Credit: Shutterstock photo

Credit: Shutterstock photoValue Expectations submits:

There once was a time when the "learned" believed the sun revolved around the earth, the world was flat, and government spending led to sustainable economic growth. This week's Investment Advisor Ideas focuses on another such misconceived idea, classifying stocks with growth and value designations. While the investment consultant community has firmly adopted the growth vs. value concept, at some point, hopefully in the near future, this classification will go the way of the buggy whip, leaching, and the above silly misconceptions. After all, the classification tends to imply a choice between owning a stock that can grow but doesn't offer much value, versus one that offers a compelling value but doesn't offer much growth. Such a choice is silly - every stock valuation implies a future stream of cash flows to justify its price. If today's price implies a smaller cash stream than a company is capable of generating, it is a value stock. If a stock's price implies greater cash stream than a company is capable of generating, it is a value trap, regardless of how sexy its products are or how strong its future revenue growth appears. It does not get much simpler than that.

Years ago, in 2005, I traded emails with a popular financial writer that had just criticized AutoZone ( AZO ) for failing to deliver sufficient comparable store sales growth, though the company continued on its stated path of improving margins. He appeared smart as AutoZone shares were underperforming, and carried on with his typical snarky tone in his email. I more or less let him know he was clueless and silly for not understanding wealth creation and how that translates to intrinsic value. Needless to say, he did not reference my analysis in his later article on the company and AFG failed to obtain a PR win. Our analysis was vindicated, however, as over the past 5 years AZO has moved from approximately $80 at the time to $250 today, while the S&P 500 remained flat. Worth noting, for most of the years, AutoZone's comparable store sales growth was still negative to mediocre. His (and other investors) obsession on "growth" versus "value", rather than understanding that AZO was taking the right steps to create shareholder value and the cash flow expectations embedded in its price were very reasonable caused him to miss a great trade of our day. He was fixated on AZO as a growth stock that failed to deliver "growth", rather than understanding AZO's valuation. It is often said that history repeats itself, and today's lesson may apply to many technology giants. For example, [[CSCO]] was recently crushed on weak growth numbers, but justifying its stock price requires virtually no top line growth if it can maintain its existing margin levels. As today's kiddie set often whines - Just saying....

Much like Beta as a risk proxy survived long after its "use by" date, due to its simplicity so I suspect has been and is the case for the growth vs. value classification. Instead, we would like to see stocks classified in duration terms, as companies will pursue different strategies which lead to different cash flow durations. This provides a much better framework to structure a portfolio for different phases of the economic cycle. Further, it better allows analysts to discuss stocks in terms of the operational expectations (sales growth, margins, and turns), and how they translate into future cash flows to evaluate how attractive a stock looks as an investment. At the same time, we are also mindful of reality - some investors still want traditionally defined growth and value stocks. Like golfers with stubborn hitches in our swing, we understand the need to "play through our slice" and thus prepared this list to help identify attractive "growth" and "value" stocks.

Growth vs. Value - The New Buggy Whip

Traditionally, most investors tend to identify themselves as either growth or value oriented when they approach constructing their portfolios. There are many varying approaches of how to classify stocks in either category, but growth investors typically focus on earnings and sales growth regardless of the company's ability to add value to its shareholders, whereas value investors search for stocks trading at relatively low price multiples. We believe that both approaches for picking stocks have their pitfalls if the investor fails to understand the cash flows that are driving the company's value and how they relate to its stock price. If a growth company is capable of generating larger cash stream than is implied by its current stock price, we consider it attractive. Likewise, if a low P/E company's stock price implies greater cash stream than a company is capable of generating, it is a value trap. Below we have provided a list of stocks which we consider attractive right now in both the "value" and "growth" universes, to help investors from both groups identify investment opportunities.

But first let's examine the past performance of growth vs. value stocks. We looked at many past studies comparing the performance of the two groups and although the approaches to differentiate one from the other may vary, most studies tend to show that value stocks have outperformed their growth brethren over the long haul, even when taking into account the high growth technology led stock markets of the 1990's, just prior to the tech bubble. The chart below is a study by Fama & French (via thedividendguyblog.com), comparing the value of a one-dollar investment back in 1927, based on size and growth/value characteristics. This study confirms that value stocks did earn far greater returns than the growth stocks regardless of the size classification.

As mentioned before, there are many different methods investors use to separate growth and value universes - here are some of the most common characteristics for the two groups:

Growth companies tend to have...

- High earnings growth rate

- High sales growth rate

- High R.O.E

- High profit margin

- No or low dividend yield

Value Companies tend to have...

- Low P/E ratio

- Low price/sales ratio

- Low price/cash flow

- Low price/book ratio

- High dividend yield

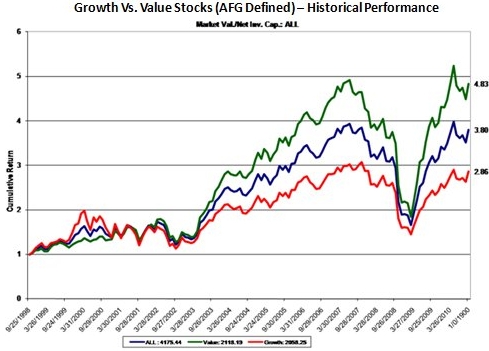

At AFG we have developed our own methodology of classifying the companies within a certain universe as value and growth - we use their relative Market Value/Net Invested Capital ratio. Companies with MV/IC greater than the median for the group are considered "growth", and those lower than the median are considered "value" stocks. The following chart provides some insight into how growth has fared relative to value stocks in the past based on AFG's classification. As you can see, in line with what we have already found out, AFG defined value stocks have outpaced growth stocks over the past 12 years.

click to enlarge

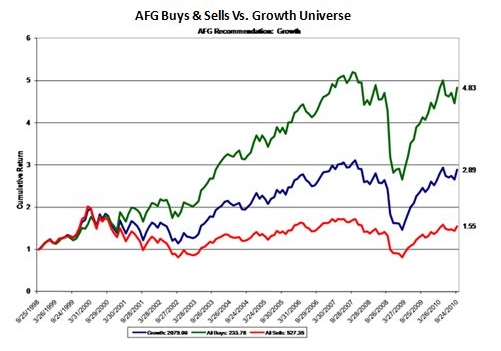

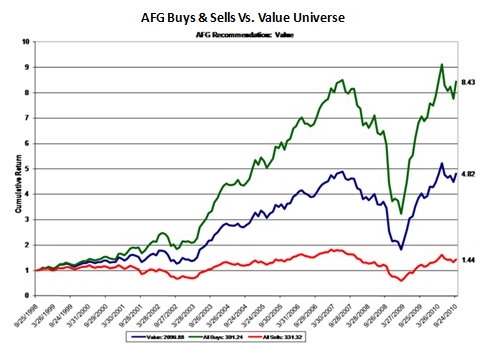

In addition, we wanted to shine some light on how our buy and sell recommendations have done within each group. The chart below demonstrates that there is a significant positive spread between the returns of the companies we find attractive and those we recommend to stay away from in each style category.

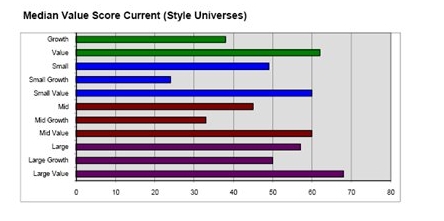

Now that we have viewed the past performance, let's look at our outlook of the attractiveness of each investment style going forward using our EM framework and valuation metrics. Based on current valuation attractiveness within our default valuation model, value looks more attractive as an investment opportunity than growth in any size category (small, mid, large), with the large cap value bucket looking the most attractive of the bunch.

In an ideal world, our portfolios would be filled with stocks with booming earnings growth and discounted price tags, however in reality any solid growth stories will attract investors, which inflate the price. We recommend not to automatically ignore companies based on style as there are plenty of attractive opportunities in both the growth and value universes, especially when utilizing AFG's research and valuation techniques to identify attractive long and short prospects. By not overlooking companies based on style you will increase the size of your fishing pond and your portfolio will benefit from the diversification.

In the table below, you will find a list of companies in both styles (based on MV/IC) that look attractive going forward. When creating our list of Attractive Growth/Value stocks we looked for companies that fit the following criteria:

- Attractive valuations

- Profitable from an economic standpoint

- Expected to improve economic profitability

- Poised to outperform

Disclosure

See also Do Patents Hold Promise for OPTi's Future? on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}