Credit: Shutterstock photo

Credit: Shutterstock photoInvestorPlace - Stock Market News, Stock Advice & Trading Tips

Earlier this month, Nomura initiated coverage on Tesla Inc (NASDAQ: TSLA ) with a buy rating and Street-high $500 - yes, $500 - price target. The target implies more than 40% upside. Tesla issues stock in the form of capital raises and employee compensation; however, assuming its share count stays constant and TSLA stock runs to $500, it would imply a market cap of around $80 billion to $85 billion.

This would make Tesla roughly equivalent to Starbucks Corporation (NASDAQ: SBUX ) and PayPal Holdings Inc (NASDAQ: PYPL ) and more valuable than companies like Costco Wholesale Corporation (NASDAQ: COST ), Qualcomm, Inc. (NASDAQ: QCOM ) and Adobe Systems Incorporated (NASDAQ: ADBE ). Is it warranted?

TSLA Stock's Upgrade

TSLA stock is up 1,130% over the last five years and 65% year-to-date. One could make an easy argument that Nomura is late to the party. However, at least TSLA stock was about 10% off its highs when the call was made.

Nomura analyst Romit Shah says Tesla has an " insurmountable lead " in vehicle range per dollar. That's even with companies like General Motors Company (NYSE: GM ) announcing new plans to significantly increase its electric vehicle (EV) game ( at least 20 vehicles by 2023 ). Ford Motor Company (NYSE: F ), BMW , Mercedes and many others are trending in that direction as well. Most are being forced this way, considering many countries have already made the decision to ban internal combustion engines (although several of these bans are a decade or more away).

By the analyst's words though, the competition is "largely inferior." Will it stay that way?

Tesla should experience an "unprecedented" increase in sales, and even though the Model 3 is experiencing some production issues, it should rebound soon enough. By 2020, Shah says Tesla should be operating with gross margins in the mid- to high-20% range.

Notably, the collective analyst community expects TSLA to grow sales 70% this year and another 68% in 2018 to $20 billion. Longer-term estimates call for 37.5% growth in 2019 to $27.5 billion, while 2020 estimates call for 29% growth to $35.5 billion. Since these estimates are so far out, they may prove to be inaccurate.

Breaking Down TSLA Stock

Ford and GM may not be appropriate comparisons. After all, revenue growth is among their largest hurdles, unlike Tesla. Neither automaker has attractive growth rates for this year or the next. But what are margins like?

In 2016, GM had gross margins of 12.8%, and Ford's were 19%. 2015's figures were 12% and 15.4%, respectively. So Shah's call for gross margins in the mid- to high-20% range aren't too crazy. Tesla isn't Ferrari NV (BIT: RACE ), but the latter sports gross margins of 45%, so it is doable.

Cash burn has to be one concern for investors. Admittedly, TSLA's operating cash flow (OCF) temporarily improved in 2016. OCF of negative $124 million was a vast improvement from the $525 million deficit in the prior year. However, through the first six months of 2017, Tesla has OCF of negative $270 million.

On a free cash flow (FCF) basis, it doesn't get much better. In fact, it gets a lot worse. On a trailing 12-month basis, FCF currently sits at negative $3.15 billion. The FCF situation is certainly not ideal. After hovering between negative $300 million and negative $200 million for several years, FCF is plunging, particularly over the last six months. The fact that cash flow from financing continues to jump is also slightly concerning.

Much of this can be attributed to Tesla's Model 3 production push, as well as other ambitions such as the Gigafactory.

The Bottom Line on TSLA Stock

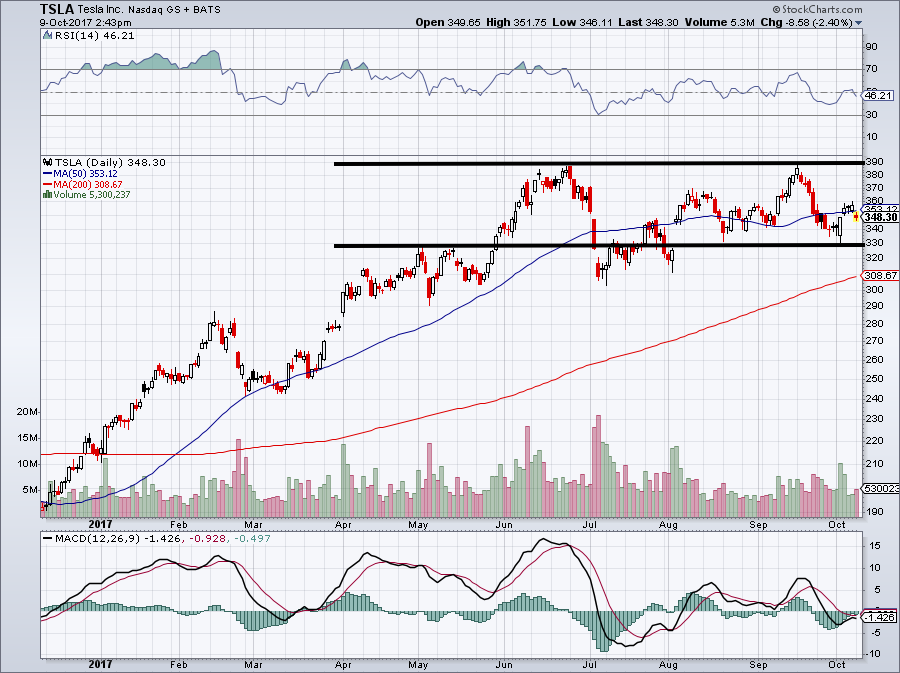

Click to Enlarge

It's really hard to be a long-term buyer of TSLA stock at these levels. I don't doubt Tesla's future by any means, but there are fundamental concerns to be aware of. For me to be a buy-and-hold investor, I need a massive correction. If the TSLA stock price fell 30% to 40%, I would be interested. That kind of decline is not impossible when considering what a broad market correction can do to high-volatility stocks.

- Why Tesla Inc (TSLA) Stock Is STILL Just a Gamble Right Now

That said, I would not short TSLA stock. There are cult-stock buyers and momentum pushers that can drive massive losses for short sellers. YTD gains suggest just that possibility. $330 was previously resistance and now acts as support. Tesla stock price fell below the $350 level, so there's reason to be leery in the short term, but so long as $330 holds, bulls can stay long with $390 still acting as stiff resistance.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell . As of this writing, Bret Kenwell held a long position in SBUX.

More From InvestorPlace

- 3 Gold Stocks Ready to Run

- Tesla (TSLA) Stock Pops Again, But Should Investors Hit the Breaks?

- The 10 Most Expensive Stocks in the S&P 500

The post Will Tesla Inc (TSLA) Stock Really Climb to $500 Per Share? appeared first on InvestorPlace .

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}