Growth, expansion, day-to-day working capital, investments in equipment or technology, these are all ingredients for a thriving business. And, the recipe calls for funding. So, what keeps businesses from the cash influx they need, and what is the answer?

We asked business owners how they felt about five main barriers to getting a business loan, and many respondents checked multiple boxes. While the number of small business owners who responded to Finder’s Consumer Confidence Index was small, their responses still have merit. I’ll break down each issue business owners face and a possible solution to consider.

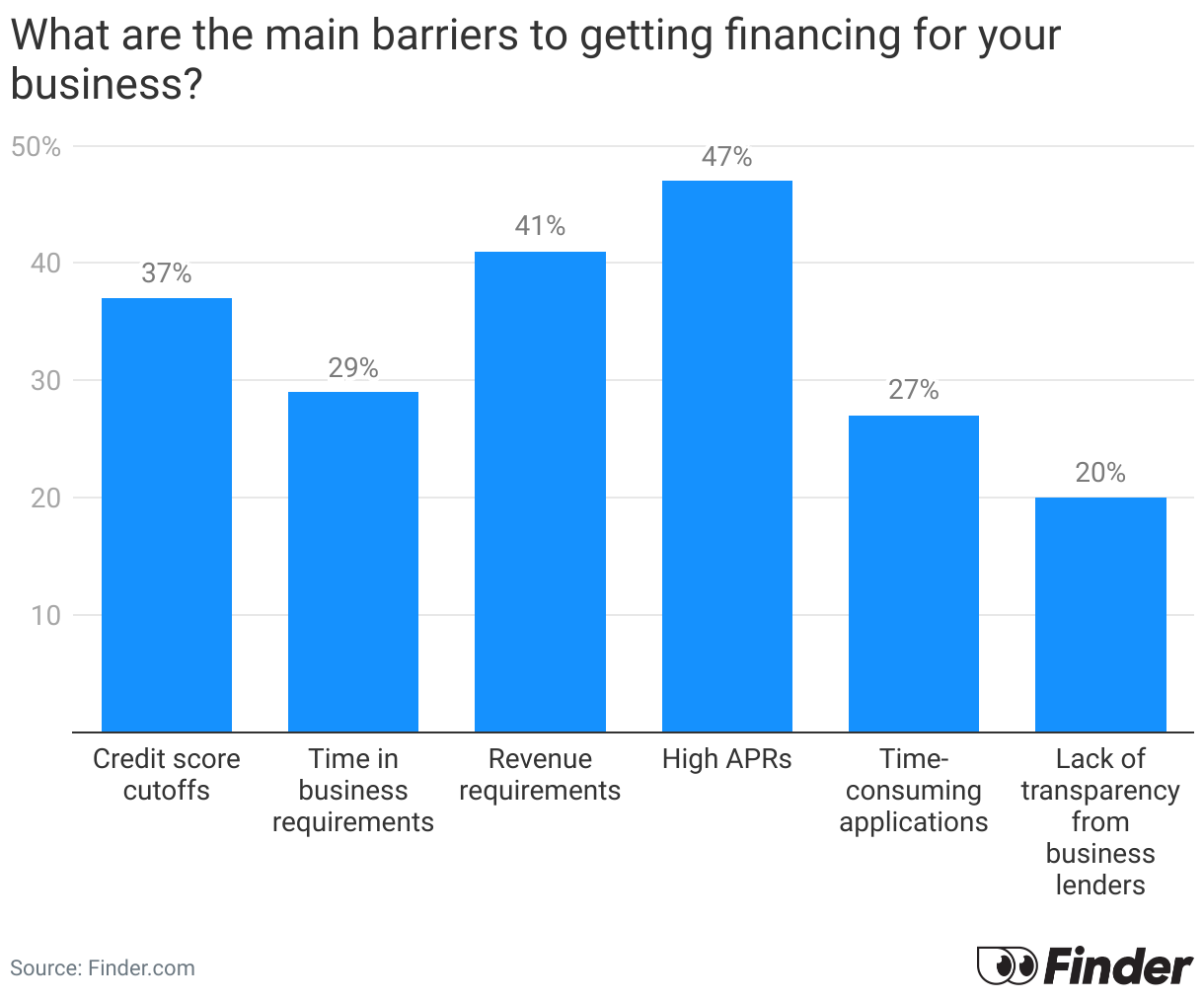

Top 5 barriers to financing

The survey showed that nearly half of American entrepreneurs agree that high APRs are the main reason they can’t get funding. That’s no surprise in the current market. However, the next three reasons are all requirements related: They don’t meet either revenue, credit score or time-in-business requirements. And, more than a quarter of respondents also checked the box for time-consuming applications.

The (possible) solution: No-doc business loans

Now, I won’t claim I have the answer to all business owners' financing hurdles, but a no-doc business loan is one option that may provide relief for business owners facing similar issues when trying to get a business loan.

What is a no-doc business loan, and how does it work?

A no-doc business loan is a type of loan that requires much less paperwork to apply for than a traditional business loan from a bank. These “low-doc” loans come in the form of short-term loans, invoice financing or factoring, merchant cash advances and lines of credit. Lenders offering low-doc business loans mainly operate online and can typically connect to your financial accounts, which means you may not have to provide much more than possible bank statements and signed contracts.

What’s more, lenders requiring less documentation typically base their lending decisions on additional factors that traditional lenders may not take into account. For example, incoming invoices, customer credit histories and more. And, in my research, many of these no-doc business loans come with lower thresholds than typical eligibility requirements.

How can a no-doc loan help?

A no-doc loan offers a better shot for business owners who don’t meet traditional loan revenue requirements, credit score cut-offs and time-in-business requirements to find a lender willing to work with them. From borrowers with bad credit to startups, searching for no-doc loans may be your best chance at getting funding.

Flexible eligibility requirements

No-doc loans typically have more lenient eligibility requirements. While annual revenue requirements for no-doc loans aren’t all below $100,000, you have a better chance of finding a lower revenue requirement threshold compared to banks.

And, like many online lenders, you may find more options willing to work with low or fair credit borrowers. This is especially true with business loan marketplaces and loans like merchant cash advances or other working capital loans.

Fast application and funding

No-doc loans offer some of the fastest funding on the market. And it makes sense, right? Less paperwork and simplified applications can cut your time to funding by more than half. Where a traditional business loan can take weeks or more to get through the qualification process and funding, a no-doc loan can be funded in a few business days or less. And, application decisions can take mere minutes in some cases.

What to watch out for?

You may have noticed I didn’t answer to the high APR barrier to financing. And, the truth is, the tradeoff for more relaxed eligibility, ease of application and speed of funding is higher interest rates. Because a lender presumably takes on more risk by “not knowing” every detail of your financial history, as they would with a traditional loan, more risk is involved. To lessen that risk, borrowers can expect to pay points above the interest they’d pay with a traditional business lender.

Wrap Up

If you’re a thriving business but can’t qualify for traditional financing or need money fast to act on a business opportunity, a no-doc business loan may offer the final ingredient you need. While costs run higher, the relaxed eligibility and fast funding can mean the difference between securing the money your business needs to succeed or passing up opportunities that can keep your business running in the right direction.

Megan B. Shepherd is a personal finance editor at Finder committed to helping Americans navigate the financial world of loans and insurance. Megan’s expertise has graced the pages of Forbes, Fox, Time, Reviews.com, and carinsurance.com, adding invaluable information related to loans and insurance. Megan’s adept knowledge of financial topics has also led to contributions to reputable publications like Nasdaq and MediaFeed, where she intricately dissects and explains personal loans, financial strategies and smart borrowing tactics.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Finder

Finder is a global financial technology platform which allows members to save, invest and spend via the Finder mobile app and website. Finder’s mission is to help people make better financial decisions and work with partners to connect via API into the Finder platform to offer saving and investment services and products. Finder was founded in Australia in 2006 and now operates in 50+ countries with 2,600+ product partners and 10+ million visits every month, serviced by 500+ crew passionate about helping our members achieve their full financial potential.

Read Finder's Bio