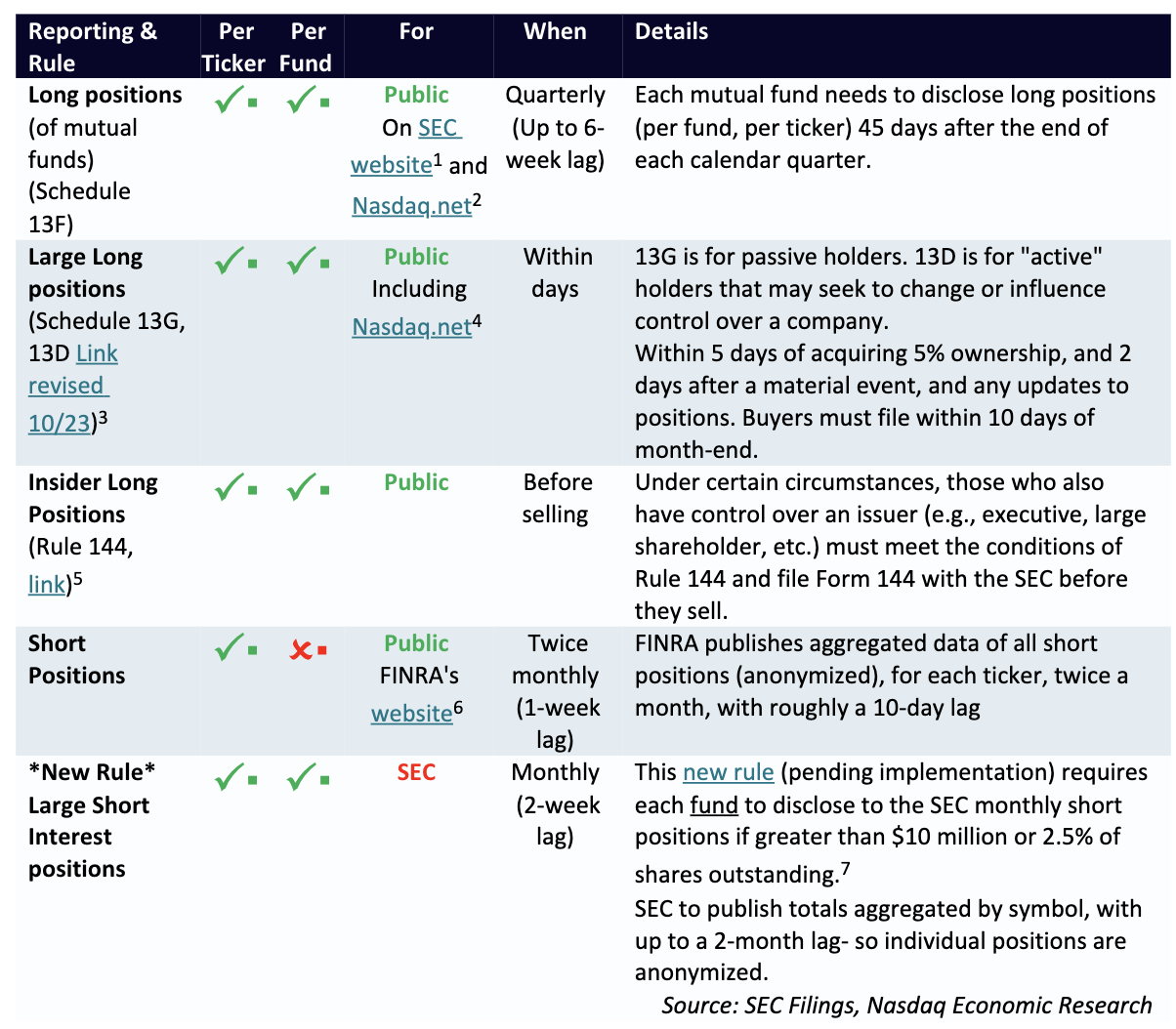

What data is there on short positions?

The data available to companies and traders on short positions differs from the data on long positions.

In general,

- Long position reporting is more granular but less frequent.

- In contrast, short positions are reported more frequently but usually aggregated across the whole industry.

That means companies can tell who owns their stock but not who is short their stock.

Table 1: There are a number of different position reporting rules

What does short position data show?

We have seen before that short positions across the whole market remain remarkably stable over time. The data doesn’t even seem to indicate that shorts increase much during a market selloff. That study also showed that short interest is higher in small- and mid-cap stocks than large- or micro-cap stocks.

We can also look at short positions by stock (below). This shows that:

- The median short position is around 5% or less of shares outstanding for all sectors.

- There are currently larger shortages in the consumer and healthcare sectors than in other sectors.

Chart 3: Short positions as a percent of market cap (by sector)

The data above also shows that a handful of stocks have short interest above 25% of their shares outstanding. We’ve talked about how this can happen before. It’s because borrowed stock can be used to settle new “long” buys. However, that also means each of those stocks has long positions of more than 125% of their market cap.

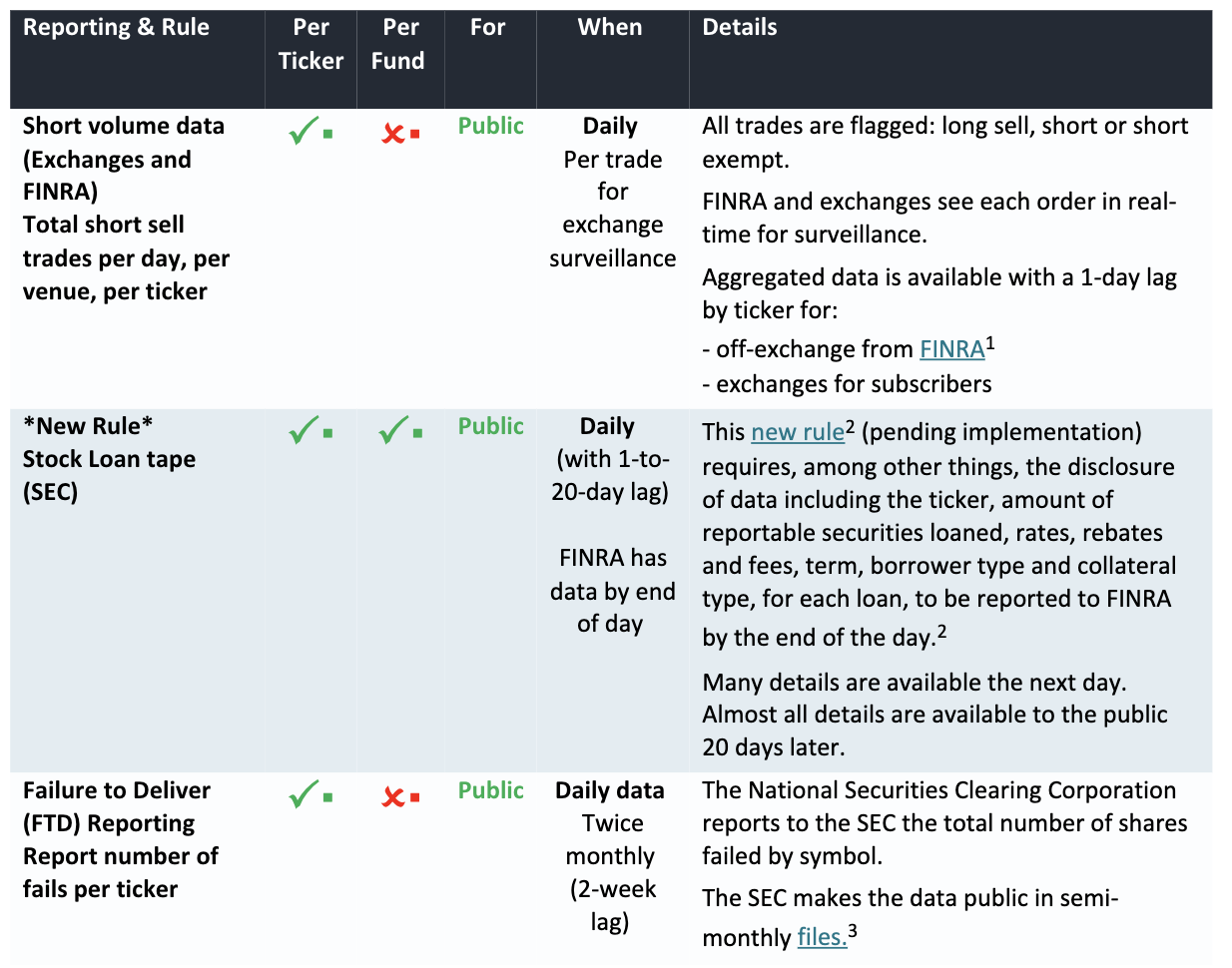

What data is there on short trades?

Regulations also require the disclosure of specific short-trading data. This includes information on short sells as they happen, new rules to highlight stock loan activity, and reports showing the amount of failing trades – which are all part of how shorts operationally work.

Table 2: There are some rules reporting short trading activity as it happens

How do short trading rules work?

There are also rules that direct how short selling works. They limit short selling in a selloff and ban naked shorting. They are mostly in a rule called “Reg SHO,” which is an SEC rule governed by the Exchange Act of 1934, which we include in the table below. There are also rules restricting short selling in the 1933 Securities Act.

Table 3: There are a number of different rules that impact short trading

How do short trading rules work?

Under SEC Rule 200(g), there are three ways to mark sell orders: long, short exempt or short. The basic difference between these three categories are:

- Long sell: The seller owns the security and sells it.

- Short sell exempt: The seller expects to own the stock by settlement date, for example, from delivery from an options trade. Effectively, these are treated as long sales.

- Short sell: The seller does not own the security (or won’t own it by the time of settlement). In order to settle the trade, the seller needs to instead borrow it from a long owner willing to lend their stock (for a fee), and when short sell circuit breakers are on, the up-bid rule applies to these orders.

What does short trading data show?

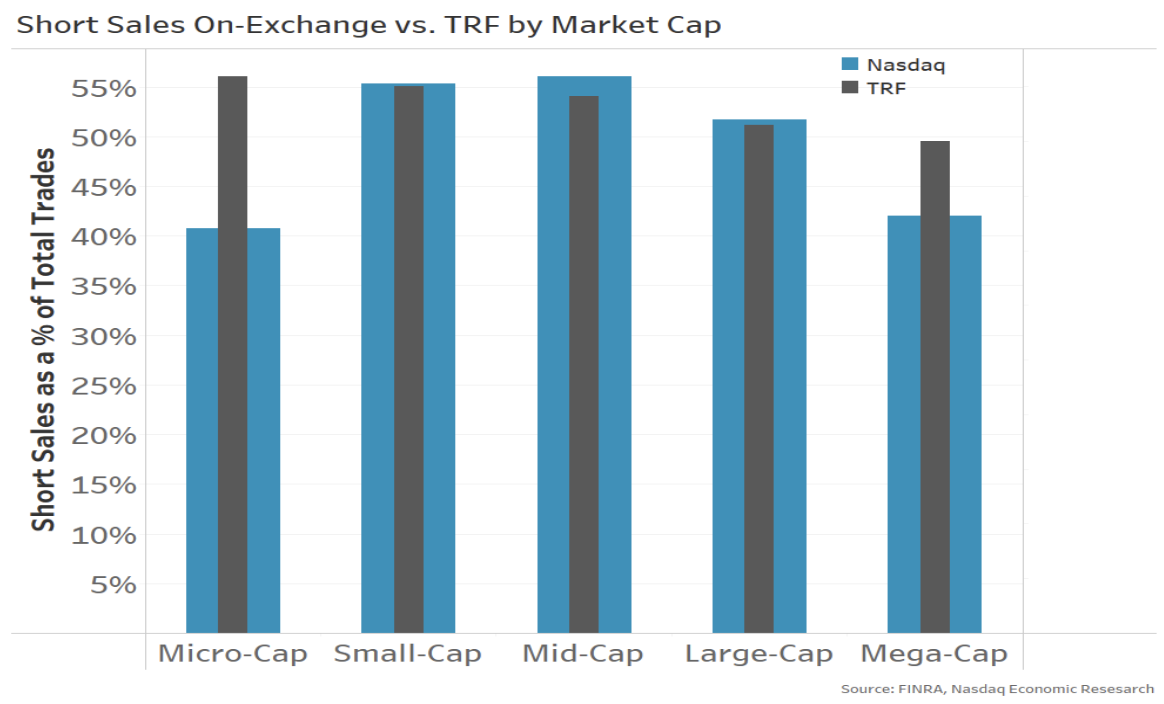

Short sale trading data shows that the typical stock has around 40%-50% of its daily trading volume short sold. That seems a lot, but it’s consistent with the proportion of trades done by intermediaries in Chart 1 above.

Interestingly, we also see that percentage is pretty consistent regardless of the stock’s:

- Market cap or size

- Traded on an exchange or off-exchange. (Although microcap stocks seem a little different, where less short selling happens on exchanges. However, that is consistent with how and what stocks retail trade – implying this is mostly retail market makers facilitating retail orders).

Chart 4: Short trades as a percent of all trades supports our prior research that there is a lot of arbitrage trading in the market

It’s also important to note that this percentage only shows the sell side of all the trades. We know there are also a lot of buy-to-cover trades, as position data show short positions rarely change and are much smaller than the trading data above suggests. Rather than building larger shorts, most intermediaries close out positions within minutes, hours, or maybe days.

Why is a stock loan important to short selling?

In a few spots already, we’ve highlighted stock loan reporting, tapes and borrow requirements.

The reason a stock loan is important is that a security is required to settle each transaction. Currently, two days after the trade date, but soon, just one day later. It’s known as “delivery-versus-payment” or DVP.

Chart 5a: A long sale requires the transfer of the stock at the same time as cash

A new buyer will demand stock before they hand over cash – even if they bought from a short seller.

Given that a short seller doesn’t already own the stock, they need to borrow it from a long holder before the settlement date.

Borrowing stock costs money – both financing collateral to secure the loan and a fee for the lender. So, what normally happens is the seller “locates” a borrower on the trade date. Then, they borrow stock on the settlement date and use it to settle the short trade.

Chart 5b: A long sale requires the transfer of the stock at the same time as cash

There is one exemption on pre-locate of stock, and that’s for a bona-fide market maker. However, market makers still need to deliver stock to settle open short positions, so they do need to incur the cost of borrowing stock before settlement.

Fails are small

If a short seller fails to borrow the stock before the settlement date, the trade will “fail.”

Importantly, failed trades data shows that fails are relatively rare.

In fact, on any day, around three-quarters of all stocks have NO shares failing. And almost 96% of companies have fails for less than 10,000 shares.

Chart 6: Typical count of companies with fails, by size of failing orders

Another way to look at this is to compare the value of failing trades to total market capitalization. This shows that all fails combined are consistently below 0.01% of all market capitalization, adding to between $2 billion and $5 billion of trades.

To put that in perspective and remembering that buys can fail too (if the stock is not allocated from the right account for settlement), U.S. company stocks have buying and selling that adds to closer to $700 billion every day.

Chart 7: Total failing shares consistently add to less than 0.01% of all market cap

In addition to reporting shorts to the market, naked shorting is banned, and RegSHO stops shorts from setting new low prices when a stock has already fallen 10%.

Buy-in rules trigger after one day

The new buy-in rules introduced after the credit crisis require a broker to buy stock to cover a failing position of any customer.

If that isn’t done within one day (two days for a market maker), that broker will be in the Reg SHO “penalty box.” That means they will be required to pay to pre-borrow (not just locate) stock before any shorts in that security are executed across all of their customers.

Threshold list stocks also require pre-borrow

In addition, exchanges publish a “threshold list,” which includes stocks that have had significant fails for more than five days in a row. That doesn’t mean it is the same counterparty failing – just that all fails are not resolved before more occur. Brokers are also required to pre-borrow (not just locate) those stocks before new shorts are executed for all of their customers.

Academic research says short selling makes markets better

Academic research overwhelmingly shows that short selling, on balance, is good.

Most research finds that it tightens spreads, increases liquidity, and improves the accuracy of valuations, especially after news. Overall, that makes markets more efficient at allocating capital, reduces the costs of capital for companies and reduces trading costs for investors.

Other research has shown that short-term bans on short selling do the opposite – reducing liquidity and widening spreads. Interestingly, studies also find no evidence that bans stop stock prices from falling.

Importantly, one study found that during large price reversals, short selling is notably smaller than long selling. As a result, long selling was shown to affect stock prices more than short selling.

There are rules to slow short sellers in a correction

Despite academic research finding short selling is good and that it doesn’t tend to force stocks lower, U.S. rules include a “circuit breaker” to slow short sellers during a dramatic price drop.

If a stock falls 10% during the day, the “modified uptick rule” is put in place. When that occurs, for the rest of that day and the next day, all short-sell trades cannot hit the bid when they sell. That stops them from setting new low bid prices and means they need to wait for a buyer to pay to cross the spread to trade with them.

The data seems to bust most short-selling myths

A lot of people think short sellers harm the market. But the data really doesn’t support them.

Short positions show that for most stocks, shorts are small and consistent across time. That, combined with a lack of persistent fails at scale, indicates that most short selling is closed out the same day as the short.

Perhaps most important of all, when a long investor sells a highly shorted stock, they are more likely to recall loans on their shares, which may cause the shorts to cover, adding buying pressure to the market.

In short, short data indicates that overall, shorts do more good than harm – and there are rules to curb short trading. Short selling helps investors buy their stock for lower costs and higher returns.

Latest articles

This data feed is not available at this time.

Data is currently not available