Investors continue to seek ways to profit from the launch of fifth-generation (5G) networking services. But when it comes to benefiting from this upgrade, they might want to establish a strong connection with Qualcomm (NASDAQ: QCOM).

The semiconductor company's essential role in the 5G market should take Qualcomm stock dramatically higher in the coming years. Here are three reasons why.

1. The demand for 5G smartphone chipsets

AT&T, Verizon, and T-Mobile have spent the last few years and tens of billions of dollars developing a nationwide 5G network.

Image source: Getty Images.

With 5G's faster speeds and lower latency, engineers expect it could easily be 10 or more times faster than the previous 4G technology.

Samsung began selling 5G phones last year. However, coming off the recent release of the Apple iPhone 12, the 5G upgrade cycle has reached a new plateau.

Hence, almost every smartphone user will probably want to upgrade to this technology at some point. Grand View Research predicts the market for smartphone chipsets will grow at a compound annual growth rate of 63%. Consequently, some expect 2021 will become a defining year for the company.

2. Qualcomm's position in the smartphone chipset market

For now, smartphone manufacturers have only one company they can choose to obtain a needed 5G chipset -- Qualcomm.

Despite this situation, both the government and Qualcomm's competitors have failed to label Qualcomm a monopolist in a legal sense.

In the end, Apple's settled its lawsuits, and Qualcomm persuaded the courts to overturn a previous monopoly decision. This is because customers and even regulators want 5G chips more strongly than they wish to curtail Qualcomm's market power.

Still, although Apple settled in court, it also bought Intel's smartphone chipset business. This could someday give Qualcomm a competitor. However, unless and until that day comes, all of the benefits of 5G chipset growth will accrue to Qualcomm.

3. The valuation does not reflect the opportunity

Qualcomm's latest quarterly non-GAAP revenue rose by 35% from year-ago levels. Diluted earnings per share increased by 86% over the same period.

This is probably not a one-time number. Qualcomm also issued guidance for the first quarter of 2021. During this period, Qualcomm believes diluted EPS will reach $1.95 to $2.15 per share. Considering that Qualcomm earned a diluted EPS of $0.99 in first-quarter 2020, this would result in an approximate doubling of earnings.

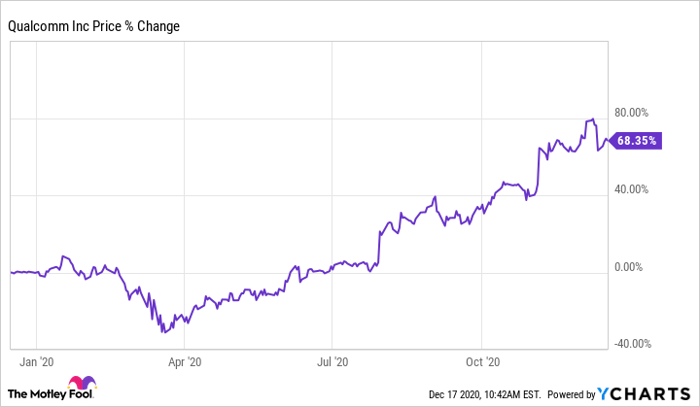

This level of growth is not reflected in Qualcomm's current stock price. Despite stock price growth of almost 70% in the last 12 months, Qualcomm stock trades at a forward price-to-earnings (P/E) ratio of about 21.

Such a multiple usually reflects lower levels of profit growth than investors have experienced recently with Qualcomm. Hence, the relatively low valuation looks like a huge opportunity for investors.

Qualcomm is a buy

Not only is Qualcomm a buy, but it is also hard to imagine a better position for prospective buyers. Regardless of what happens with the overall economy, the world will almost certainly embrace the faster speeds of 5G.

Since only Qualcomm makes a critical 5G chipset, all of the benefits of the forecasted 63% CAGR will probably go to this chip stock. The massive earnings growth of Qualcomm reflects this.

What does not reflect the opportunity is the forward P/E ratio, which now stands barely above 20. Given the market conditions and the financials, tech stock investors should connect with this opportunity before the valuation and the Qualcomm stock price move much higher.

10 stocks we like better than Qualcomm

When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the ten best stocks for investors to buy right now... and Qualcomm wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of November 20, 2020

Will Healy has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Apple and Qualcomm. The Motley Fool recommends Intel, T-Mobile US, and Verizon Communications. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.