Credit: Shutterstock photo

Credit: Shutterstock photoBy Fabian Renauer :

General:

Express Scripts ( ESRX ) is the largest PBM with around a 30% market share, processing 1.5 times as many claims as its nearest competitor, CVS Caremark ( CVS ). Due to its size and the number of people it represents (~155M covered lives), ESRX has become systemic to the pharmacy/drug manufacturer system (not unlike Visa/ MasterCard in the payments industry), meaning it has substantial negotiating power and you cannot get rid of it.

Retention Rates and Business Model:

ESRX serves large companies and health plans. Upon signing on new clients, it takes around 1 year for the integration costs to pay for themselves, after which the client represents little marginal cost, making it a very profitable, annuity-like payments stream. Since PBM contracts are only around 3-4 years in duration (every year, ~25% of ESRX's business is up for renewal), the important aspect of the business is high retention rates. ESI and Medco have long had very strong retention rates in the mid to high nineties and ESRX had a 94% retention rate in 2012 with 2013 looking even better to date. In general, high PBM retention rates stem from the fact that offerings from different PBMs - in one way or another - lead to similar cost savings for plan sponsors, yet plan sponsors face high switching costs if they want to change PBMs upon contract expiry which almost always offsets any cost savings offered by competing PBMs.

PBMs can arrive at the same cost savings for plan sponsors through different ways. At one end of the continuum are PBMs that compete solely by offering high drug discounts which means these PBMs sacrifice their own margins to be competitive (i.e. passing on more of the manufacturer rebates and pharmacy reimbursement spread), while PBMs on the other extreme offer competitive prices (not as low) and provide additional programs/ services to lower the overall plan cost to a similar level (e.g. adherence programs, contacting doctors to switch prescriptions from branded drugs to generics etc.). ESRX operates based on the latter structure (Mr. Paz, ESRX's CEO, is known for saying "I get mad at my team if they want to compete on price") and offers many ancillary services to lower drug costs.

Due to ESRX's large size, these programs are far cheaper (as their cost is spread over many plan sponsors) than providing plain discounts, enabling it to have higher margins on its business. Clearly, price cutting is far easier than implementing and executing these programs successfully, however, discounts alone are the short sighted view. ESRX achieves approximately a 65% response rate when contacting doctors vs. a 15-22% industry standard (response rate = contacting doctors about cost-saving steps such as getting them to switch specific drug prescriptions from branded drugs to generics).

Economies of Scale and Rates of Return:

ESRX has strong economies of scale as PBMs' SG&A and CapEx tend to stay fairly constant within a wide relevant range. Under Mr. Paz, ESI has always been very cost efficient in terms of SG&A and CapEx, even when it was still slightly smaller than Medco and CVS. 2012 saw a year of unnaturally high SG&A as a percentage of GP for ESRX due to merger integration costs (switching ESI clients to Medco platform etc.) which will normalize in 2013+, yet it still beat its major competitor CVS and fast-growing Catamaran ( CTRX ).

Pharmacy benefit management is a very non-capital intensive business which, along with ESRX's high retention rates and cost efficiency, causes it to have strong returns on equity and tangible assets. ESRX is far more efficient at deploying its capital/ assets than its major competitors and, due to its cost efficiency and cost cutting programs, turns far more of its revenue into FCF.

The important aspect of the Medco acquisition is that ESRX combines the best programs and platforms of ESI and Medco (TRCs, Consumerology, RationalMed), which ESRX can use to lower drug costs for plan sponsors in a margin preserving way, as well as combining both companies' large positions in the lucrative specialty and mail-order pharmacy businesses with the result of having a market dominating ~25-30% specialty market share and ~60% mail-order market share.

Future Growth:

Specialty:

Specialty drugs drive annual drug cost inflation as they are complex drugs/ treatments that are expensive to create and target very specific diseases affecting only a small percentage of the population. Specialty drugs represent around 1% of prescription drug purchases yet make up ~24.5% of annual prescription drug costs (2012). By 2015, specialty drugs are expected to grow to 50% of prescription drug costs, a yearly cost increase of 18.5%.

While specialty drugs aren't as high-margin for PBMs as generic drugs, they carry a far greater price tag and rake in a large net dollar amount - an interesting example of this is H.P. Acthar Gel (specialty drug for severe epilepsy) for which ESRX got an exclusive distribution arrangement after which it raised its price from $1,600 to $23,000 . Specialty drug manufacturers tend to arrange exclusive distribution agreements with a single PBM if these drugs are highly complex, to ensure that they can better monitor their distribution and ensure that the people actually distributing the drugs have received proper training (otherwise they get pressure from the FDA). ESRX, due to its strong position in the specialty market and its large patient reach, is poised to benefit from that fact as it's the perfect partner for exclusivity arrangements (specialty represents 15-20% of ESRX's revenue).

Patent Cliff:

2011 and 2012 have seen expirations of blockbuster drug patents (e.g. Lipitor) which will continue at a significant level until 2016, with patents aggregating (cumulatively) $176B in sales dollars expiring between 2013 and 2016. PBMs' generic drug margins are almost four times as high as their branded drug margins and branded drug sales represent 18-20% of ESRX's revenues wherefore this represents a tremendous growth opportunity for ESRX.

Aging Population:

The PBM industry will be positively affected by the changing demographics as Baby Boomers are getting older. What is important in this regard is that, while the average PBM member fills 10-15 prescriptions per year, people over the age of 65 fill more than 40 prescriptions per year (3-4 times more). The U.S. bureau of the Census expects the population of U.S. citizens 65+ to increase by 14M (35%) between 2010 and 2020, increasing from 13% to 16% of the population. This will affect ESRX indirectly through its health plan clients and directly through its MA-PD plans.

Health Exchanges :

ObamaCare will see around 30M uninsured U.S. citizens enter the market through health exchanges in late 2013 and the beginning of 2014. ESRX is well represented through its health plan clients as well as its own MA-PD in 40 states which are estimated to receive ~90% of new lives.

Other:

Healthcare costs and prescription volume will continue to grow for the simple reasons of growing obesity among Americans (currently around 1/3 of Americans are diagnosed as obese) and the growth in chronic conditions and terminal illnesses which require people to continue to use drugs/ therapies for the rest of their lives. This reminds of Warren Buffett's Gillette argument that hundreds of millions of men need to shave every morning and it's not going to get any less - these people definitely cannot go off their medications and the influx will continue to outpace mortality rates (we get better and better at saving and prolonging lives).

Concerns:

- ESRX currently has ~$14.5B in long-term debt. ESRX uses the debt/ EBITDA metric with a 1-to-2 times range to determine the amount of debt it is willing to carry. ESRX is currently at 3.11x debt/ EBITDA, meaning it will be retiring debt in the range of $5B to $6B over the next two years which is a lot of money relative to ESRX's FCF that does not go to value creating uses for shareholders. On the positive side, only $2.63B of that debt is variable rate, so each 100 bps increase in interest rates would only reduce FCF by ~0.4% (using after-tax interest expense). Also, by repaying debt now, ESRX won't be forced to refinance debt at higher interest rates in the future once rates rise.

- Industry consolidation: It will be difficult for ESRX to make any other major acquisitions given its current size and the long antitrust hearings (8 months) it had to go through for the ESI Medco merger. Meanwhile, the industry is consolidating with players like Catamaran growing very fast. However, despite this consolidation, the competitive landscape won't undergo a 180 degree turn as even right now any of the top 10 PBMs can serve a Fortune 50 company. The name of the game is high retention rates and making significant margins on contracts, both of which ESRX already does.

Valuation:

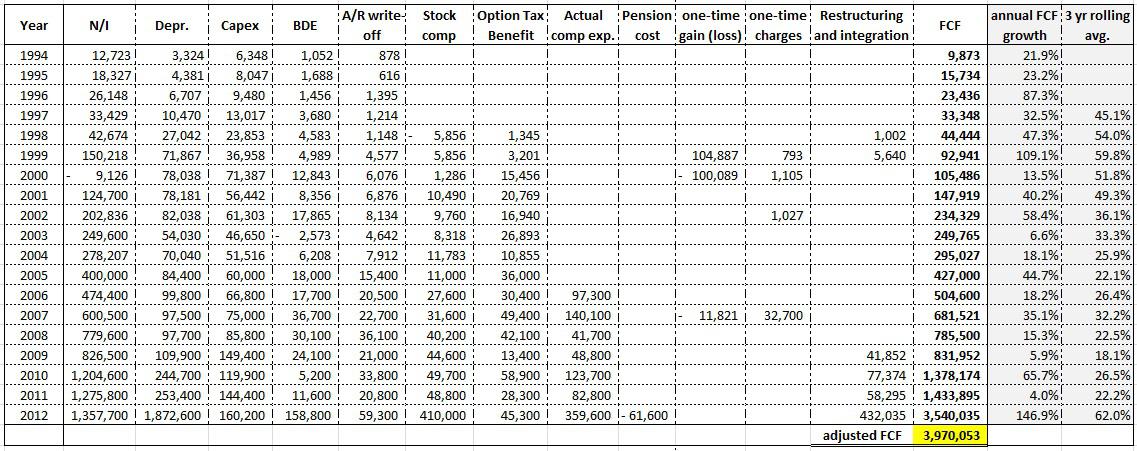

click to enlarge image

* Numbers in thousands

**BDE = Bad debt expense

*** Stock comp. = Black Scholes compensation expense added back on CFS. Stock comp is added back in the FCF analysis and replaced with a different estimate of compensation expense, namely 'Actual comp. exp.'

**** Actual comp. exp. = approximation of actual stock comp. cost [calculation: average price per share*shares issued - proceeds from stock comp. Avg. price per share estimated through treasury repurchase costs]

*****Stock comp and Option Tax Benefit aren't included in FCF calculation pre 2006 because Actual comp. expense couldn't be estimated

******One-time gains/ (losses) were subtracted/ (added back). One-time charges were added back. Restructuring costs were added back.

---------

ESRX's normalized 2012 FCF is ~$4B adjusted for merger integration costs, assuming similar CapEx as in 2012 and a conservative 27% SG&A as a % of GP (conservative as it should eventually fall below ESI's 2010/ 2011 SG&A as a % of GP due to ESRX's increase in scale and significant SG&A overlap).

Based on the normalized 2012 FCF, ESRX is selling at around 12-13 times FCF, implying an equity yield of 7.5-8.5%. Using the normalized FCF and assuming continued 5-6% FCF growth over the next five years (based on 2011's 4% growth rate as it was a non-acquisition year, plus a conservative 1-2% for the increasing patent expirations and other mentioned growth factors*) suggests a 12.5-14.5% CAGR in ESRX's share price.

*It is very difficult to identify a reasonable FCF growth range for the growth factors mentioned above wherefore the growth could come in far stronger than the estimated 1-2%.

Conclusion:

ESRX is the most efficient player in the PBM industry with the strongest management/ utilization programs in place. It will benefit strongly from future industry growth, especially due to its dominance in the specialty industry, high retention rates and a strong FCF margin. At 12-13 times FCF and given the expected industry growth, it is lucratively priced with an expected 12.5-14.5% CAGR.

------------

Additionalresearch notesfrom Subcommittee hearing on ESI - Medco merger:

- Mail pharmacy is basically a duopoly. ESRX has a market-leading ~60% mail-order market share. CVS Caremark is second largest with 24% and the third largest player only has 3%.

- Specialty is very concentrated. ESRX has a leading market share of ~30%, ahead of CVS and WAG which are the second largest at 15% each (top 3 control ~60% of specialty).

- The top 3 PBMs (Medco, ESI, CVS) were the go-to choice for 84% of the Fortune 50 in 2012. While other PBMs within the top 10 do have the capacity to provide services to Fortune 50-size companies, most of these companies prefer to take the safe route with what is now the top 2 (ESRX, Medco). In its bidding process, Ohio State University received competitive bids from smaller PBMs but decided to go with ESI because they felt more comfortable with ESI's larger, stronger infrastructure.

- Very large players such as CalPERS can only be served by ESRX or CVS.

- Medco lost 13% of its revenues (not including the UnitedHealth contract) in 2012 due to uncertainties regarding the merger as clients thought ESRX would significantly raise prices upon consummation. Retention rates have normalized again in the mid to high nineties as prices weren't raised.

- No company other than Shopko wanted to testify against ESI and Medco at the Subcommittee hearing out of fear for retaliation. This illustrates the amount to which large companies depend on the top 2 as they couldn't risk upsetting one of them.

Disclosure: I am long [[ESRX]]. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

See also LRR Energy CEO Discusses Q2 2013 Results - Earnings Call Transcript on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}