The technology sector is having a fantastic year, with the Nasdaq Composite (NASDAQINDEX: ^IXIC) up by 30% so far. Many of the largest stocks in the tech sector are doing even better, like Nvidia, which has soared by 209%.

But not every tech stock is participating in the rally. Workiva (NYSE: WK), for example, offers a unique portfolio of software products to help companies streamline data aggregation and reporting, which are becoming increasingly important business functions. Its stock is down 4% this year, and it's down 42% from its all-time high, which was set during the tech frenzy in 2021.

The underperformance in Workiva stock hasn't deterred Wall Street. The majority of the analysts tracked by The Wall Street Journal have assigned it the highest-possible buy rating, and not a single one recommends selling. Its business is growing nicely, and its stock currently trades at an attractive valuation, so here's why investors might want to follow the analysts' lead.

Image source: Getty Images.

Workiva's software is growing in importance

Technologies like cloud computing are helping businesses of all sizes to run their operations online. That enables them to access a global customer base and to tap into remote workforces, which are big positives. However, it also means businesses need to use dozens or even hundreds of digital applications every day, which leads to fragmented workflows.

That creates a nightmare for managers in terms of monitoring progress, gathering data, and compiling reports. Workiva solves that problem with its cloud-based platform, which plugs into almost every leading productivity and storage application, and aggregates their data onto one dashboard.

That means managers don't have to track data through each individual piece of software -- whether employees are using Alphabet's Google Drive, Microsoft Excel, or Salesforce. It can all be aggregated through Workiva.

From there, it offers hundreds of templates to help managers quickly convert that data into reports for executives, or submit regulatory filings to the Securities and Exchange Commission, which is very useful for publicly traded companies.

The company is now using its expertise to focus on environmental, social, and governance (ESG) reporting, which is a fast-growing global opportunity. Governments all over the world continue to introduce new rules that require organizations to report their impact on the environment and society, and Workiva's ESG tool helps them track carbon emissions, workforce diversity, and similar metrics.

The platform allows businesses to access pre-built ESG frameworks, form strategies, collect data, compile reports, and connect teams so they can collaborate. As mandatory ESG reporting becomes more widespread in the coming years, this product could be a big growth driver for the company.

Revenue growth accelerated in Q3, driven by high-spending customers

Workiva recently reported its financial results for the third quarter of 2024 (ended Sept. 30). It generated a record $186 million in total revenue, which was a 17% increase from a year ago. That was also an acceleration from the 15% growth in the second quarter, and the strong result prompted management to raise its revenue forecast for the 2024 full year by $6 million to a range of $733 million to $735 million.

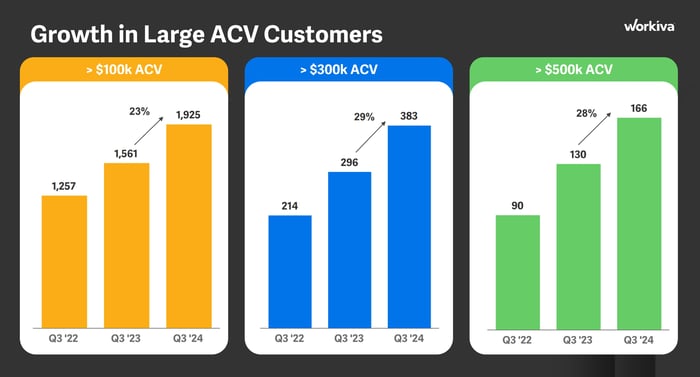

Growth is being driven by its highest-spending customers. At the end of the third quarter, the company was serving 6,237 businesses, which was a 4.9% increase from the same quarter last year. And the increase in customers with annual contract values (ACVs) of at least $100,000, $300,000, and $500,000 outpaced overall customer growth by a wide margin, as the chart below shows.

Image source: Workiva.

That highlights how important Workiva's software is becoming among the largest organizations, which typically have highly complex digital operations. Moreover, the proportion of customers that have adopted at least two of the company's products reached a record high of 68% during the third quarter, which is evidence of a positive reaction to the company's expansion into areas like ESG.

These strong results are even more impressive considering that management is carefully controlling costs to improve its bottom line. Through the first nine months of 2024, operating expenses increased by just 10%, and while the company still lost $46.2 million at the bottom line, that was a vast improvement from the $123.3 million it lost in the year-ago period.

Once Workiva achieves consistent profitability, it will have the flexibility to start investing more aggressively in growth initiatives like marketing and research and development, which could trigger faster revenue increases over the long term.

Wall Street is bullish on Workiva stock

The Wall Street Journal tracks 11 analysts who cover Workiva, Seven of them have assigned it the highest-possible buy rating. Two more are in the overweight (bullish) camp, while the remaining two recommend holding. No analysts recommend selling.

Their average price target for the next 12 months is $104.3, which represents an upside of 14.3% from where the stock trades as of this writing: $91.49. However, the Street-high target is $120, which implies an upside of 31.1%.

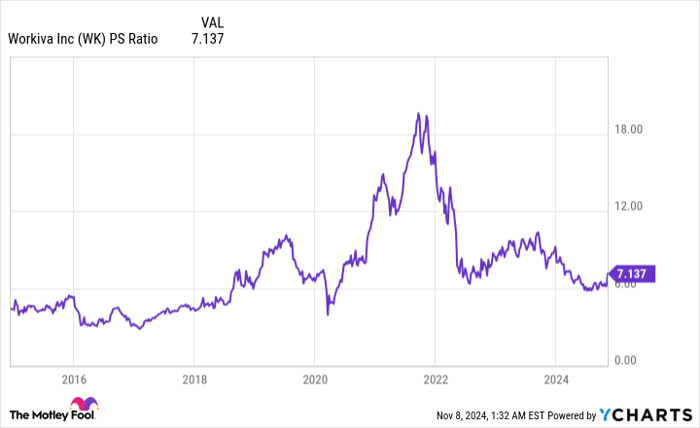

As I mentioned at the top, the stock is down 42% from its record high, which was set in 2021. It was unquestionably overvalued back then, with a price-to-sales ratio (P/S) of around 20. But the decline in its stock combined with the company's consistent revenue growth has shrunk that P/S down to a more reasonable 7.1.

WK PS ratio, data by YCharts.

I think the stock could exceed even the high end of Wall Street's forecasts over the long term because management places the value of its financial opportunity at $35 billion across financial reporting, ESG reporting, compliance reporting, and more. Considering Workiva's market capitalization is just $5.1 billion right now, the company has a long runway for growth.

Should you invest $1,000 in Workiva right now?

Before you buy stock in Workiva, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Workiva wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $904,692!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 4, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Microsoft, Nvidia, Salesforce, and Workiva. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.