Credit: Shutterstock photo

Credit: Shutterstock photoBy Matt Sheldon :

One of the concepts regarding "investing in water" that we struggle to communicate is that it is not a sector bet. That is hard to comprehend since most of the stocks in which we invest are either industrial companies or utilities. But because water courses through the veins of the global economy, a water investing strategy has a multitude of end market drivers, providing a stabilizing and diversifying growth element to a global equity allocation.

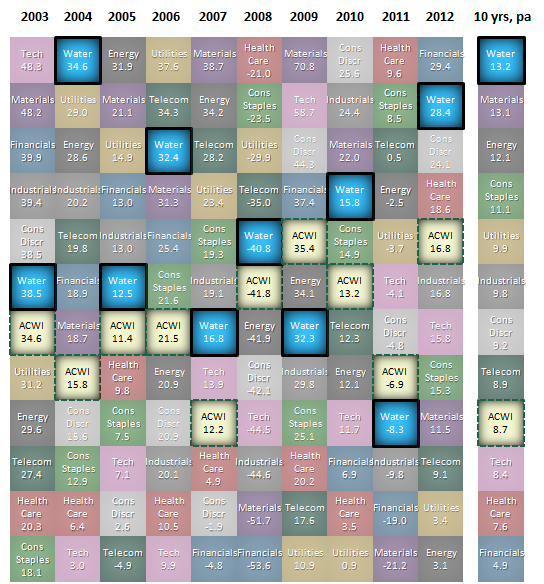

With the recent circulation of aiCIO's periodic table of annual hedge fund strategy returns ( here ), it reminded me that a picture is worth a 1000 words. Using this structure, we have put together a periodic table of MSCI All Country ( ACWI ) sector returns over the last 10 years, inserting the performance of our KBI Water Strategy (gross returns). Unlike the ACWI sectors, which come in and out of favor year by year, Water performs consistently in the upper tiers - and rises to the top in aggregate over the last 10 years.

Source: Kleinwort Benson Investors, Datastream, MSCI, total return, based in USD, gross of fees as at December 31st 2012

Why is this? Because water is such a critical component of life and industry, water businesses are driven by diverse and sometimes geographically specific end market dynamics. Perhaps, the best example for this is Pentair ( PNR ). Nearly 20% of its sales are related to housing - i.e. the consumer discretionary sector. A further quarter of its business is generated from sales to power plants, refineries and gas processors (energy sector) and nearly 10% is sold to food and beverage companies (consumer staples). Another example isKurita Water (KTWIF.PK) in Japan. It sells ultrapure water equipment and services to the semiconductor and flat panel display companies (technology) and steel mills (materials). It also sells water treatment chemicals (materials) to its customers. Companies selling analytical equipment or components to the water industry for quality testing, like Danaher ( DHR ) and Idex ( IEX ), are also selling into biotech and pharma laboratories (healthcare) and electronics manufacturers (technology). In total, almost all the sectors in the global equity market are represented.

The other reason for the consistency in performance is that investing in water provides both risk-on and risk-off investment options. Regulated water utilities can act quite defensively while water infrastructure companies can act very cyclically. Being able to actively manage between these two based on bottom up valuation metrics and top down perspectives has resulted in a beta of the KBI Water Strategy of approximately 1.0 since inception in late 2000.

Why does this distinction matter? Investing in water means different things to different people, so it is important to outline exactly what we mean and take on the myths that create hesitation to the opportunity. Faced with a "sector bet" decision, the question is whether the short- to mid-term timing and conditions are ripe for outperformance. But we would argue that investing in water requires, instead, an understanding of the long-term tailwinds, and appreciating the breadth of those tailwinds across many end markets and companies. From that, we believe, the long-term consistent outperformance is derived.

Disclosure: I am long [[PNR]], [[DHR]], [[IEX]], [[KTWIF.PK]]. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.Please see profile page for full disclosure.

See also Dunkin' Brands Group, Inc. Presents at UBS Global Consumer Conference, Mar-14-2013 10:30 AM on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}