Credit: Shutterstock photo

Credit: Shutterstock photoBy Evan Powers :

As political and economic uncertainty continue to rise on what seems like a daily basis (particularly in this election cycle ), the allure of the Roth IRA - and its younger cousin, the Roth 401(k) - also steadily grows. Indeed, data from the Employee Benefit Research Institute suggests that total balances in Roth accounts increased at twice the rate of traditional retirement accounts in recent years, spurred largely by a surge in traditional-to-Roth "conversions" (which, as I've investigated previously , can be a savvy move for many recent retirees).

The younger generation is particularly enamored of Roth accounts, as investors age 34 and under have more than eight times as many dollars invested in Roth IRAs than in their Traditional IRA counterparts. Much of that gap stems from an expectation that higher tax rates are inevitable in the future, as the nation eventually adjusts to its ever-worsening fiscal position . Regardless of the wisdom of such a decision, the question that has often gone unanswered is: once you've established a Roth account, how should it be invested? What kinds of assets should it (or shouldn't it ) hold?

Most analysis on the topic tends to conclude that it's best to stash your "most aggressive" investments inside your Roth, reasoning that those investments will have the highest returns over the long run, and hence the greatest potential benefit from tax-free growth. Since the most aggressive investments tend to be on the equity side of the ledger (rather than the fixed income side), this yields some common recommendations: Roths should hold small-cap stocks, or international stocks (perhaps emerging markets stocks), speculative growth stocks , or maybe even new IPO issues .

That basic reasoning seems to be sound, but is it really the best advice? Like most portfolio decisions, a decision on how to invest a Roth must take into account the totality of an investor's portfolio allocation, and be considered holistically, not in isolation. So before you go piling all of your favorite triple-leveraged ETFs into your Roth IRA, here's a quick primer on how best to approach the decision.

Consider asset location basics

As investment returns have come under pressure due to experimental monetary policies , the practice of tax-optimizing a portfolio has grown in popularity and importance. The focus on tax optimization has fueled an interest in asset location strategies, which aim to minimize overall tax bills by holding the right investments in the right types of accounts.

Classically, this has meant stacking tax-inefficient fixed income investments in tax-deferred retirement accounts, while concentrating equity investments in taxable investment accounts. That practice has three primary benefits, which can be summarized as follows:

- Fixed-income investments that would otherwise generate taxable income each year can defer tax on those periodic payments, yielding greater compounded returns inside the IRA

- Returns on equity investments that would ultimately be taxed at ordinary income rates if held in an IRA can qualify for preferable long-term capital gains rates by being held in a taxable account

- Volatility in equity investments can potentially create opportunities for tax-loss harvesting in a taxable account. Tax losses on equity investments held in an IRA cannot be used to shelter other taxable investment gains (but, note Michael Kitces' caveat on the benefits of tax-loss harvesting)

While these might on the surface seem like minor issues, the impact on an overall portfolio can in fact be quite significant over a long time horizon.

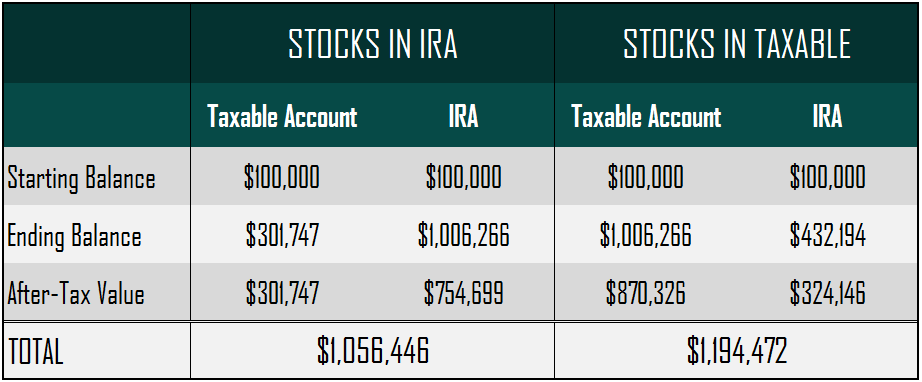

Consider the following table, which shows the theoretical difference between a portfolio that has not been tax-optimized (bonds in taxable account, stocks in IRA) and a portfolio that has been fully tax-optimized (bonds in IRA, stocks in taxable).

Assuming investment returns of 8% on stocks and 5% on bonds (with an ordinary income tax rate of 25% and a long-term capital gains rate of 15%), we see the following:

In this case, the difference between the two portfolios is more than $138,000, which amounts to a full 69% of the original investment amount! The recommendation, then, to hold high-return stocks in a Roth IRA - or in any type of IRA - flies directly in the face of classic asset location best practices! (Note that for the preceding calculations, we've assumed that the IRA is a Traditional IRA, not a Roth. That difference can be ignored as irrelevant for this portion of the analysis, since our assumption of constant tax rates means that Roth and Traditional accounts will yield essentially the same outcomes over the long run).

However, there are some significant limitations to the classical analysis with respect to asset location strategies, limitations that will vary in impact from one investor to another - and from one investing environment to another. Here are those limitations:

Problem #1: Stocks pay dividends

The biggest problem with the classic asset location analysis (as presented above) is that it assumes perfect tax efficiency on the equity portion of the portfolio - in other words, 100% of the investment returns can be attributed to long-term capital gains (rather than dividends), and those gains continually compound over time until the stocks are liquidated in retirement.

Of course, in the real world, this is hardly ever the case. Even the broad-based S&P 500 Index currently pays a dividend yield of roughly 2%, and its historical average yield is in fact closer to 4%. And if we amend our original asset location analysis from above to include some tax drag from dividends, the picture changes pretty dramatically.

Assuming the same 8% annual return on stocks, but with 3% of that total return coming from dividends (and the remainder from capital gains), here is what we see:

The $138,000 benefit from tax optimization has been slashed almost in half (to ~$77,000), just from the introduction of a 3% annual dividend yield (and an attendant "tax drag"). This tax drag would in fact be even worse than that, except that most dividend payments currently qualify for preferential tax treatment , rather than ordinary income treatment. If that tax treatment ever changes, so too would the math.

Obviously, some sectors (like utilities and financials) will have even higher dividend yields than has been modeled here, while others (like technology) will be lower, so the impact of this tax drag will likely vary from one investor to another. The potential benefits of asset location, then, cannot be considered static or universal. As the dividend yield on the stock portion of a portfolio changes, so too will the viability of standard asset location strategies.

Problem #2: Portfolio turnover

Also embedded in the classical analysis is an assumption of zero portfolio turnover (and hence, zero annual capital gains tax). Again, in reality, this is almost never a reasonable assumption - even basic rebalancing strategies can introduce 5% to 10% portfolio turnover annually, and active investment strategies (whether via active trading by a DIY investor or via actively managed mutual funds ) can easily bump that figure as high as 50% or more.

Even more so than dividends, that kind of turnover (and annual capital gains generation) can rapidly tilt the tax-optimization scales in the opposite direction. The math can vary somewhat when incorporating turnover assumptions, but as a general rule of thumb, an annual turnover rate of 20% or greater on the stock portion of an investment portfolio can flip asset location on its head, making it financially optimal to hold stocks in an IRA, rather than in a taxable account.

So, for investors who prefer active strategies on the stock side of their portfolio, tax-optimizing a portfolio may mean doing the exact opposite of the traditional advice.

Problem #3: Changing portfolio composition

A final consideration that will add to the turnover ratio is the life cycle of portfolio allocation, and how that may generate tax liabilities over time. Remember, if an investor were to fully embrace the classic asset location advice (and hold all equity exposure in a taxable account), then we would expect to see the taxable account continually grow at a more rapid pace than the IRA, to the point where rebalancing the portfolio would eventually require the investor to hold some fixed income securities in the taxable account, just to keep balanced.

Indeed, if we look back at our original asset location analysis (reproduced below), the beginning portfolio was perfectly balanced between stocks and bonds ($100,000 in each, split between the two accounts). But, after 30 years of compounding returns, the portfolio allocation had shifted dramatically toward stocks!

Without engaging in any rebalancing along the way, the ending portfolio (assuming stocks held in the taxable account) is composed of 70% stocks, 30% bonds, representing a significant drift from the original 50-50 allocation. Of course, anyone familiar with target-date funds (or with the "glide path" theory that guides their investing approach) knows that this is the opposite of the classical advice, which suggests that investors should decrease stock exposure as they age, not increase it.

Of course, taking action to correct the imbalance would even further eat into the theoretical benefits of asset location strategies. Over time, not only would annual capital gains on the taxable side be necessary in order to restore balance, but systematic liquidations would also be necessary, in order to gradually de-risk the total portfolio. Since there would be no initial stock exposure on the IRA side at all, there would be no opportunity to do this rebalancing in the IRA, and all moves would have to be made in a taxable account, thus generating additional capital gains tax.

In practice, though, this final point ends up being the least important one to investors, even though its impact is theoretically quite large. That's because most individual investors don't have anywhere near the initial 50-50 balance between taxable investments and tax-advantaged investments that we modeled - on the contrary, most investors have almost all of their investments tied up in IRAs or 401(k) plans of some sort or another, with a relatively small amount invested in taxable accounts. Still, it's a dynamic that bears mentioning and watching, since it can be quite a significant factor for some (usually higher net worth) investors.

So, what should we put into the Roth?

All of this is to say that there is no one-size-fits-all advice for what types of assets to hold in a Roth (or in any tax-advantaged account, for that matter). The advisability of what sorts of investments to hold in a retirement account will vary significantly based on the nature of the investments held, the frequency with which they are bought and sold, and trends in overall portfolio allocation.

To decide what to hold in a Roth, then, we recommend a four-step process for investors, one that takes into account a full-portfolio view.

Step 1: Determine current and future asset allocation

First, decide how much risk you want to hold in your portfolio (perhaps informed by a risk tolerance assessment), and how you'd ideally like to change that portfolio risk over time. Some investors will choose a highly risky (equity-heavy) portfolio that has a fairly steep "glide path" toward lower risk over time. Others will choose a more conservative allocation, with a shallower glide path (a more constant allocation over time).

This initial allocation will largely dictate the ability to which you can (or cannot) tax-optimize your portfolio. An investor who, for example, wants to hold 80% stocks but has 50% of his investment assets in each type of account will not have full flexibility to stack all of one asset type in one type of account. Some split of assets will be necessary, due simply to the disparity between the 80% figure and the 50% figure.

Step 2: Select specific securities and a desired trading strategy

Just knowing that you want to hold, say, 60% stocks and 40% bonds is only half the battle. Do you want to own high-dividend utilities stocks, or more speculative growth stocks? Do you plan to trade frequently (or invest in actively managed funds), or is a more passive investment approach more your style?

As we've mentioned above, a passive approach with low dividend payments will tend to benefit from a classic asset location strategy, whereas a more active approach with higher dividend payments could skew in the opposite direction. Knowing the characteristics of your investments - and how you intend to interact with them - is a key step in deciding which investments to hold in which types of accounts. In fact, it's almost certainly the most important step.

Step 3: Determine which of those investments are appropriate for a taxable account

Depending on the characteristics of the investments you've chosen, you should be able to determine which assets are best held in the taxable account, and which are better placed in a tax-advantaged account. Again, as we've shown here, that determination will vary from investor to investor.

You cannot skip the first two steps and hope to make a proper decision as to what investments to hold in a Roth IRA (or in any other type of retirement account). A full understanding and accounting of the total portfolio view - and how that view will change over time - is an essential step to making an intelligent decision regarding which investments to hold where.

Step 4: Now, put the most aggressive investments in the Roth

Now, and only now, should the most aggressive remaining investments be placed in the Roth account. Note that the decision regarding overall asset location must be made first , before this final step can be completed.

For an investor who has determined in the first three steps that classic asset location strategies are indeed appropriate given their situation, it's likely that higher-yielding fixed income investments will be the best candidates for a Roth. Indeed, this is the case for many investors that I encounter in my practice: as a result, high-yield bonds and REITs end up being frequent targets for inclusion in Roth accounts.

If, however, an investor has determined that the opposite is true, and that stocks should be held in retirement accounts (whether because of turnover or other tax inefficiency on the chosen stock investments), then it might be best to turn instead to the small-cap or emerging market stock recommendations that I so often see made.

A final word

At the end of the day, it's not necessarily wrong, per se, to suggest that a Roth should hold your "most aggressive" investments. It's just that a more nuanced recommendation should be made: Put simply, a Roth should hold the most aggressive investments within the investment category that has been deemed appropriate for tax-deferral in the first place . While that may seem a subtle distinction, in the world of tax-optimization, it's the small things that can often make huge differences over time.

Don't skip steps when deciding which investments to hold in which types of accounts. To fully tax-optimize a portfolio means understanding not just the characteristics of the accounts in question, but the characteristics of the investments, the investor, and the accounts, and how those characteristics all interact with each other.

Thoughtful tax planning in a portfolio is rarely easy, but it can yield fairly significant added benefits over a long time horizon. And in today's low-return environment, your ability to be "tax smart" could ultimately mean the difference between meeting your retirement goals and falling agonizingly short .

See also Short-Term Bond Funds Vs. Prime Money Market Fund on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}