Credit: Shutterstock photo

Credit: Shutterstock photoBy Jeff Young :

Editor's note: Seeking Alpha is proud to welcome Jeff Young as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Pro.Click here to find out more »

The S&P 500 Index: A Backgrounder

We will use the S&P 500 Index ( SPY ) as a proxy for the broader stock market. Our orientation here is towards capturing broad tendencies ("the forest"), rather than more isolated patterns ("the trees") which may be less representative.

The S&P 500 Index as we know it today was born on March 4, 1957. Between 1926 and 1957, the index consisted of only 90 stocks. One point to keep in mind - since the S&P 500 Index as reported does not comprehend dividend reinvestment, the returns implied by comparing changes in the index over time are lower than would be the case if dividends were accounted for. For example, the S&P 500 Index increased at a compound annual rate of 6.2% between the end of 2007 and the end of 2017, but if you bought the index through an exchange-traded fund like SPY at the end of 2007 and reinvested the dividends you received from it, your annual return through the end of 2017 would be 8.4%.

Investing 101: A View from 20,000 Feet

If we want to understand better where we are going, it is helpful to know where we've been. To facilitate this, I share below a long-term view of the performance of the S&P 500, going back to 1871. Although as noted previously the S&P Index goes back only 60 years, that is not sufficient for the analysis we want to undertake. Consequently, we will piggyback on the work of a luminary in the investing world, Robert Shiller - the author of Irrational Exuberance . Shiller's website provides a backcast of the S&P 500 Index going back to 1871, which he constructed by using comparable indices that are available for these earlier time periods as proxies.

Here we are looking at the S&P on an inflation-adjusted basis (i.e. "real" rather than "nominal") to provide more of an "apples-to-apples" comparison across a period that spans many generations. The graph is presented on a logarithmic scale to allow for consistent comparisons on a relative basis at different price levels, and results reflect reinvestment of dividends to allow tracking of total returns. 1

The consistency in returns over time is striking. During the postwar period (January 1946-December 2017), we see a 6.9% inflation-adjusted CAGR - identical to the gains shown prior to this (January 1871-December 1945). However, the composition of these returns differs markedly between these time periods:

Given the persistent pattern shown above, we observe that when the S&P index (inflation-adjusted, and comprehending dividend reinvestment) is below its long-range trend, subsequent gains will be higher than average, as the index tends over time to "regress to the mean" (i.e. the trend line); conversely, when the index is above its long-range trend, subsequent gains will be lower than average.

This is a useful guide and should help us in managing our expectations as to what the future holds, but it does not give us sufficiently precise and actionable information onto which we can base our investment decisions - so we will need to explore this relationship more deeply.

A Framework for Valuing the Stock Market

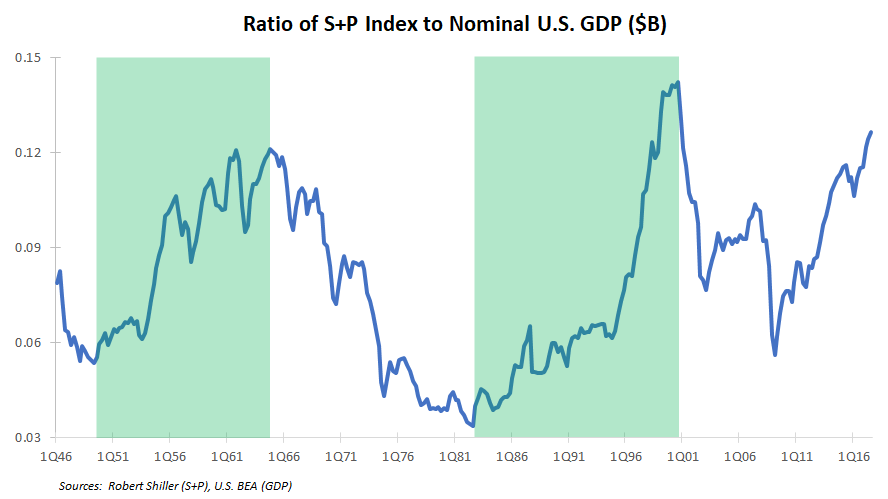

We'll begin constructing our framework with an assist from the man whom many consider to be the world's greatest investor. In 2001, Warren Buffett observed in a Fortune Magazine interview that market cap to GDP (now oftentimes referred to as "the Buffett Indicator") is "probably the best single measure of where valuations stand at any given moment". We want to take the long view here, and many measures of market capitalization (such as the Wilshire 5000) do not provide a very lengthy historical time series; consequently, we will use Shiller's S&P 500 as a proxy. For the reasons noted previously, our analysis will focus on the postwar period.

Our source of U.S. GDP data is the Bureau of Economic Analysis. If we compare the S&P Index with nominal GDP for each quarter during the postwar period, we see the following (areas highlighted in green mark periods of rising ratios):

You'll notice that this measure exhibits some apparent periodicity - a trough in 2Q49, followed by a peak in 1Q65 (16 years later), another trough in 3Q82 (17 years later) and a peak in 3Q00 (18 years later). This pattern of 15 to 20 year cycles is consistent with that posited by Michael Alexander in his provocative book Stock Cycles: Why Stocks Won't Beat Money Markets Over the Next Twenty Years - published in October 2000, which happened to coincide with the 3Q00 peak referenced above.

Developing the Framework

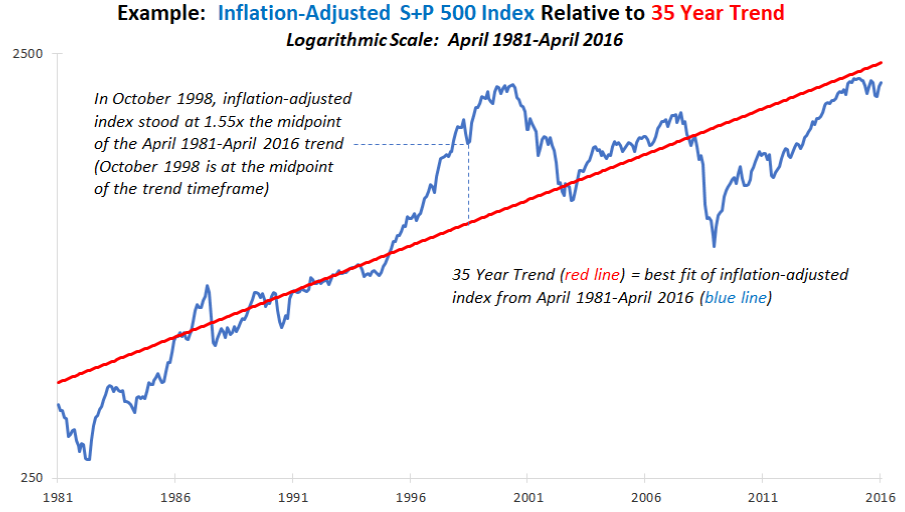

Alternating uptrends and downtrends of 15-20 years each yield a complete cycle (uptrend plus downtrend) of around 35 years. Comprehending one complete cycle in our valuation measure should ensure that this measure is not being influenced by the periodic extremes of share prices that take place during these 15 to 20 year upturns and downturns, as the extremes will tend to offset each other, and each 35-year cycle will have one of each extreme. We calculate a valuation measure for a given month by taking the S&P 500 Index relative to the midpoint of the 35-year trend that surrounds it (17½ years before the month indicated, and 17½ years after it) 2 :

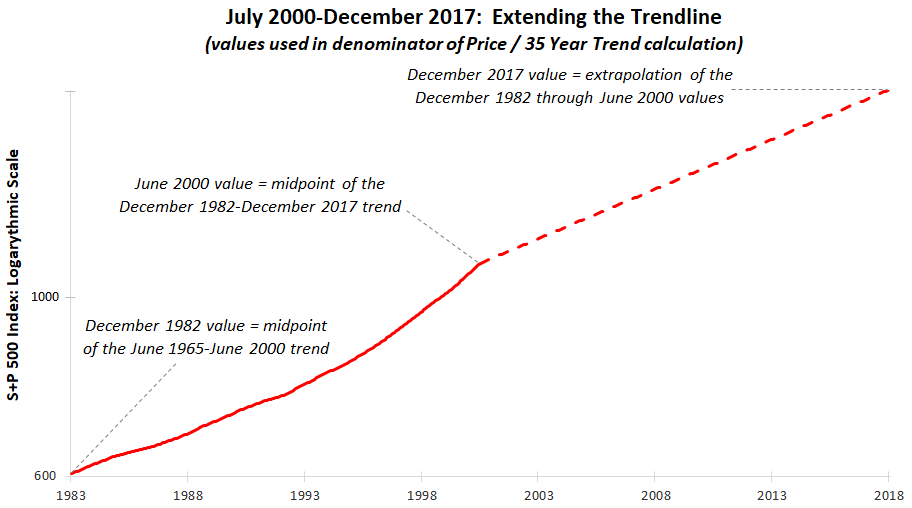

This works nicely in principle - but it won't be suitable for more recent history (starting in August 2000) since the relevant 35-year trend for these months will extend into the future. For example, the 35-year trend whose midpoint is December 2017 would span the period from June 2000 to June 2035. In this case, we will instead extrapolate the midpoint of the 35-year trends for each month from December 1982 to June 2000:

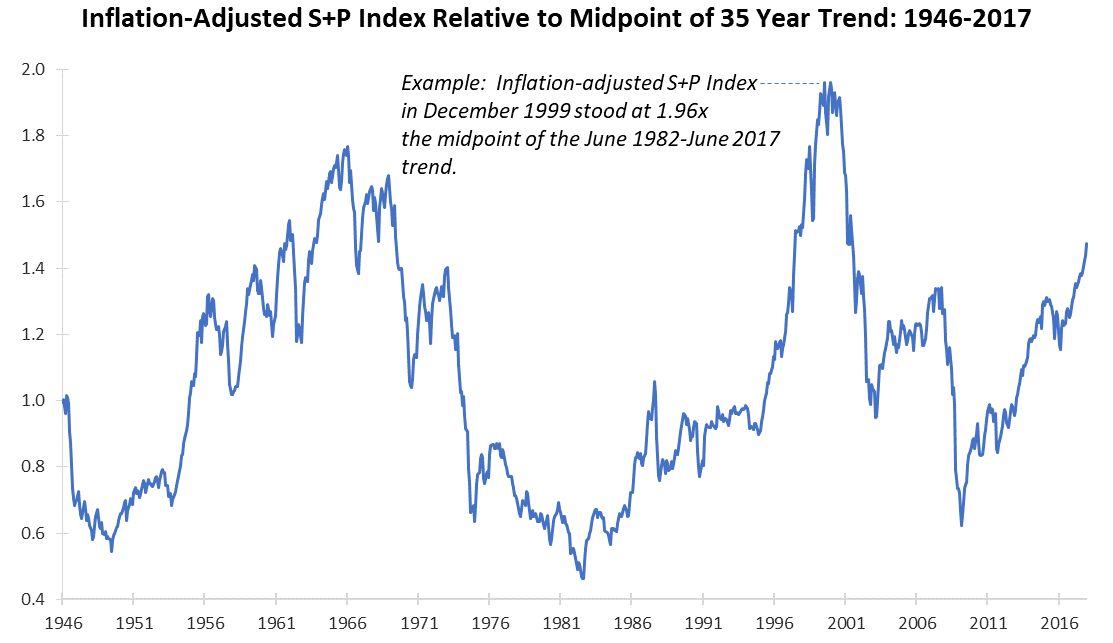

Not surprisingly, when we calculate a historical time series for our measure of the S&P index relative to trend, we see a pattern consistent with the "Buffett indicator" 3 :

Applying the Framework

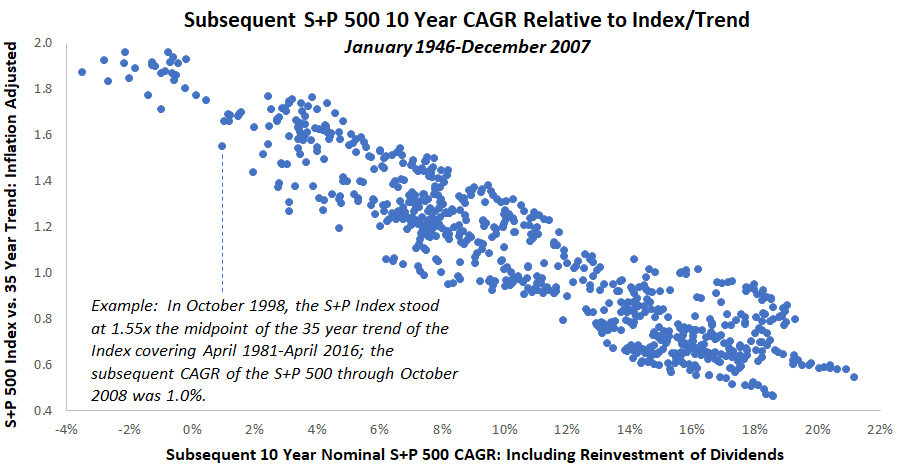

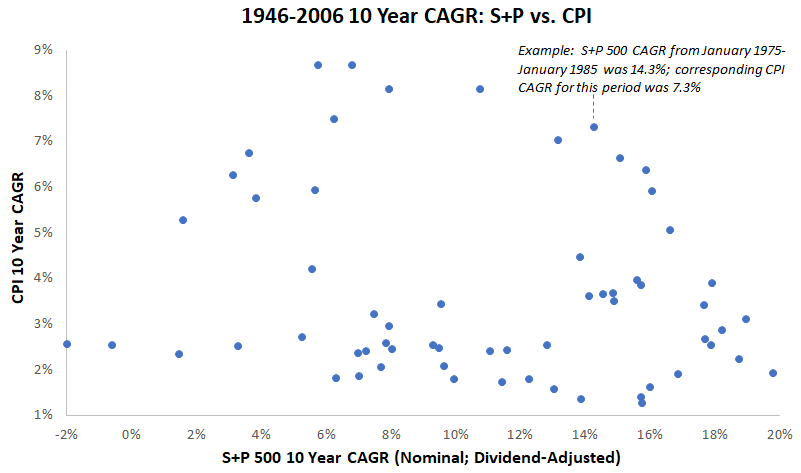

As suggested earlier, the logic behind calculating a valuation measure is that (for example) periods of high valuation should be followed by sub-par market returns, given the previously demonstrated tendency of the S&P index to regress to the trend line. But does this tendency play out in practice? Let's look at the numbers. Here we will compare our valuation measure for each month from January 1946 to December 2007 with subsequent 10-year returns:

We see in the graph above a pretty clear relationship. If we draw a best fit through the points in the graph, we come up with a formula for projecting the 10-year S&P nominal 4 annualized return, including re-investment of dividends:

10 Year CAGR = 25.6% - 13.7% x (Price / 35 Year Trend) 5

Given the January 2018 price-to-trend ratio of 1.53, this equates to a projected 4.5% CAGR for the 10-year period that runs through January 2028.

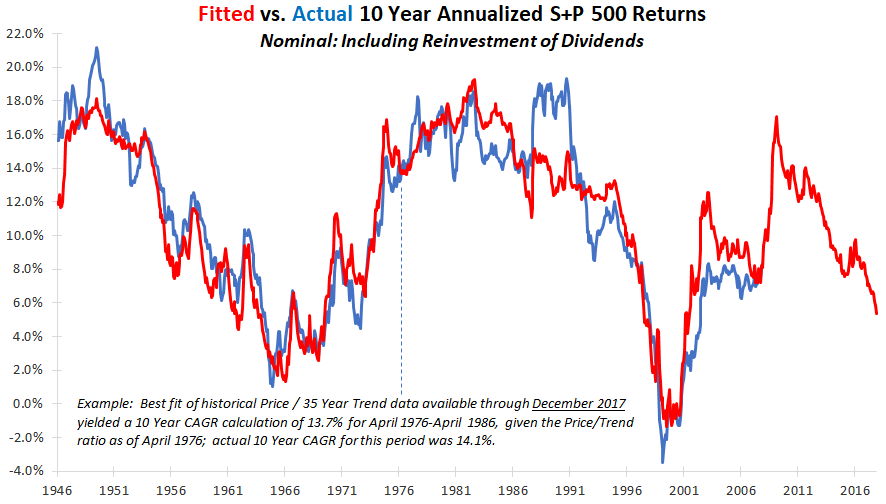

When we compare projected 10-year returns using our formula above with the actual 10-year returns that subsequently transpired, we see the predictive power of this relationship:

Can we expect this equation will anticipate future returns as accurately as it has done in the past?

No!

The coefficient and intercept in our equation have been calculated to produce the best fit with subsequent 10-year returns over the historical time frame, using those very same 10-year returns to minimize the difference between fitted vs. actual subsequent 10-year CAGRs through December 2007. Going forward, however, we won't know ahead of time what coefficient/intercept will best anticipate future returns, and hence we won't have the ability to "train" our equation to fit these returns as closely as possible. To cite an extreme example, you may be familiar with the infinite monkey analogy - winners of the primate typing competition won't likely perform as well going forward as they did in the past, to the extent that luck or nonrecurring factors contributed to their previous performance.

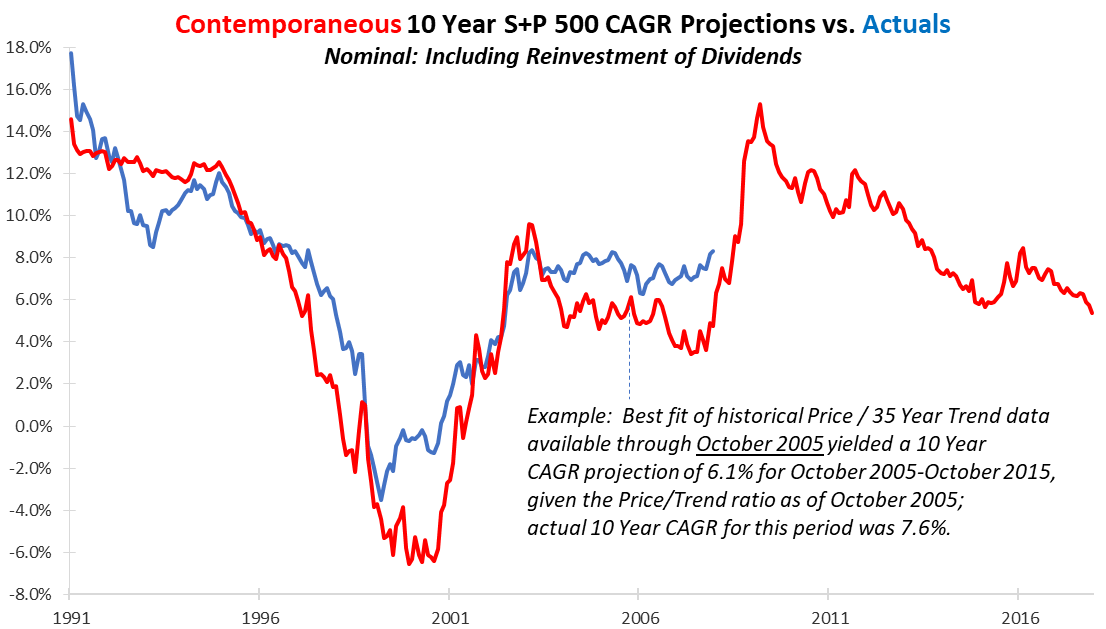

To get a better idea as to the predictive power of our model, we need to assess its performance based on contemporaneous data, i.e. without any foresight. For example, in developing a model to project the 10-year CAGR for October 2005-October 2015, we would want to calculate a coefficient/intercept that produced the best fit based only on historical data that was available through October 2005. We can do this for each month from January 1991 to January 2008. 6

So how good does the model perform if we deprive it of foresight? Not quite as well as in our previous example, but the results are still quite impressive:

Contemporaneous projections are the "gold standard" to use in validating the predictive power of a model, and in determining potential margin of error in the model output. It is the difference between these contemporaneous projections vs. subsequent actuals that we will use in determining the probability distributions of outcomes in our forecast of 10-year S&P returns.

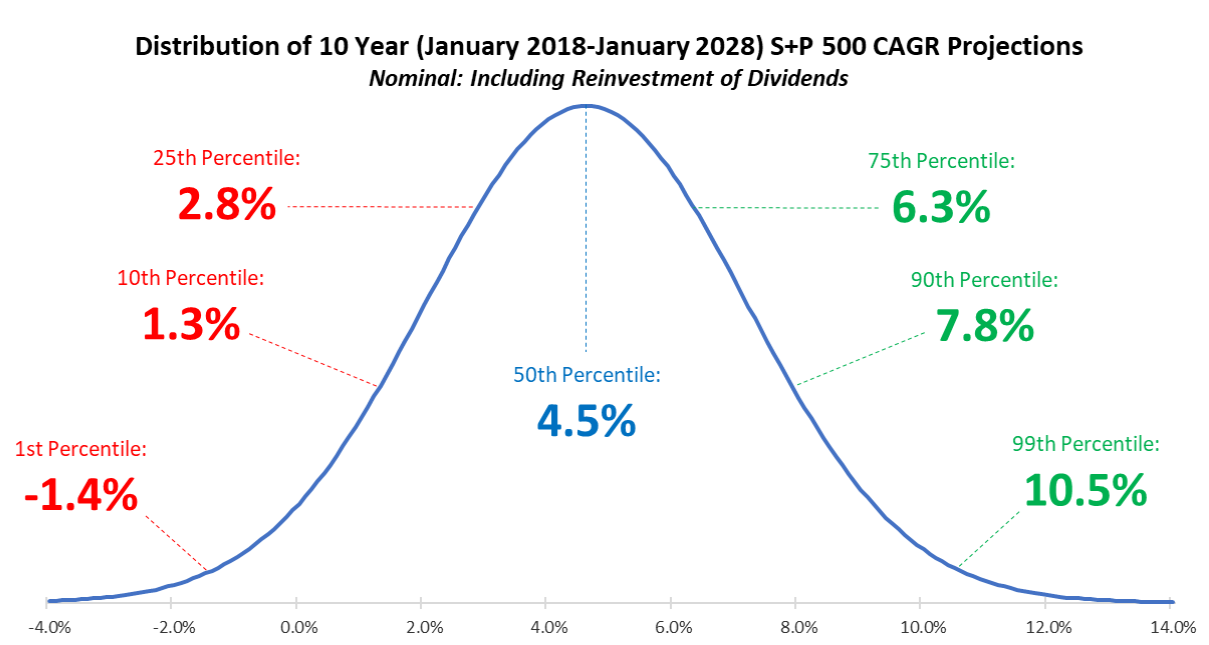

For example, the standard error of our contemporaneous projections is 2.6% - which means that approximately two-thirds of the time, the subsequent 10-year CAGR came within 2.6 percentage points of our projection. 7 Given this historical performance, we therefore anticipate that S&P returns over the January 2018-January 2028 time frame will fall within 2.6% of our projected 4.5% CAGR approximately two-thirds of the time, which equates to a range of 1.9% to 7.1%. 8

The Bottom Line

The Stock Market Sanity Equity Valuation Model will be updated each month; the resulting projected distributions of 10-year S&P returns will appear on the landing page of our website, stockmarketsanity.com :

One caveat to note here…as indicated previously, we saw a paradigm shift with the advent of the postwar period, which was accompanied by greater (or at least more effective) use of monetary and fiscal policies to moderate and lengthen the business cycle. This environment has fostered a degree of stability which has enhanced the predictive power of our model. In the future, it is always possible that a new policy regime will emerge, which could undermine the ability of previous tendencies to anticipate future outcomes. Until we have evidence that this is taking place, however, we will revert to the "null hypothesis" that historical patterns are relevant indicators of future outcomes. And conversely, it is also possible that the predictive power of our models will improve in the future, as they are given a longer historical time series to train themselves against.

One Final Note

Does the 1Q09 value in the "Buffett Indicator" graph shown previously represent an end to the downturn which began in 3Q00 (which would undermine the notion of regular 15 to 20 year cycles), or will the increase in this measure since 1Q09 be wiped out by a new downturn that will establish a lower trough and an end to the cycle which began in 3Q00? I believe that the future is unknowable, so it is impossible to say with certainty, but the next recession - whenever it occurs - is likely to be accompanied by a significant decline in the S&P relative to GDP, if history (most recently the recessions which commenced in March 2001 and December 2007) is any indication. Forewarned is forearmed, so we'll study the conditions that preceded past recessions and the range of outcomes associated with them a future update.

Stay tuned.

Notes

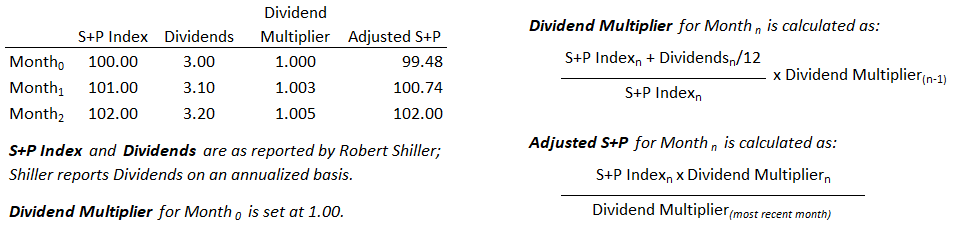

1 Here is an example of the methodology used to adjust for dividend reinvestment:

2 Using the midpoint of the trend for the 35-year period that surrounds it as the basis of our calculation for a given month ensures that the position of this month within the cycle will have negligible effect on the calculated valuation measure; conversely, if we calculate our valuation measure on the basis of a trailing trend (i.e. December 2017 price relative to December 1982-December 2017 trend), the valuation measure will tend to be whipsawed during months that are at the extreme peaks and troughs of the cycle.

3 Given the consistency of our measure with the Buffett indicator, you may be wondering why we don't just use the Buffett indicator as the basis for our valuation measure. One shortcoming of using GDP (as the Buffett indicator does) in a calculation of stock market valuation is that historical GDP figures are periodically revised; in contrast, our measure relies only on the S&P index, which will not undergo subsequent revision.

4 You might reasonably ask why we are projecting nominal (rather than inflation-adjusted or "real") S&P returns, particularly given that the 35-year trends we are using in our calculations reflect inflation-adjusted numbers. As luck would have it, historical data (one observation per year, using January as our point of reference) shows that nominal S&P performance has been relatively immune to the inflation environment (r-squared is only 0.02):

This means that if we are to forecast inflation-adjusted S&P returns, we must comprehend a forecast of the inflation rate, which has proven to be notoriously difficult to predict (as anyone who sold 10-year Treasuries in September 1981 - when they were yielding a whopping 15.32% - can attest). Given this, it's not surprising that the predictive power of our model is stronger for nominal returns than it is for inflation-adjusted ones. Since fixed income alternatives (outside of TIPS) are generally denominated in nominal terms, the utility of our model in evaluating alternative asset allocations is not unduly compromised by a reliance on projections that are also stated in nominal terms. Of course, if you would like a forecast in inflation-adjusted terms, you can apply your own 10-year forecast of inflation to Stock Market Sanity's nominal projections.

5 For you statistics jockeys out there, here are the relevant diagnostics for this equation:

6

7 This Standard Error compares favorably with the corresponding value of 2.0% for the projections that employ foresight, as shown in footnote #5 - this relatively small difference suggests that overfitting is not a significant problem in our model.

8 Given the limited historical time frame (205 months) available to us, we will assume that our forecast error is distributed normally. If we compare the distribution of forecast error from our contemporaneous projections vs. what might be expected from a normal distribution, the two appear to line up quite well, except for the fact that the normal distribution demonstrates more of a "long tail" - not surprising, given that the relatively short time frame available to us in the contemporaneous projections limits our opportunity for outliers:

See also Boston Scientific Corporation 2017 Q4 - Results - Earnings Call Slides on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}