However, since this is a capital-intensive industry with high fixed cost of operation and the fairly constant need to expand capacity, it takes longer to recover from any drop in demand.

Because of the increased digitization and greater reliance on digital services over the past few months, a number of players have been able to recoup their losses to stage strong comebacks. Valuation hasn’t kept up in all cases.

Our picks are JOYY Inc., trivago N.V. and Uber, Inc.

About the Industry

Internet - Services companies are primarily those that rely on huge software and hardware infrastructure, referred to as their properties, to deliver various services to consumers. And consumers can avail the services by accessing these properties with their personal connected devices from almost anywhere in the world.

Companies in the sector generally operate two models: an ad-based model where the service is offered free and an ad free model where they charge for the service. Alphabet (GOOGL), Facebook (FB), Baidu (BIDU) and Akamai (AKAM) are some of the larger players in the space while Dropbox (DBX), Etsy (ETSY), Shopify (SHOP), ANGI Homeservices (ANGI), Uber (UBER), Lyft (LYFT) and Trivago (TRVG) are some of the emerging players.

COVID has brought mixed fortune for the industry because the wide range of services provided by this group has m

Factors Shaping the Industry

- Traffic acquisition is one of the most important drivers of revenue, so companies invest in advertising or building communities that can draw more users to their online properties and get them to spend more time there, much like a store owner would try to keep a prospective buyer within the store. Some large players, including those providing infrastructure services, grow by tying up with other such large players for access to their customers. Since the personal touch is absent in an online store, many rely on cookies and other technologies to track users, collect data on them and profile them in order to better understand their needs. App-based service providers like Uber retain customers with competitive pricing and loyalty programs.

- ·As these companies have grown over time, some of them have collected such a wealth of information on their users that the data itself is now helping them build artificial intelligence (AI) to lower cost and generate new technologies and services. As a result, ad-based services are no longer considered free in some parts of the world and the EU in particular has framed a complex law in GDPR that requires service providers to acquire explicit permission from users before collecting their data. More recently, the U.S. has also expressed concern over the lack of competition in the space as big players with a lot of data virtually dominate their markets.

- The installed base of connected devices continues to grow beyond PCs and smartphones to IoT, automotive and more, creating additional opportunities for targeting. The ownership of multiple devices automatically drives people to use these services more as they increasingly automate routine chores.

- While not all businesses are built on the same scale or have the same customer reach, the scope for growth is huge. For companies that are already pursuing research in AI, the prospects are even brighter.

Zacks Industry Rank Indicates Improving Prospects

The Zacks Internet - Services industry is housed within the broader Zacks Computer and Technology sector. It carries a Zacks Industry Rank #102, which places it among the top 40% of more than 250 Zacks-classified industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates that the industry is climbing rapidly out of the pandemic-induced downturn.Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1. So overall, prospects for this industry have notably improved over the past six months.

The industry’s positioning in the top 50% of Zacks-ranked industries is because of its gradual recovery from the pandemic. So its aggregate earnings estimate revisions for 2022 are encouraging, have been incrementally positive over the past year and especially since July 2021. The 2023 estimates are however moving in the opposite direction, which seems to indicate that the current strength includes some pent-up demand and relatively easy comps, which will undergo a correction next year. The aggregate estimate for 2022 is up 11.10% while the average for 2023 is down 11.10% from last year.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

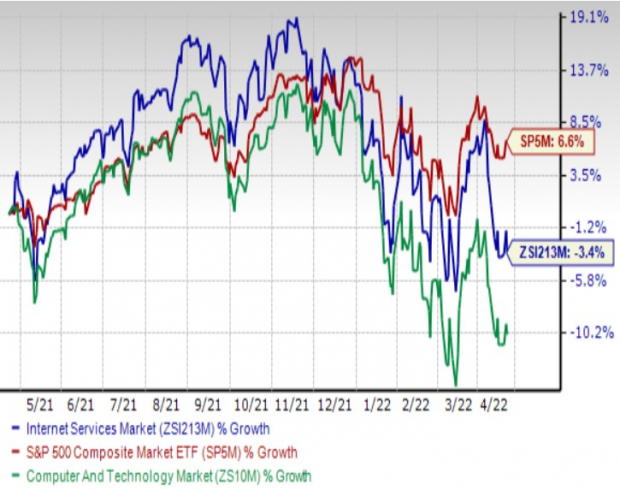

Industry's Stock Market Performance Has Weakened

The industry kept ahead of both the broader sector and the S&P 500 index through most of the past year, but the uncertainties that racked the market since January took a greater toll on it than the S&P 500.

As a result, it is down a net 3.4%% over the past year compared to the broader sector’s 10.3% decline and the S&P 500’s 6.6% gain.

One-Year Price Performance

Image Source: Zacks Investment Research

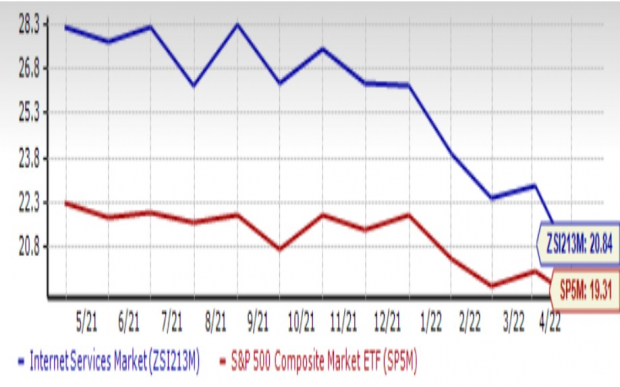

Industry's Current Valuation

On the basis of forward 12-month price-to-earnings (P/E) ratio, which is a commonly used multiple for valuing technology companies, we see that the industry is currently trading at a 20.8X multiple, which is below its median value of 26.3X over the past year, a function of the recent uptick in earnings estimates. The multiple is above the S&P 500’s 19.3X although below the sector’s 22.6X. It is not unusual for the tech sector to trade at a higher multiple than the S&P 500 because of its higher growth profile.

Forward 12 Month Price-to-Earnings (P/E) Ratio

Image Source: Zacks Investment Research

3 Stocks Worth Buying

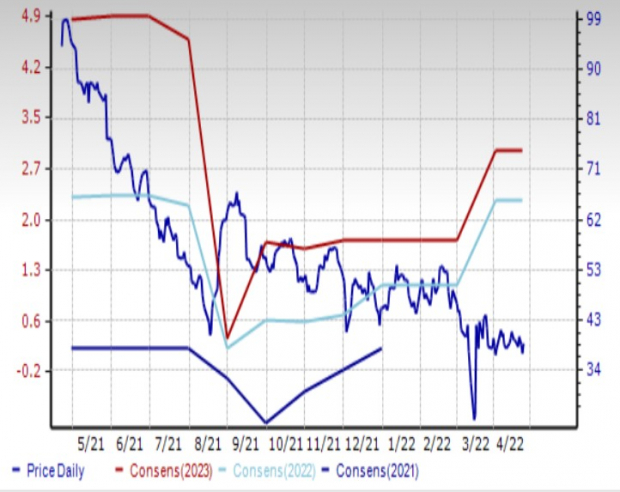

JOYY YY Inc.: Singapore-based Chinese company JOYY, through its subsidiaries, operates several audio and video social media platforms in the U.S., UK, China, Japan, South Korea, Australia and other places. Its popular platforms are Bigo Live, facilitating live streams of specific moments, video calls and trend videos; Likee, a short-form video-based social platform; Hago, a casual game-oriented social platform; and imo, a chat and instant messaging application with video calling, text messaging, and photo and video sharing. Revenues come from in-app virtual items, subscription fees, online education and advertising.

JOYY follows a global-local strategy for growth in its business. The global aspect involves geographical expansion while the local aspect involved the attraction and development of local content. This strategy, along with increased popularity of its short-video and live streaming platforms, and increased monetization of its various platforms is generating strong top line growth for the company while enhanced operating efficiency is boosting its profitability. JOYY also returns cash to shareholders in the form of share repurchases and dividends. The sale of a portion of Huya and YY Live to Baidu will also bring in several billion dollars.

There is only one analyst providing estimates on this stock. And after the quadruple-digit and triple-digit earnings surprises in the last two quarters, this analyst has significant raised estimates for the current year. So now we see that the 2022 estimate is up $1.20 (112.1%) in the last 60 days, while the 2023 estimate is up $1.27 (74.3%).

The shares of this #1 (Strong Buy)-ranked company are down 58.9% over the past year.

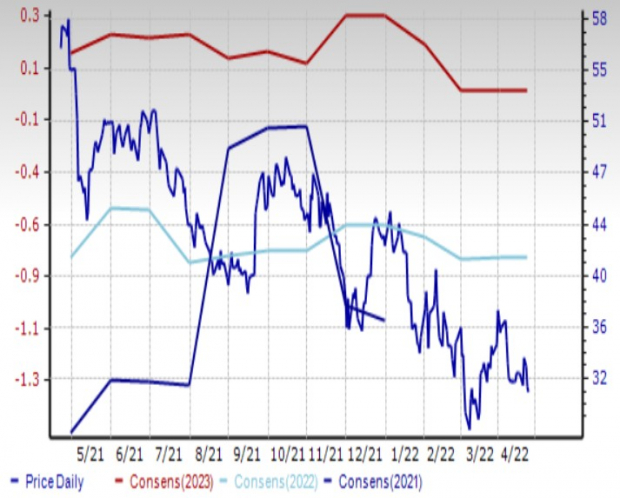

Price and Consensus: YY

Image Source: Zacks Investment Research

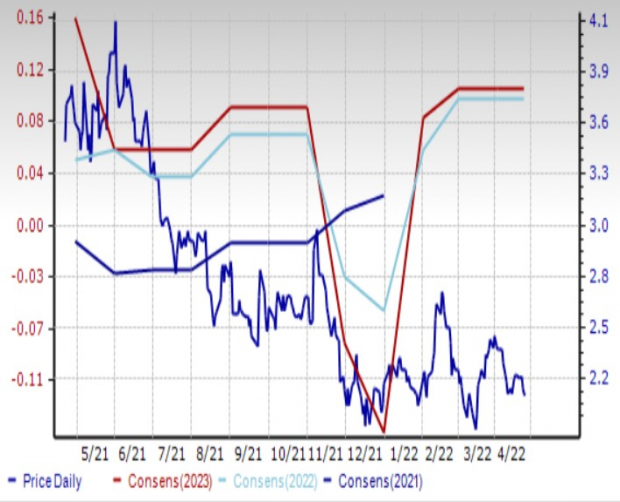

trivago N.V. TRVG: Düsseldorf, Germany-based trivago N.V., together with its subsidiaries, operates a hotel and accommodation search platform in the US, UK, Germany, and elsewhere. It offers an online meta-search service for hotels and accommodation through online travel agencies, hotel chains and independent hotels. Customers access to its platform through 53 localized websites and apps in 31 languages. As of December 31, 2021, its hotel search platform included access to 5 million hotels and other types of accommodation worldwide.

With pandemic concerns alleviating to an extent, governments across the world are opening up more to tourism, which is potentially positive for a company like trivago. However, travel is still likely to be closer to home this year and providers could be labor constrained this summer. This basically points to continued rise in prices across the board, which is not negative for the company. Because it has reduced the cost base over the past couple of years, it will be easier for the company to stay profitable.

This year is expected to be particularly strong for trivago as it grows from a small base. So the 2022 estimate has gone from 5 cents to 10 cents in the last 60 days, an increase of 50%. The 2023 estimate remains steady however. Overall revenue and earnings are expected to be up a respective 58.4% and 233.3% this year and 24.7% and 6.7% in the next.

The shares of this #1-ranked company are down 39.3% over the past year.

Price and Consensus: TRVG

Image Source: Zacks Investment Research

Uber Technologies, Inc. UBER: Uber develops and operates proprietary technology applications/platforms connecting the providers and users of services in the United States, Canada, Latin America, Europe, the Middle East, Africa, and the Asia Pacific. Its primary business is in ride sharing, and this has been diversified into food delivery and freight.

Uber is another stock set to benefit from the pandemic moving to the endemic and the return to normalcy of day-to-day life. So as more people travel to work and other places, ride hailing services are bound to see greater demand. This will end the drought in customer traffic. The trend is already evident from 2021 results, wherein the company posted solid surprises in each of the four quarters, averaging 126.4%.

Despite this strong showing, analysts remain cautious, raising their 2022 and 2023 estimates by a penny each in the last 60 days.

The shares of this Zacks Rank #1 stock are down 44.4% over the past year.

Price and Consensus: UBER

Image Source: Zacks Investment Research

Zacks Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.