Given all the unknowns when planning for retirement, it's crucial to think carefully and make thoughtful decisions about saving and investing because some common mistakes can significantly impact your financial future.

Here are three costly retirement mistakes you can’t afford to make and insights on how to avoid them.

1. Not contributing enough in your 401(k) to earn the full company match

One of the most advantageous benefits provided by many employers is the 401(k) match. This benefit is essentially free money offered by your company to boost your retirement savings. According to a 2023 Vanguard research report, 85% of 401(k) plans in 2021 offered an employer matching contribution, with an average employer match of 4.4%.

Surprisingly, many employees fail to take full advantage of this opportunity by not contributing enough to earn the full company match. While more than two-thirds (66%) of private industry workers had access to a defined contribution plan like a 401(k) in 2022, only 48% of those eligible employees participated, according to the Bureau of Labor Statistics.

The mistake

Some individuals contribute to their 401(k) but stop short of maximizing their employer match. For example, if your employer matches contributions up to 4% of your salary, failing to contribute at least that amount means you’re leaving free money on the table.

The cost

By not maximizing the company match, you’re missing out on a significant boost to your retirement savings. Over the long term, this can result in a substantial reduction in the potential size of your retirement nest egg.

For example, let’s assume your annual salary is $50,000, and your employer matches 100% of your contributions up to 4% of your salary. If you have no starting 401(k) balance and contribute 4%, or $2,000, each year, your employer will also contribute $2,000. If you start saving at age 25 and until age 65 and earn a 7% annual rate of return, this could translate to a potential 401(k) balance of $828,522.06. Dropping your contribution rate by even 1% could reduce your retirement savings by $207,142.94.

How to avoid it

Review your employer’s 401(k) matching policy and strive to contribute at least enough to earn the full match. Consider gradually increasing your contributions to ensure consistency and take advantage of any raises or bonuses to boost your retirement savings.

2. Funding your IRA but not investing your money

Individual retirement accounts (IRAs) offer a valuable avenue for retirement savers with potential tax advantages. The best IRAs also offer tools and resources to help you maximize your investments.

However, merely funding your IRA is not enough — you must also invest those funds. Otherwise, your money will sit stagnant in your IRA without growth.

The mistake

Some individuals diligently contribute to their IRA each year but leave the money sitting in cash or low-yield investments. This cautious or uninformed approach might seem safe, but it exposes your savings to the eroding effects of inflation over time.

The cost

Failure to invest your IRA funds means missing out on the opportunity for compound growth. Over the years, inflation can erode the purchasing power of your money, and your retirement savings may not keep pace with the rising cost of living.

Moreover, uninvested cash has no chance to benefit when markets rally, and being out of the market can significantly impact your portfolio’s potential performance. A $10,000 investment in the S&P 500 between January 1, 2003, and December 30, 2022, where you missed 10 of the market’s best days, would result in $35,136 less than if you were fully invested during that period, according to JP Morgan.

How to avoid it

Develop a well-thought-out investment strategy for your IRA based on your risk tolerance, time horizon and financial goals. Consider a diversified portfolio of traditional assets like stocks, bonds, ETFs (exchange-traded funds) and alternative assets like real estate and commodities to optimize your potential returns while managing risk. Or avoid stock picking altogether and invest in an S&P 500 index fund for instant diversification and to perform at least as well as the market.

3. Don’t devote too much of your portfolio to individual stocks

For individual investors — and even professionals — stock picking is a fool’s errand. Research shows that individuals almost always underperform the market.

While the allure of picking individual stocks can be tempting, it’s often a risky and costly approach to retirement investing.

The mistake

Some investors believe they can outperform the market by cherry-picking individual stocks. However, this approach requires extensive research, time and expertise. And even then, you’re likely to underperform the market. Even seasoned professionals struggle to beat the market consistently.

Relatively few active managers can outperform passive managers over any given period, either short-term or long-term, according to S&P Global’s S&P Indices versus Active (SPIVA) Scorecard. For instance, 60.90% of actively managed funds underperformed the S&P 500 over one year, as of June 30, 2023. Over 15 years, as much as 92.19% of active funds underperformed the S&P 500.

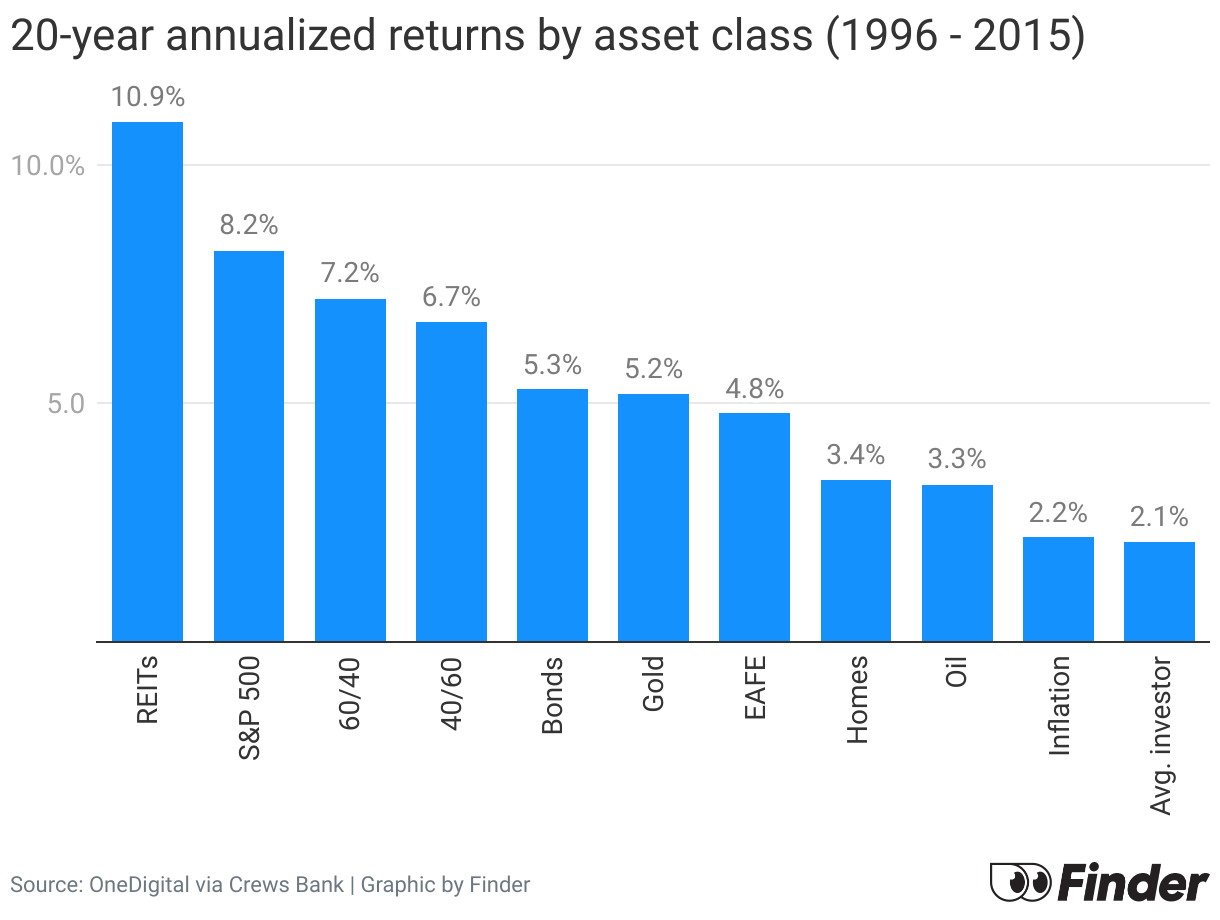

Individual investors perform even worse. While the S&P 500 saw annualized returns of 8.2% between 1996 and 2015, the average retail investor saw just 2.1%.

The cost

Picking individual stocks can lead to underperformance, excessive trading fees and increased risk. If your stock selections don’t outpace the broader market, you may miss out on the steady and reliable returns offered by the overall market.

How to avoid it

Consider investing in low-cost index funds that track broad market indices. This approach provides instant diversification across a wide range of stocks, reducing the risk associated with individual company performance. Index funds are known for their cost efficiency and historically competitive returns. If you have a strong conviction about individual stocks, allocate only a small portion of your portfolio to such investments to manage risk.

Bottom line

As you plan for retirement, avoiding these three costly mistakes can make a significant difference in the success of your financial future. Take advantage of employer matches, ensure your retirement funds are actively invested and consider the benefits of diversified index fund investments.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Smart Investing Retirement

Finder

Finder is a global financial technology platform which allows members to save, invest and spend via the Finder mobile app and website. Finder’s mission is to help people make better financial decisions and work with partners to connect via API into the Finder platform to offer saving and investment services and products. Finder was founded in Australia in 2006 and now operates in 50+ countries with 2,600+ product partners and 10+ million visits every month, serviced by 500+ crew passionate about helping our members achieve their full financial potential.

Read Finder's Bio