Credit: Shutterstock photo

Credit: Shutterstock photoBy Logribel Biostocks :

TiGenix ( TGXSF ) -- listed on Euronext Brussels -- is a leading but little known Belgian cell therapy biotech with an advanced adipose-derived allogeneic stem cell product platform in various clinical stages. TiGenix also has a commercialized product (ChondroCelect) for cartilage repair in the knee, which was the first ever approved commercial cell-based product in Europe in 2009 (Advanced Therapy Medicinal Product).

TiGenix's most advanced clinical stage adipose-derived product is currently in phase 3 for the treatment of complex perianal fistulas in Crohn's disease patients (local injection of allogeneic adult stem cells, codename: Cx601). Results are expected in early Q3-2015 and if positive would allow for commercial launch in Europe in 2017. Commercial launch in the US could start around 2019 after completion of a single pivotal phase 3 if approved by the FDA -- following TiGenix's discussions with the FDA and the introduction of a Special Protocol Assessment in December .

TiGenix has also completed a phase 2a trial in refractory Rheumatoïd Arthritis patients and initiated in 2014 a phase 1b trial in severe Sepsis. Both of these indications are treated via intravenous injection of allogeneic stem cells (codename: Cx611). The company intends to launch a phase 2b trial in early RA in Q3-2015.

The eASC platform

One of the biggest challenges of cell therapies is the ability to deliver commercially viable finished products with reasonable production costs and high margins -- see the unfortunate example of Dendreon's ( DNDNQ ) Provenge which failed mainly due to expensive and complex manufacturing processes . This is a challenge TiGenix understands very well from its own experience with ChondroCelect , an autologous treatment for cartilage repair in the knee developed by the company and approved by the EMA in 2009. Although economically relevant and covered by national reimbursements in several European countries, ChondroCelect has not until now proven to be a commercial success, generating an expected net revenue of EUR 1m in 2014. This owes mainly to the very high production costs of the autologous stem cell treatment which result in narrow margins despite a relatively high selling price for Europe (EUR 20k per procedure).

Following this experience with ChondroCelect -- now licensed to Swedish Orphan Biovitrum ( BIOVF ) -- and based on a new expanded Adipose-derived Stem Cell (eASC) platform, TiGenix has chosen an allogeneic approach to develop all of its consecutive treatments. This new platform uses mesenchymal stem cells extracted and expanded from adipose tissues (fat) of consenting adult donors.

Adipose-derived mesenchymal stem cells benefit from numerous advantages over other cell types in terms of cell collection -- fat is a readily available tissue source collected through a simple and harmless liposuction -- and have a proven enhanced safety profile through well understood mechanisms of action. This therapeutic mechanism is based on the "natural" anti-inflammatory effect of the eASCs: it does not depend on cell differentiation, thereby reducing the risk of unforeseen cell type formation (no toxicity nor tumorigenic behavior) and it does not require HLA matching nor the use of immunosuppressors even though the cells are not a patients' own and come from donors (sources: here , here and TiGenix ).

TiGenix's eASC and chondrocyte (ChondroCelect) platforms are well-protected by a number of granted and pending patents in 20 jurisdictions including the US, with expiry dates of 2024 onwards (see here and here )

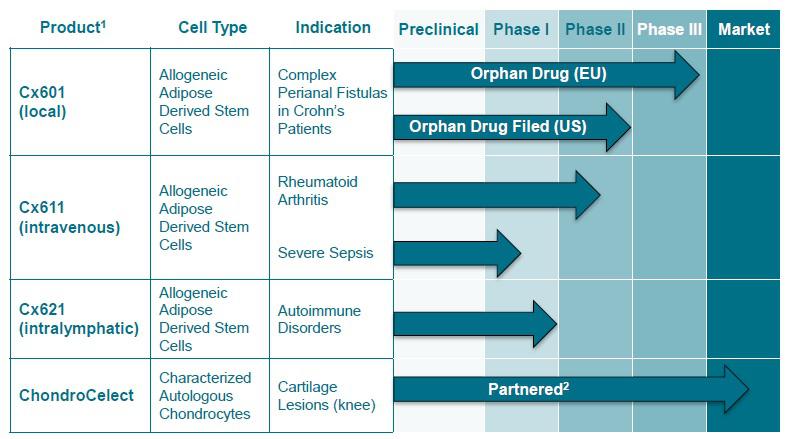

TiGenix's pipeline to date is mainly based on its eASC platform developments:

(source: TiGenix)

Cx601 -- allogeneic local injections

Cx601 is an adipose-derived allogeneic stem cell suspension for the treatment of complex perianal fistulas in Crohn's disease patients, currently in phase 3 in Europe. Recruitment of this robust phase 3 trial (278 patients across 50 centers, randomized 1:1, double-blind, placebo controlled) has been completed in November 2014 and first results are now expected in Q3-2015. Cx601 has been designated an orphan drug by the EMA (granting a 10-year market exclusivity after approval).

Perianal fistulas are a frequent manifestation of Crohn's disease. A perianal fistula is an abnormal connection between the perianal space and outside skin surface with an important negative impact on quality of life. It is a highly debilitating affection with an unmet therapeutic need as current treatments are generally marked by poor efficacy and high costs.

There are approximately 1 million new Crohn's disease patients each year in Europe and in the US (this equates to a very conservative 0.12% yearly incidence rate ). Within this population, it is estimated that approximately 12% of these patients (app. 120.000 patients) will be affected by complex perianal fistulas. With an annual treatment price of $20k this represents a total market opportunity in excess of $2 billion in Europe and US combined.

Current treatment options include antibiotics, immunosuppressive agents, biologics (Remicade or Humira) and as a last resort, surgery. All of these treatments have high recurrence rates (around 50%) and more advanced options like biologics (or antiTNF-alpha) have poor efficacy results ( 36% of remission for Remicade against 19% for placebo) despite high risks associated with such medications (see so-called " black box warnings ").

In phase 2 , Cx601 was well-tolerated and demonstrated a significant 56% efficacy rate (patients achieving complete closure of treated fistulas after 24 weeks) with maximum 2 doses of injected cells. Moreover, nearly 70% of patients achieved a reduction in the number of draining fistulas. This is a notable improvement on biologics (between 23 and 36% of efficacy) with a much more favorable safety profile, although on a rather small patient population (N=24).

The target population for TiGenix's Cx601 are patients refractory to antibiotics and/or immunosuppressants and failing at least one biologic. It is estimated that around 80% of all treated patients will fail biologics at some point in their treatment course (source : TiGenix ). Therefore, with a selling price of $20k and a market share of 35% this represents a $672 million opportunity in peak sales per year for TiGenix -- and this is taking into account very conservative population and pricing assumptions as TiGenix currently assumes that Cx601 average selling price could reach around $35k per year.

According to TiGenix's own previsions, completion of Cx601 European phase 3 in 2015 would allow the company to file its EMA application for market authorization in 2016, anticipating a commercial launch in Europe in early 2017. The same clinical results would also allow the company to start its US pivotal phase 3 in 2016, anticipating commercial launch in the US in late 2019.

Therefore, a 2024 sales forecast is anticipated to capture both European and US peak sales. See table 1 for a selling price / market share sensitivity analysis for Cx601 (base assumption = $672m) -- see Conclusion below for a comprehensive company valuation based on these anticipated sales.

- Table 1

Cx611 -- allogeneic intravenous injections

Cx611 is an intravenously-administered product of allogeneic expanded adipose-derived stem cells in development for early Rheumatoid Arthritis and severe Sepsis. TiGenix started in December 2014 a phase 1b trial in severe Sepsis and intends to start a phase 2b trial in early Rheumatoid Arthritis in Q3-2015.

Rheumatoid Arthritis ((RA)) is a chronic polyarticular inflammatory joint disease typically involving the small joints of the hands and feet that affects between 0.5 and 1% of adults in the developed world. Although there are already a number of treatment options for RA, it is estimated that approximately 20% of all patients do not have an adequate response to current treatment after failing several pharmacological options (DMARDs, immunosuppressants, biologics, etc.) (source: TiGenix).

A phase 2a trial in refractory RA patients completed in 2012 (53 patients, single-blind and placebo controlled) demonstrated good safety results and showed promising signs of efficacy . After only 3 injections of Cx611 (in combination with standard of care or DMARD ), 37% of patients were still good to moderate responders after 6 months, and 5 patients even remained in complete remission after the treatment (9% of 46 patients completing the trial) with no comparable placebo response. Although the study was not powered for statistical significance, these results were obtained in a very tough patient population as every patient treated had failed at least 2 biologics and had been diagnosed with the disease for a mean-time of 15 years. A graphic summary of those results is shown below.

(source: TiGenix)

These promising results in refractory RA patients will be the basis for a phase 2b trial due to start in Q3-2015. The aim will be to induce and maintain low disease activity in patients with early acute & inflammatory disease state, before transferring to biologics (like Humira). As global RA market is expected to grow to more than $18 billion in 2023 , there is of course a huge opportunity for an effective and safe treatment that fits within existing treatment protocol.

Severe Sepsis is a potentially life-threatening complication of infection where the whole body is subject to an inflammation caused by bacteria, fungi, viruses or parasites. If sepsis progresses to septic shock, blood pressure drops dramatically, which may lead to death. Patients with severe sepsis require close monitoring and treatment in a hospital intensive care unit.

As a proof-of-concept study, TiGenix initiated in December 2014 a phase 1b trial to test the mechanism of action of Cx611 in this indication. The trial is a randomized, placebo-controlled trial in which healthy volunteers will be challenged with a bacterial endotoxin to induce sepsis-like clinical symptoms. Results are expected in Q3-2015.

Sepsis is an affection of complex nature and its variable presentation has made it hard to develop therapies. Cx611 could be added into current clinical management, representing a good therapeutic and commercial opportunity in an unmet clinical need.

Cx621 -- allogeneic intralymphatic injections

Cx621 is an allogeneic eASC product candidate for the treatment of autoimmune diseases via a proprietary technique of intralymphatic administration. TiGenix is exploring this administration route with the hope that the systemic effect of the adipose-derived stem cells could occur at the secondary lymphoid organs, propagating the anti-inflammatory effect to draining lymph nodes and spleen.

TiGenix completed a small exploratory phase 1 (randomized and placebo-controlled) in 2012 in 10 healthy volunteers. Safety results were good , with no severe adverse events reported.

Manufacturing processes and margins

Owing to the allogeneic nature of its stem cells platform and thanks to a robust and uniform manufacturing process for all of its eASC products (Cx601, Cx611 and Cx621), TiGenix is able to considerably improve product margins over autologous products.

Indeed, liposuction from a single healthy donor could provide as much as 2.400 doses of Cx601 and 4.000 doses of Cx611 at current trial dosing. With an assumed cost of goods of EUR 1.500 (source : Edison Research ) and an estimated selling price of minimum EUR 15.000, this would equate to a at least 90% gross product margin, in line with pharmaceutical industry's best performers .

(source: TiGenix)

Clinical trials and competing stem cell therapies

A number of cell therapy companies in the world have been conducting clinical trials and developing stem cell platforms. Some of them could be compared with TiGenix's allogeneic eASC platform.

The biggest company involved in allogeneic stem cells is Mesoblast ( MEOBF ), an Australian company which acquired Osiris' ( OSIR ) Prochymal -- a pioneering but controversial product -- in 2013 and is also developing its own Mesenchymal Precursor Cell (MPCs) platform. Both products use expanded bone marrow-derived allogeneic mesenchymal stem cells. Mesoblast has a number of phase 2 and 3 allogeneic assets, including one ongoing phase 3 trial in Crohn's disease patients with Prochymal in which it intends to look for " evidence of efficacy in high-risk groups such as those with fistulizing disease ". However, this shouldn't represent any foreseeable competition for TiGenix's Cx601 on the US market, as Mesoblast has not yet reached any decision on a specific orientation towards a treatment for fistulas and does not have to this date any efficacy data on this indication. Mesoblast also has a small ongoing phase 2 trial in Rheumatoid Arthritis (48 patients, completion date H1-2015) targeting patients refractory to biologics (antiTNF-alpha). Mesoblast is currently valued at $1.1 billion (with approximately $250 million in cash).

In April 2014, Athersys (ATHX) stopped early a phase 2 trial of MultiStem (allogeneic bone-marrow derived mesenchymal stem cells) in Ulcerative Colitis -- an Inflammatory Bowel Disease closely related to Crohn's disease -- after it failed to prove significant efficacy in an interim analysis . The trial was being conducted by Pfizer (PFE) under a collaboration and license agreement with Athersys. To this date, the company is admittedly pursuing evaluation of 16-week data, including the impact of second round dosing for a subset of patients.

Despite some Crohn's disease related trials with stem cells not faring so well in recent years, it is interesting to note that a private South-Korean company, Anterogen, has developed a product using autologous adipose-derived mesenchymal stem cells specifically designed to treat fistulas in Crohn's disease patients. This product, Cupistem , has been approved in 2012 in South-Korea following a phase 2 trial in which the treatment demonstrated 82% efficacy (full closure of treated fistulas in 27 of 33 patients completing the trial). Similarly, before turning to allogeneic stem cells, TiGenix tested its own autologous adipose-derived stem cells (codename : Cx401) in several clinical trials totaling 154 treated patients with efficacy results ranging from 40 to 75% (source: TiGenix). Therefore, there appears to be repeated clinical evidence of efficacy in autologous treatments of fistulas and some evidence of allogeneic efficacy as well (Cx601 phase 2 results). The main question right now is to see if these results will be reproduced in a large scale allogeneic trial like TiGenix's Cx601 phase 3 trial (278 patients); the answer should come in early Q3-2015.

Management team experience

So far, TiGenix has a proven track record of clinical trial successes to which an experienced and pragmatic management team is no stranger.

Current CEO Eduardo Bravo -- who took over the lead with TiGenix's 2011 merger with privately-held Spanish company Cellerix -- has more than 25 years of experience in the pharma industry, including positions held at Sanofi-Aventis (including Vice President for Latin America), Cephalon (acquired by Teva) and SmithKline Beecham.

Worth mentioning as well is the presence on TiGenix's board of directors of Jean Stéphenne , former boss of GlaxoSmithKline Biologicals (GSK).

In September 2014, TiGenix strengthened its management team with the appointment of a Chief Medical Officer and a Vice President Medical Affairs and New Product Commercialisation. These new members are to be in charge of preparation and implementation of the development plan of Cx601 in the United States and commercial launch in Europe.

Key events and coming milestones

The most important event in the coming months for TiGenix will be the results of Cx601 phase 3 trial due for Q3-2015. In H1-2014 conference call, management indicated a probable release in early-Q3, so results could be available as soon as July 2015.

Other notable milestones are shown below according to TiGenix's official previsions.

(source: TiGenix)

Potential risks

TiGenix's future mainly depends on the success or failure of the ongoing phase 3 trial of Cx601, as other prospects are still in early-stage developments (phase 1/2). Bigger trials may not replicate the good results of smaller ones. Upon disappointing results, the company's valuation could well be consequently and durably impacted -- as Cx601 represents a significant amount in the company's current valuation, a downside in the range of -75% in worst case scenario is not unlikely.

With $22.5 million of cash available as of 30th September 2014, management has confirmed that -- at current cashburn -- TiGenix has sufficient funds to cover operations until after Cx601 phase 3 results. Nevertheless, additional cash will be needed to fund a pivotal US phase 3 for Cx601 and the commercial launch in Europe. These funds could be obtained via loans, partnering and/or capital increase -- the latter resulting in shareholder's dilution and potential downside depending on applied discount.

Conclusion and valuation model

With a current market cap of $100 million, I believe TiGenix's valuation offers a rare investment opportunity with a clear timing perspective (Q3-2015) and a favorable risk/reward profile -- owing to previous clinical results.

According to my risk-adjusted NPV valuation model and considering 2024 peak sales (EU + US) of $672 million -- see sensitivity analysis above -- I estimate current fair value of TiGenix to be at $250 million (or app. $1.50 per share). This represents a 130% upside on the share price at time of writing (app. EUR 0.55 or $0.65).

To reach this valuation, I assume a conservative probability of success for Cx601 phase 3 EU trial (65% despite proven efficacy) and somewhat lower chances (55%) for the US trial due to uncertainties on partnering and protocol details. Commercialization in Europe is estimated to bring a 30% royalty revenue to TiGenix -- although direct sales could probably result in higher margins -- and a 20% royalty rate is assumed for US sales. In the meantime, ChondroCelect sales are estimated to grow slowly to an estimated $2 million revenue.

As of now, Cx611 and Cx621 valuations are not specifically forecast as TiGenix has yet to prove significant clinical efficacy and define further strategic options. However, potential for these promising developing assets is included in a 20x multiple of 2024 net profits in the company's valuation model below.

See Table 2 below for summary of my valuation model's main assumptions (rNPV at 15% discount).

- Table 2

I estimate that a success in Cx601 phase 3 trial could bring the valuation of TiGenix close to $300 million or higher by year's end -- due to revised risk probabilities on Cx601 clinical trials -- and open the way for high value partnering or buy-out deals. Indeed, TiGenix could become one of the very few companies in the world with a clinically successful allogeneic stem cell platform and the potential to deliver a commercially viable "off-the-shelf" product on an orphan market estimated in excess of $2 billion annually.

Disclosure: The author is long TGXSF. The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it. The author has no business relationship with any company whose stock is mentioned in this article.

See also U.S. IPO Weekly Recap: Big Data Produces Small Returns In A Selective IPO Market on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}