The cannabis market enters 2020 with plenty of catalysts for higher sales and profits. A lot of companies have made changes in executive leadership to handle the next phase of growth as legalization in cannabis markets slowly progresses and public market veterans are more apt to join the sector.

Due to a wide-open market opportunity and readily available capital, most industry participants have gone guns blazing into nearly every segment of the cannabis market. The global cannabis market is expected to be worth $200 billion, but industry participants must deal with the current environment in order to survive and thrive.

The executive leadership team best equipped to focus on particular market strengths will reward shareholders. The company able to streamline operations while maintaining growth should see the biggest stock rebounds as capital requirements disappear in a tough funding environment. Not to mention the stronger companies can utilize available capital, whether equity or cash, to snap up beaten-down players, helping consolidate the industry and eliminate competition.

While Canopy Growth (CGC) made headlines after replacing its CEO with a Constellation Brands (STZ) executive, we wanted to look into three other Canadian companies that could see their big corporate pivots reward shareholders:

Tilray (TLRY)

On January 15, Tilray, which has seen dramatic highs and lows, announced a new COO and CFO. Current CFO Mark Castaneda will transition to Strategic Business Development after leading Tilray on the wild IPO ride to $300 back in 2018. Ever since, the company has failed to impress the market due to substantial operating losses.

The two new executives come with impressive backgrounds. New CFO Michael Kruteck was the CFO of Pharmaca Integrative Pharmacy, with prior senior financial roles at beverage giant Molson Coors (TAP).

COO Jon Levin came from Revlon (REV), where he was responsible for consumer products sold through major retailers in the U.S. Both executives have the crucial experience in the beverages and CPG segments, areas Tilray wants to expand in 2020 and beyond.

As with most of the other cannabis stocks, the founding CEO remains in the leadership role. The big question is whether anything changes at Tilray with the moves at the top.

When Tilray reports Q4 results, the market will eagerly pay attention to whether the company undergoes any type of restructuring. For Q3, the company reported revenues of $51.0 million, but the net loss was $49.1 million, and the EBITDA loss was a rather large $23.5 million.

The market cap is down to below $2.0 billion, so the new executives will need to work wonders to justify the market value on only $310 million in 2020 revenues.

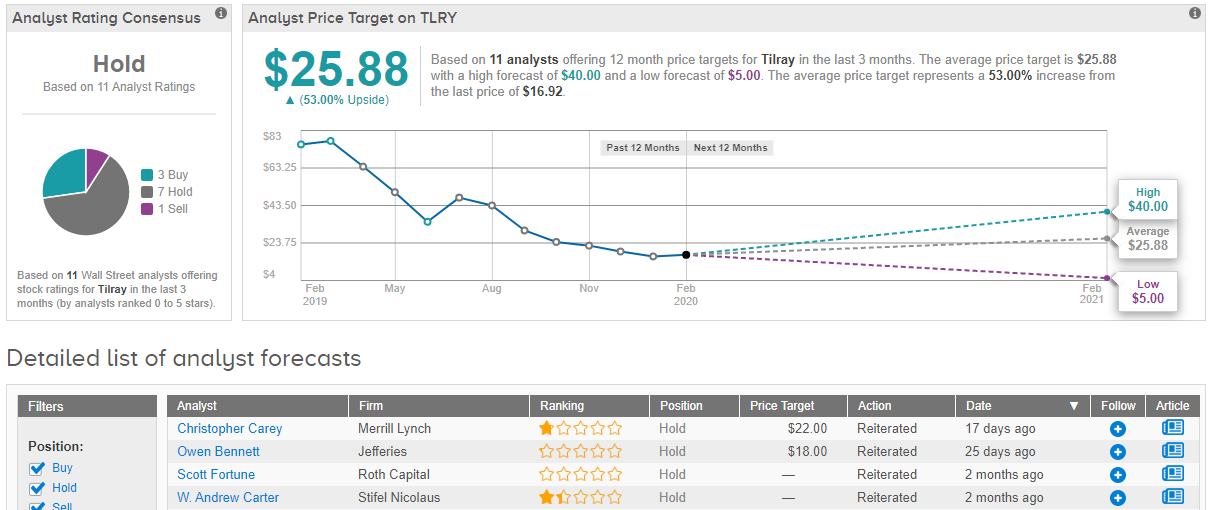

When it comes to Wall Street, analysts are taking a cautious approach. In the last three months, the stock has received 3 Buy ratings, 7 Holds and 1 Sell, making the Street consensus a Hold. However, the $25.88 average price target implies that shares could climb 53% higher in the next twelve months. (See Tilray price targets and analyst ratings on TipRanks)

Sundial (SNDL)

Sundial hasn’t gotten a lot of media attention after going public back in August when the cannabis industry was already struggling. On January 30, the CEO and COO both left the company. Very few companies see several top executives exit within six months of the IPO.

Along with the executive departures, Sundial will implement a cost-cutting initiative to generate C$10-$15 million in savings for 2020. Back in November, the company reported that in Q3, revenues hit C$33 million and it boosted production nearly 10-fold within two quarters to 11,700 kg of premium cannabis.

For the quarter, adjusted EBITDA loss was C$7.9 million as the company scaled production and expanded into Europe with the purchase of agricultural indoor producer Bridge Farm. The market most likely isn’t fond of Sundial boosting EBITDA losses and building out operations in the UK.

Additionally, the stock took a big hit at the end of the week due to the executive shuffle. However, the interim CEO’s cost-cutting initiative is a positive first step for a company whose $140 million in cash on the balance sheet from the IPO makes a turnaround a very real possibility.

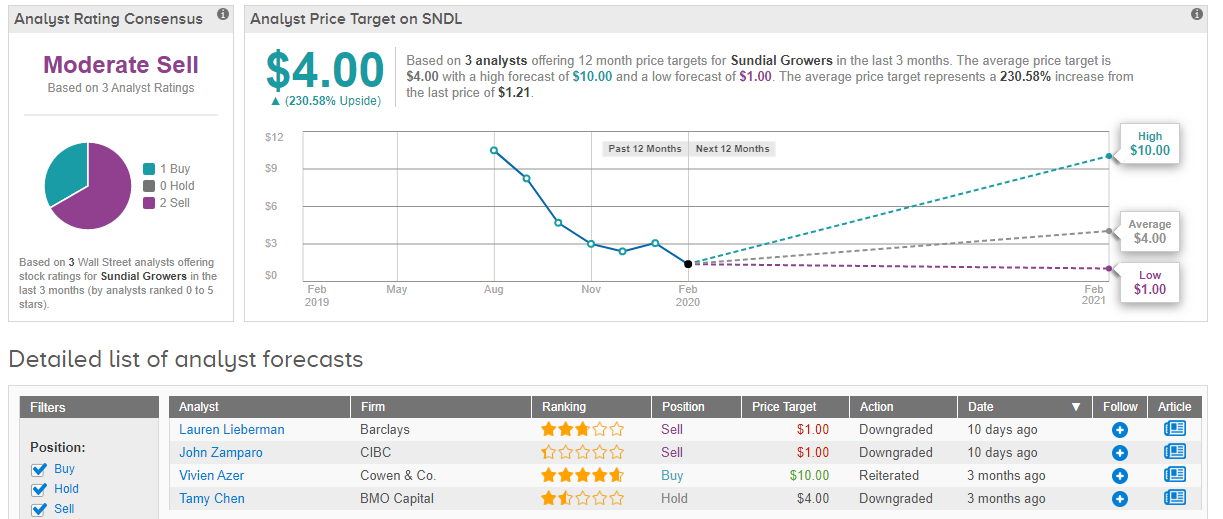

The rest of the Street is bearish on SNDL, with 1 Buy call and 2 Sells adding up to a Moderate Sell consensus rating. It should be noted, though, that the $4 average price target puts the upside potential at 231%. (See Sundial stock analysis on TipRanks)

HEXO (HEXO)

HEXO replaced the CFO just prior to announcing a massive cut to FY20 guidance. The company had the least impressive executive shuffle, promoting the VP of Strategic Finance to the new role and keeping the founding CEO at the helm of the company.

Since the CFO’s replacement, HEXO has launched the Original Stash cannabis value brand and raised over $100 million in cash to fund operations. The biggest issue remains the reorganization to cut costs, with the prior CFO’s efforts not anywhere near enough for the company to reach positive EBITDA in the near term.

In its most recent quarter, HEXO gross margins were only 31% and the company had several impairment charges. Prior CFO Michael Monahan, who previously worked at Nutrisystem, was highly regarded, but the issues were blamed on him not working at the Canadian facilities during this ramp up period.

Under the new CFO, HEXO will have to show that more dedicated leadership will lead to better product development and cost containment to match a more realistic market opportunity as 2020 progresses.

The Canadian cannabis company can’t maintain C$33 million quarterly losses when revenues are only C$14.5 million and not forecasted to top C$26 million well into 2020. Even strong 50% gross margins won’t solve their current financial predicament.

As with the above stocks, any sign the new executive is leading the charge to a turnaround could present a unique buying opportunity. Since the company is streamlining the business on top of cutting cultivation capacity, a move to exit certain business lines while doubling down on the promising value brand or cannabis-infused beverages would be bullish indications.

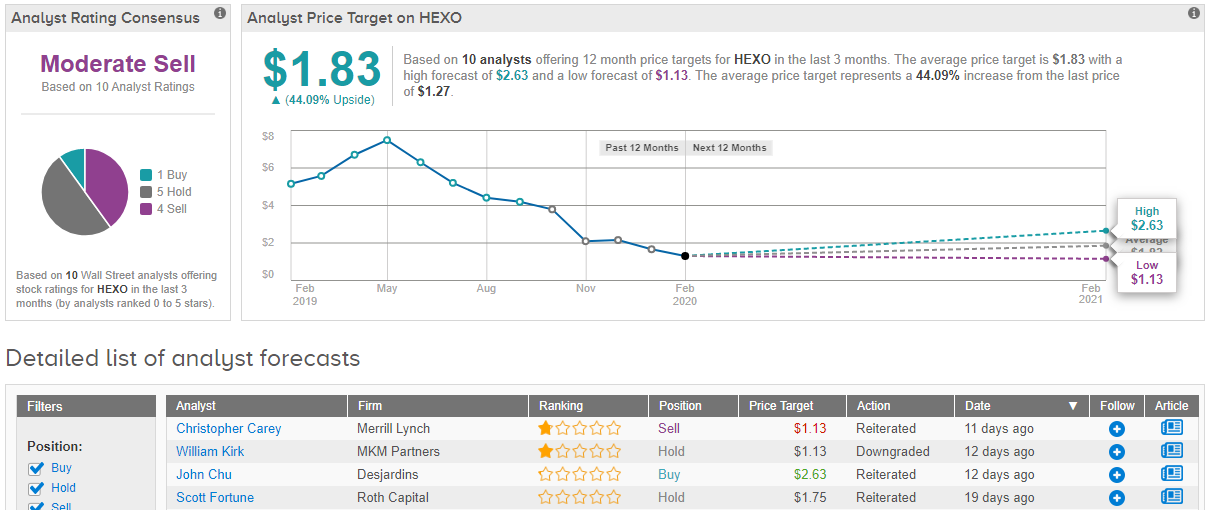

Looking at the consensus breakdown, a single Buy rating, 5 Holds and 4 Sells coalesce into a Moderate Sell. Should the $1.83 average price target be met, a 44% twelve-month gain could be in the cards. (See HEXO price targets and analyst ratings on TipRanks)

Disclosure: No position.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.