Mr. Market, a construct of the famous value investor Benjamin Graham, is a fickle individual. Sometimes he offers up opportunities that look attractively priced, only to change his mind far more quickly than you'd expect, running the price right back up again.

When shopping for potential investments, I occasionally get access to the attractive price, which is what happened with my investment in WEC Energy (NYSE: WEC). But after the subsequent share price rally over just a few months, I decided to sell the utility and use those funds to invest in a higher yield that remains out of favor.

WEC Energy moved too quickly for me

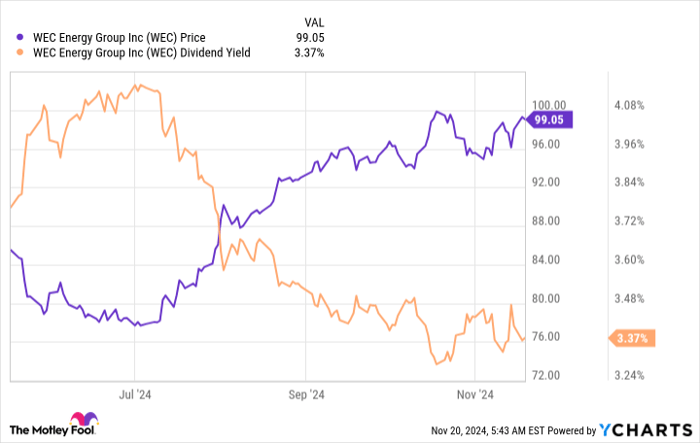

I bought WEC Energy in July 2024, when the dividend yield was north of 4%. The yield, the history of dividend growth, and the opportunity presented by the utility's ongoing shift toward cleaner energy was more than enough to get me in the door.

And then, shortly after I bought WEC Energy, utility stocks rallied. The yield from WEC Energy is now around 3.4%.

That's not high enough for me to add to my position. Add in the roughly 20% stock advance in just a few months, and I'm worried that WEC Energy has gone too far, too fast. At the very least, I see it as fairly valued and no longer cheap. In fact, I was kind of expecting that 20% stock advance would be spread over three years, not four months or so. I decided to lock in the profits and shift into a different utility-related investment.

A yield that's 4.5x the yield on the S&P 500 index

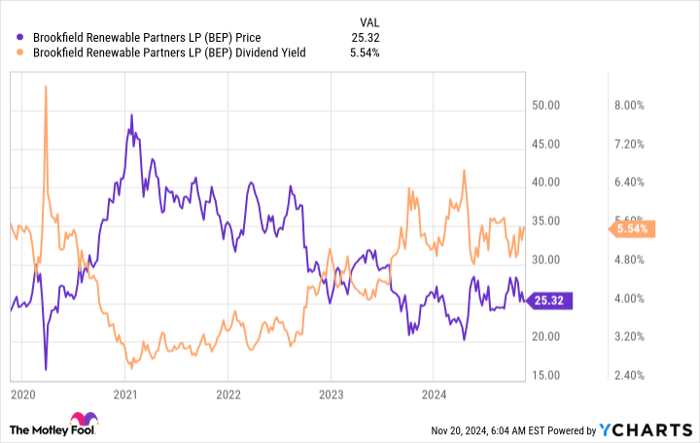

What I bought to replace WEC Energy was a unique clean energy-focused business with a 5.6% yield. That's 4.5 times larger than the yield on the S&P 500. It is twice as high as the average utility, using Utilities Select Sector SPDR ETF (NYSEMKT: XLU) as an industry proxy. And it is 1.6 times that of WEC Energy. That's a worthwhile increase compared to WEC, and definitely attractive relative to the broader utility space and the market.

But the real reason I bought Brookfield Renewable Partners (NYSE: BEP) is the opportunistic nature of its investment approach. To start, I believe there's a long runway for growth ahead as the world continues to shift toward cleaner energy alternatives. Brookfield Renewable has its fingers in just about every pie, with exposure to solar, wind, hydroelectric, storage, and nuclear. And its portfolio is globally diversified, so it can put money to work just about anywhere there's an opportunity.

That sets the stage for the partnership's approach of buying low and selling high, driven by its relationship with Brookfield Asset Management (NYSE: BAM). Essentially, buying Brookfield Renewable is a way for me, a small investor, to partner with the institutional money that Brookfield Asset Management runs.

With a strong financial position (Brookfield Renewable has an investment-grade-rated balance sheet) and its partnership with Brookfield Asset Management, Brookfield Renewable has the ability to step into troubled situations. It then restores the assets it buys to health, both financially and operationally. And if it gets a good deal, it sells the asset and repeats the process with a new investment.

Right now, Brookfield Renewable is able to do both because well-capitalized, high-performing clean energy assets are selling at attractive prices, while financially troubled clean energy assets are trading hands on the cheap. Wall Street, meanwhile, is treating the clean energy sector like every asset is in trouble (leading to what I believe is an attractive price for Brookfield Renewable), which simply isn't true.

And, on top of that, there's a huge runway for growth ahead as the world continues its clean energy shift. Brookfield Renewable, which has regularly increased its distribution, allows me to directly invest in that transition.

Brookfield Renewable is my direct play

I own Enbridge and TotalEnergies because they bridge the gap between fossil fuel-related energy and clean energy. Brookfield Renewable is my first direct play on clean energy, which I'm making after Wall Street's fascination with the sector has waned.

I guess I'm trying to be opportunistic, too. In fact, there's extra pessimism right now because of fears that government subsidies will go away in the United States. On that score, Brookfield Renewable is very clear that subsidies aren't really that important to its future.

I'm in, and I'm planning to hold on for a decade or more. You might want to reconsider this out-of-favor, high-yield, utility-like business, too.

Should you invest $1,000 in Brookfield Renewable Partners right now?

Before you buy stock in Brookfield Renewable Partners, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Brookfield Renewable Partners wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $898,809!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 18, 2024

Reuben Gregg Brewer has positions in Brookfield Renewable Partners, Enbridge, and TotalEnergies. The Motley Fool has positions in and recommends Brookfield Asset Management and Enbridge. The Motley Fool recommends Brookfield Renewable Partners. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.