Buying best-in-class but expensive-looking stocks with premium valuations is one of the hardest things to do when investing.

It's easy to look at a business trading at three times the market's valuation and go "nope," regardless of the company's promising operations. However, I believe that many of these richly valued stocks (not all, though) trade at lofty valuations for a good reason, as they have the potential for multibagger returns over a decades-long time horizon.

One such company is the fast-casual chicken wings chain Wingstop (NASDAQ: WING). Since its initial public offering (IPO) in 2015, Wingstop has become a 14-bagger -- even though investors who purchased the stock at its IPO had to pay 100 times earnings to own shares.

With the company currently down 22% as of Dec. 4 after a recent pullback, here are five reasons why I believe history will repeat for Wingstop as it becomes one of the best compounders on the market.

Five reasons Wingstop is a compelling investment

Wingstop has over 2,200 locations worldwide, a figure that has nearly doubled since 2017. The company generates the vast majority of its orders for carryout or delivery. It offers a simplified menu of wings that come in 11 flavors, as well as fries and chicken sandwiches and tenders.

By focusing on digital orders for carryout and delivery, paired with this straightforward menu, Wingstop's throughput potential only really ends where its customers' appetites do. Factors that make it a compelling investment include:

1. An asset-light franchise model

Wingstop primarily uses a franchise model, with franchisees operating roughly 98% of the company's locations. Currently, it has about 216 separate franchisees that have an average of nine restaurants with a tenure of approximately 14 years.

In exchange for a 6% royalty and a 5% fee for its advertising budget on gross sales, Wingstop provides its branding and business processes to these franchisees across the world. The beauty of this model is that Wingstop offloads most of the capital and operational risk to franchisees, making it a high-margin business capable of growing with fairly minimal capital expenditures.

2. A straightforward growth story

Despite doubling its store count since 2017, Wingstop opened 106 net new locations in its most recent quarter. This increase was good for 17% unit growth compared to the prior-year period, and shows that management still has its foot on the growth engine's accelerator.

While these shorter-term growth results are great to see and monitor, management's stretch goal of more than quadrupling its current store count is what gives the stock multibagger potential. Working hand in hand with its franchisees, the company believes it has a playbook to develop 6,000 stores domestically and 4,000 internationally -- a far cry from today's 2,200 locations.

Though this growth means nothing if the new locations aren't prosperous, I lean toward optimism thanks to the fact that 95% of Wingstop's new openings come from existing franchisees who have already seen success.

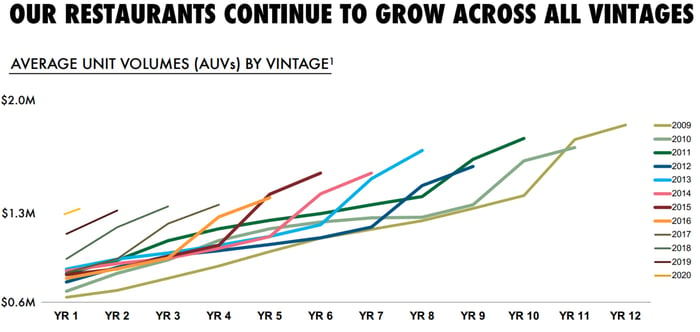

Best yet for investors? Opening new stores isn't the only route to growth for Wingstop. After delivering same-store sales growth for 20 consecutive years, the company has a long history of its locations maturing into highly profitable enterprises, with each new vintage earning more than the last.

Image source: Wingstop 2022 investor presentation.

Between these steadily improving vintages and Wingstop's nonstop store count growth, it shouldn't be surprising to learn that the company grew sales by 23% annually over the last decade, including 39% in the last quarter.

3. A high return on invested capital drives outperformance

Another reason to be optimistic about Wingstop's potential is that its return on invested capital (ROIC) has risen from 8% in 2015 to 38% today. As a measure of the company's profitability compared to its debt and equity, Wingstop's high ROIC shows that management is very adept at growing in a value-generating manner for shareholders.

Stocks with high-and-rising ROICs like Wingstop's have more than doubled the total returns of their lower-ranked peers since 2003, as this article suggests. Despite being fully in growth mode, Wingstop maintains a robust 24% free cash flow (FCF) margin, giving it ample funding to reward shareholders.

4. Steady dividend growth

Wingstop has grown its quarterly dividend from $0.07 to $0.27 since 2017. To put the power of this dividend growth in perspective, consider that if an investor bought and held Wingstop shares since 2017, they would now receive a 3.5% yield compared to their original cost basis.This feat is relatively rare among growth stocks.

Despite the company's stretched valuation, thanks in part to its status as a growth stock, it only uses 20% of its FCF to fund its 0.3% dividend yield, leaving a long growth runway ahead. While this yield seems small now, the company's dividend growth potential could prove to be massive.

5. The stock is not as "expensive" as it looks

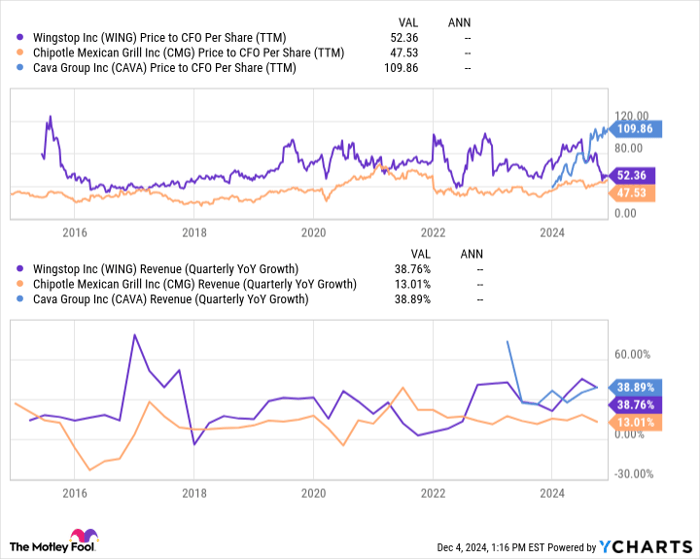

Wingstop currently trades at 98 times earnings. However, I believe a more accurate way to value the company's shares is to use its price-to-cash from operations (P/CFO) ratio of 52.

Cash from operations shows the cash a company generates before it spends anything on capital expenditures, which is new store additions in Wingstop's case. This difference makes it a more effective valuation to use to compare Wingstop to a high-growth peer like Cava Group and a more mature business in Chipotle Mexican Grill.

WING Price to CFO Per Share (TTM) data by YCharts.

I admit that this is not a perfect way to compare these three promising fast-casual stocks. Nonetheless, it highlights that Wingstop's superior growth rates are available for a valuation similar to Chipotle. Meanwhile, Cava -- which is growing at a similar rate to Wingstop -- trades at nearly double the valuation.

Ultimately, Wingstop's combination of high profitability, immense growth potential, and steady dividend growth at a relatively fair price compared to its peers makes it a super growth stock to buy and hold for decades after its recent pullback.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $376,143!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,028!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $494,999!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 2, 2024

Josh Kohn-Lindquist has positions in Chipotle Mexican Grill. The Motley Fool has positions in and recommends Chipotle Mexican Grill. The Motley Fool recommends Cava Group and Wingstop and recommends the following options: short December 2024 $54 puts on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.