Credit: Shutterstock photo

Credit: Shutterstock photoBy Gene Balas, CFA :

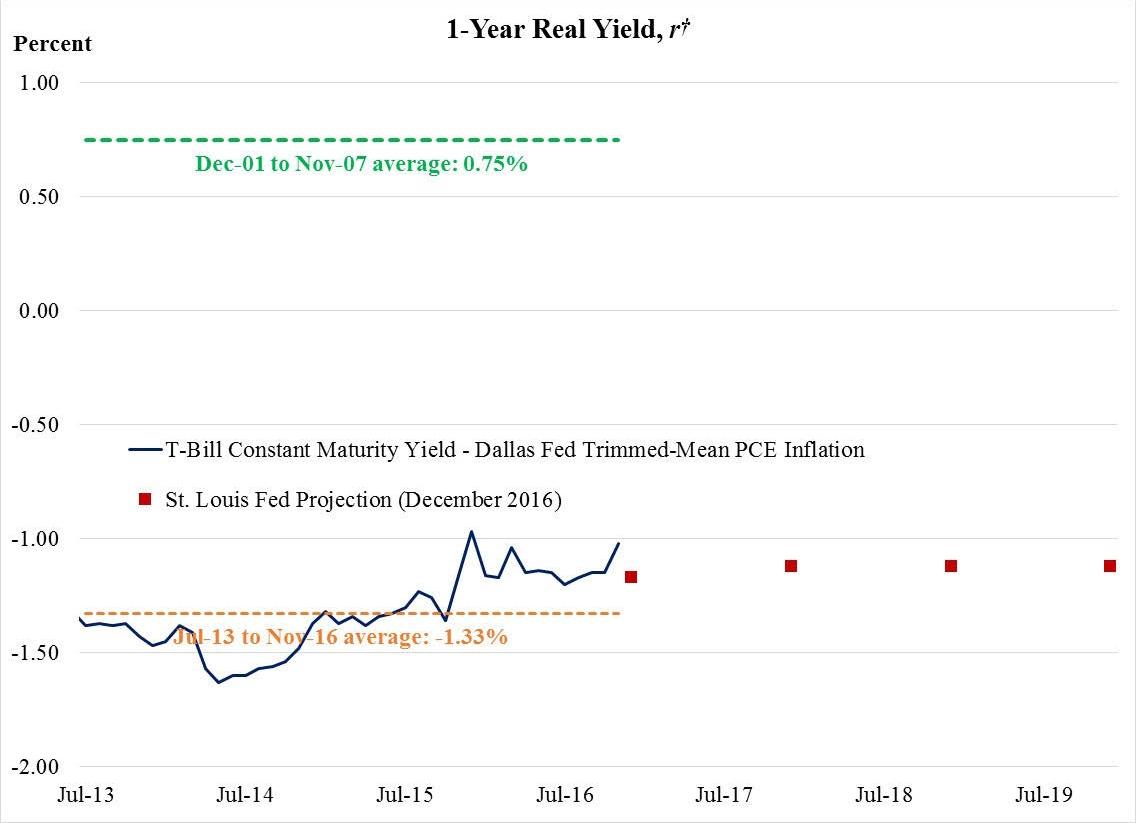

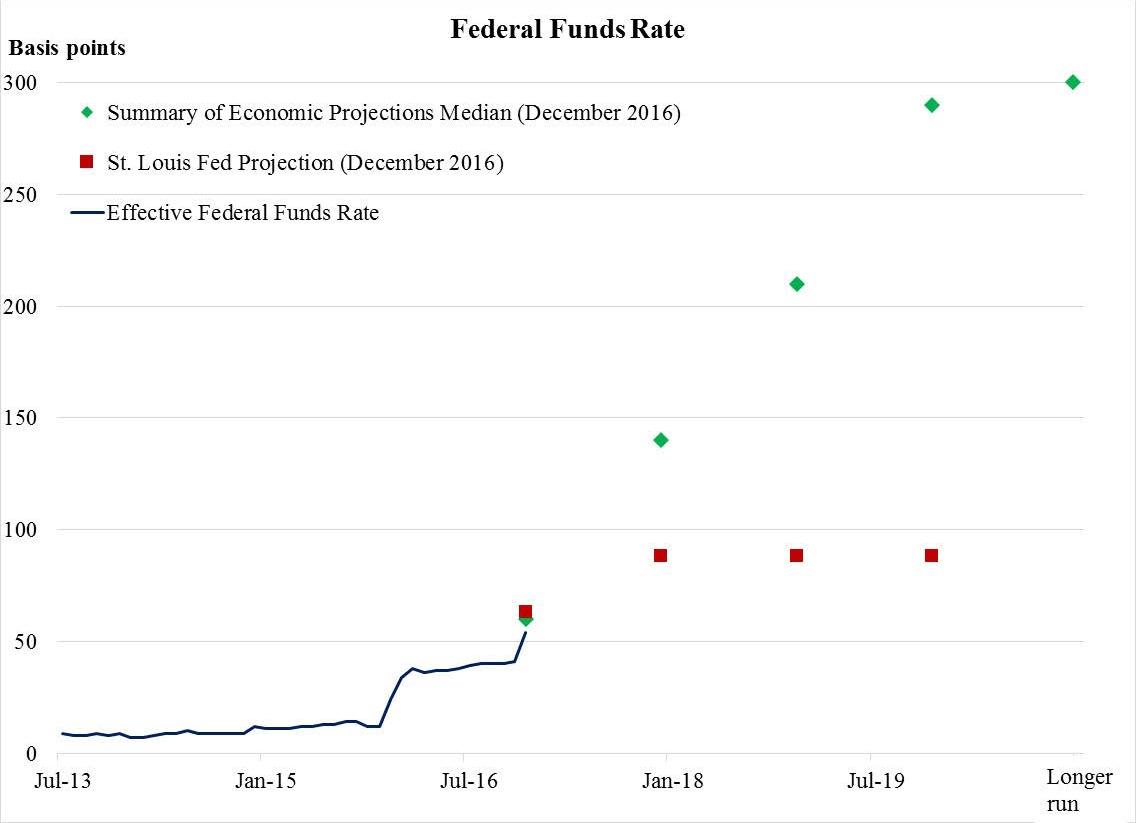

Part of this discussion may sound a bit heretical, but it is actually based on research conducted by the St. Louis Federal Reserve. And its research concludes that the natural real (net of inflation) interest rate policymakers should set should actually be negative over the longer term . According to the St. Louis Fed President James Bullard, one more Fed rate hike would be appropriate between now and the end of 2019. And that's it, which would bring up the Fed funds policy rate up to a bit less than 1%. With an inflation target of 2%, the real natural rate of interest would be roughly negative 1%.

Other Fed members, meanwhile, expect to see the Fed fund rate close to 3% in the longer run. So why does the St. Louis Fed believe rates to be so low? (You may refer to Bullard's presentations here and here .) Well, there are a few reasons. Not least of which are that inflation and employment are stable and more or less close to the Fed's target with rates where they are now. That argues for little need for a change. Another reason is that the economy simply can't grow as fast as it once did, given an aging population and a low growth rate of the labor force, along with middling productivity gains. That keeps demand for credit constrained, needing less restrictive policy rates.

So, how does the St. Louis Fed calculate where rates should be? We know that the Fed controls overnight lending rates, but the market controls everything else further out on the yield curve. True, rates are low abroad, and the stimulus measures of the ECB have flowed into U.S. markets. But even before that, we've observed that real rates on the one year Treasury have consistently fallen to reach the levels at which Bullard believes the natural rate should be. And the rest of the developed world faces the same demographic headwinds and productivity challenges as the U.S., so it is natural for rates to be low globally.

However, there is a big "but." And that is the rest of the voting members of the Federal Open Market Committee (FOMC), who decide as a group where to set policy rates, don't necessarily agree. As noted above, the midpoint of the committee's forecasts are for rates to settle around 2.75% in 2019, as evidenced in the Fed's "dot plot." The St. Louis Fed's dot is the outlier by far.

You might ask, "so what?" Well, it matters whether policy becomes too constrictive. If other Fed officials believe rates should be two percentage points higher than where some economists believe is actually more appropriate, that can slow the economy. What may seem like a perfectly reasonable policy rate in another environment may be stifling in the current low rate/low inflation regime. In other words, overshooting the policy rate could, theoretically, send the economy into recession or even deflation. (Go ask Japan.)

As such, it matters a great deal where policy rates are set, not only because borrowing costs influence the economy through obvious channels, but also through the level of the dollar. When rates are higher here than elsewhere and inflation is low and stable, foreign capital flows into the U.S. That drives up the value of the dollar, making imports cheaper and our exports more expensive to the rest of the world. That amplifies the constrictive nature of a higher policy rate.

All of this looks ahead several years. We're quite a ways away from there, of course, but these are issues to bear in mind as one makes long term planning for the future. That's true whether one is a consumer, investor or business owner. Without making any predictions, one takeaway is that interest rates may not automatically increase by a large amount just because they are currently low. It may mean that low mortgage rates can further support housing, or that companies could continue to borrow at low rates. The upshot: this may only be the case if Bullard's argument holds sway with other policymakers.

Disclosure

Investing involves risk, including possible loss of principal, and investors should carefully consider their own investment objectives and never rely on any single chart, graph or marketing piece to make decisions. The information contained in this piece is intended for information only, is not a recommendation to buy or sell any securities, and should not be considered investment advice. Please contact your financial adviser with questions about your specific needs and circumstances.

The information and opinions expressed herein are obtained from sources believed to be reliable, however their accuracy and completeness cannot be guaranteed. All data are driven from publicly available information and has not been independently verified by United Capital. Opinions expressed are current as of the date of this publication and are subject to change, and they reflect those of the author and not necessarily United Capital. Certain statements contained within are forward-looking statements including, but not limited to, predictions or indications of future events, trends, plans or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties. Indices are unmanaged, do not consider the effect of transaction costs or fees, do not represent an actual account and cannot be invested to directly. International investing entails special risk considerations, including currency fluctuations, lower liquidity, economic and political risks, and different accounting methodologies.

© 2016 United Capital Financial Advisers, LLC. All Rights Reserved

See also Lowe's: What A 'Home Run' Investment Could Look Like on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}