Nvidia (NASDAQ: NVDA) is all set to release its fiscal 2025 second-quarter results (for the three months ended July 28) on Aug. 28, and analysts expect another quarter of outstanding growth from the company.

More specifically, LSEG Data & Analytics is forecasting Nvidia's revenue to increase by 112% on a year-over-year basis to $28.6 billion. That's slightly higher than the midpoint of Nvidia's revenue guidance range of $28 billion for Q2. However, LSEG data indicates that Nvidia's adjusted gross margin may have dropped from fiscal Q1 due to the company's investments in ramping up production capacity.

If that's accurate, Nvidia's gross margin would fall below its guidance of 75.5% for fiscal Q2. Now, a slip by Nvidia in its quarterly performance or the accompanying guidance could send its shares tumbling. If that's indeed the case, it may be a good idea for savvy investors to buy this semiconductor bellwether.

However, the possibility of Nvidia's results and guidance exceeding expectations cannot be ruled out. In this article, we will examine three reasons why investors should consider buying Nvidia stock before its upcoming results.

1. An attractive valuation makes the stock worth buying right now

Nvidia's expensive valuation has been a cause for concern in recent months, which is not surprising considering the stunning surge the stock has enjoyed since the end of 2022. However, a closer look at the stock's multiples will make it clear that investors are getting a good deal on this high-flying chipmaker right before its earnings report.

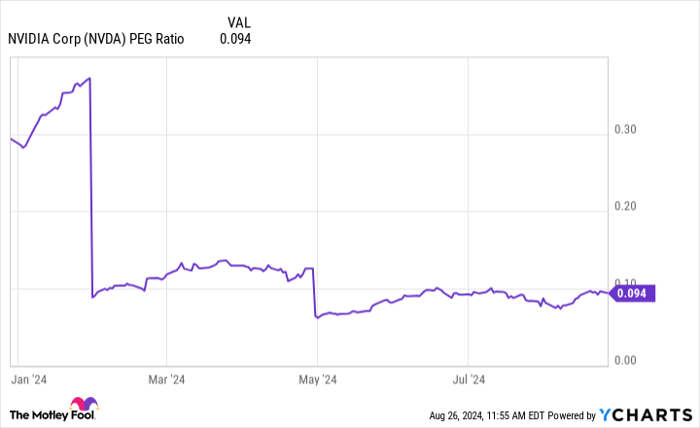

Nvidia currently trades at 48 times forward earnings. For comparison, the U.S. technology sector currently has an average earnings multiple of 46. Meanwhile, the stock's price/earnings-to-growth ratio (PEG ratio) provides an even better gauge of how attractively valued Nvidia is right now. That's because the PEG ratio is a forward-looking valuation metric calculated by dividing a stock's trailing P/E ratio by the estimated earnings growth that it could deliver.

A PEG ratio of less than 1 indicates that a stock is undervalued. By that measure, Nvidia stock seems extremely undervalued with respect to the earnings growth that it is likely to deliver.

NVDA PEG Ratio data by YCharts

As such, Nvidia is still a solid bet for investors looking to add a growth stock to their portfolios right now, especially considering that there are indications that it could deliver better-than-expected results.

2. These AI hardware companies indicate that Nvidia is poised to deliver solid results

The earnings season is about to end, which means that we can get a fair idea about the health of the AI hardware market based on results from other companies in this ecosystem.

For instance, Nvidia's foundry partner Taiwan Semiconductor Manufacturing (NYSE: TSM), popularly known as TSMC, saw its top line jump 33% year over year in the second quarter of 2024 (which coincided with two months of Nvidia's fiscal Q2). That was a significant jump from the 13% year-over-year jump in revenue that TSMC delivered in the first quarter of the year. It is also worth noting that TSMC's July revenue increased 45% year over year, outpacing the growth it has witnessed in the first two quarters of the year.

TSMC has been working hard in recent months to increase its packaging capacity of advanced chips that are used to manufacture AI chips for Nvidia. So, the surge in TSMC's quarterly revenue growth provides strong evidence of robust growth in Nvidia's revenue and earnings, especially because Nvidia is TSMC's second-largest customer.

However, TSMC isn't the only AI hardware player that has seen a significant surge in revenue recently. Super Micro Computer (NASDAQ: SMCI), which manufactures AI server solutions used for mounting chips from chipmakers such as Nvidia, reported 143% year-over-year revenue growth in the fourth quarter of fiscal 2024 (which ended on June 30).

Supermicro attributed its phenomenal growth to the "strong demand for next generation air-cooled and direct liquid-cooled (DLC) rack-scale AI GPU platforms." What's more, the midpoint of Supermicro's revenue guidance for the current quarter stands at $6.5 billion, which would be a 216% increase from the same quarter last year.

Again, this is an indication that Nvidia could be ramping up the production of its next-generation Blackwell chips, which the company had promised would arrive later in 2024. Nvidia, therefore, could not only deliver results that may outpace Wall Street's expectations, but its guidance could also turn out to be solid and help the stock sustain its stunning rally.

3. Big tech's capex surge is good news for Nvidia investors

Technology titans such as Microsoft, Meta Platforms, Alphabet, and Amazon have been ramping up their capital expenditures (capex) to bolster their AI infrastructure. For instance, Microsoft's fiscal 2024 capital spending rose 75% from the previous year to almost $56 billion. The company expects to raise its capex once again in the current fiscal year to spend money on building more AI services so that it can position itself for long-term growth.

Alphabet, on the other hand, could end the year with capex of around $50 billion as it intends to keep pouring money into servers and data centers. That would be a major increase over last year's capex of $32 billion. Even Meta raised its 2024 capital expenditure guidance to a range of $37 billion to $40 billion, up from the prior range of $35 billion to $40 billion. The social media giant's 2023 capex stood at $28 billion, and it expects its capital spending to continue rising into 2025.

Investors should note that all of these companies have been Nvidia's customers, purchasing the company's chips to train and deploy AI models. Even better, they are set to adopt the chipmaker's next-generation Blackwell processors as well, and Nvidia expects that the demand for these new chips will outpace supply well into 2025. This potential spending could carry the company for quarters and even years to come.

In all, there is enough evidence that the demand for Nvidia's AI chips continues to remain healthy, allowing it to deliver results that could exceed consensus estimates and guide above expectations. If that happens, shares of Nvidia could get another shot in the arm, which is why it may be a good idea for long-term-minded investors to buy this AI stock before it potentially soars further after Aug. 28.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 26, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.