Credit: Shutterstock photo

Credit: Shutterstock photoBy Wexboy :

So ever since Denis O'Brien started popping up at regular intervals on CNBC and Bloomberg, maybe eighteen months ago now, I knew in my gut he had a whopping great IPO in the works... Fast-forward, and Digicel's now billed as the largest 'Irish' IPO ever , a revised F-1/A was just filed with an indicative $13-$16 per share price range, and its New York Stock Exchange IPO is just about ready to drop. With everybody and their mother talking about it, how can I resist chipping in my two cents..?!

Let's kick off with an introduction: Digicel Group (Pending:[[DCEL]]) is a leading provider of mobile communication services in the Caribbean and South Pacific regions. Its mobile subscriber base has grown from just 0.4 million in 2002 to a total of 13.6 million subscribers as of June-2015 (an impressive 31.7% Compound Annual Growth Rate). It now enjoys a number one position in 21 of the 31 markets in which it operates.

The company's now beginning to evolve from a pure telecom company into a total communications and entertainment provider - that is, the triple play of Phone, Cable TV, and Broadband (it has a $0.4 billion acquisition spree lined up accordingly).

Here's the actual Digicel roadshow presentation - it's well worth watching - and final pricing's expected October-7th. In total, 124 million Class A shares are being offered, plus a 30 day underwriters' option to purchase an additional 18.6 million shares. It's also a primary IPO (with a 180 day lock-up), so Digicel expects to raise somewhere between $1.6 and $2.3 billion of cash (gross, based on the price range) - with $1.3 billion earmarked for debt repayment/refinancing.

Denis O'Brien (Founder and Chairman) will retain an equity stake in the range of 58% to 61%, which could be worth up to $3.1 billion. But apparently this majority control isn't enough for him...Digicel will boast a dual-class share structure . [He'll own 193 million Class B shares, which possess 10 times the votes of A shares. Which means 'O'Brien will be chairman, and king' ]. This structure used to be quite rare (and confined mostly to family-run and media companies), but has enjoyed an unfortunate resurgence in the past 5-10 years with scarcely a mutter of investor protest, particularly in the tech and (social) media sectors. And even today, the same old chestnut's being trotted out claiming this (somehow) protects the self-interest of the company and shareholders. But when you realize O'Brien will control (up to) 94% of the voting power, and you consider the long list of related-party disclosures in the prospectus, it's only natural to question where the real self-interest lies...

And the list of O'Brien affiliated/controlled companies which have been/will be involved with Digicel really is quite exhausting: Communicorp receives various/minor fees. AC Executive Aviation Services received $27 million in the past 3 years for the use of an airplane, while Sierra Support Services received $68 million in the past 15 months for the installation of a fiber optic network. And Island Capital's entitled to a 0.5% advisory services fee for all transactions such as tender offers, acquisitions, sales, mergers, financings, and even the Digicel IPO itself (!?) - in the past 3 years, it's collected $29 million.

But what's even more extraordinary are the deals which arguably impact Digicel's own financial stability, strategy, and competitive position. Like its (effective) 45% minority position in Digicel Holdings (Central America) Limited ('DHCAL'), which is controlled by O'Brien and provides cellular services in Panama - despite continued losses and a write-off of its equity investment (in 2011), Digicel has continued to fund DHCAL with another $119 million (in interest-free cash loans) in the past 3 years, with an additional $23 million of loans in just the latest quarter. Plus it guarantees another $64 million of DHCAL's external borrowings! The company's also granted a waiver whereby directors will not be prohibited from operating or investing in competing businesses. Not to mention Denis O'Brien actually owns (and may use) the Digicel brand name in certain parts of the world!? But most of all, we can't escape the elephant in the room...the $1.1 billion of dividends paid out to O'Brien over the past 3 years, which leaves the company with a daunting $6.5 billion of debt outstanding. What are the potential implications of such deals for Digicel and its new/minority shareholders, both now and in the future?

But that's a question each prospective shareholder must ask for themselves...

So for now, I'll focus on Digicel's valuation, and take what might be considered a pretty singular approach - which shouldn't surprise regular readers of mine - as all investors must (regularly) do anyway, if they ever hope to stand apart from the crowd and the index. Analysts will bore you to death with peer/sector valuations, metrics, and comparisons...but I'm only going to evaluate Digicel versus a single company:

MTN Group (formerly M-Cell) ( MTNOY )

[NB: I'll be referencing their most recent interim and annual results below.]

MTN's actually an African and Middle Eastern mobile communications company - here's a recent profile . It enjoys a number one position in 15 of the 22 markets in which it now operates.

It also boasts a rather astonishing 231 million subscribers - um, except they're actually in places like Nigeria, Iran, South Africa, and Ghana! So one might obviously ask, how on earth does MTN compare with Digicel? Or have I simply lost the plot?! Well actually, no...

There's a very specific logic to this peer comparison, and it's a great reminder of the sheer chutzpah of Digicel's investment bankers. Or maybe the credit belongs to O'Brien himself - after all, Denis is much smarter than he looks, and he definitely has a brass neck on him...

Because launching an IPO in NYC is sheer genius. Digicel will inevitably garner a higher valuation versus what it might achieve in Dublin and/or London, with US analysts and investors tending to automatically assign it a valuation in line with other US-listed peers. And even if a couple of them actually notice its Caribbean subscriber base, they'll fondly remember sipping cocktails on their honeymoon in lovely safe (and very dull) Aruba, and feel suitably reassured about Digicel's story and investment proposition...

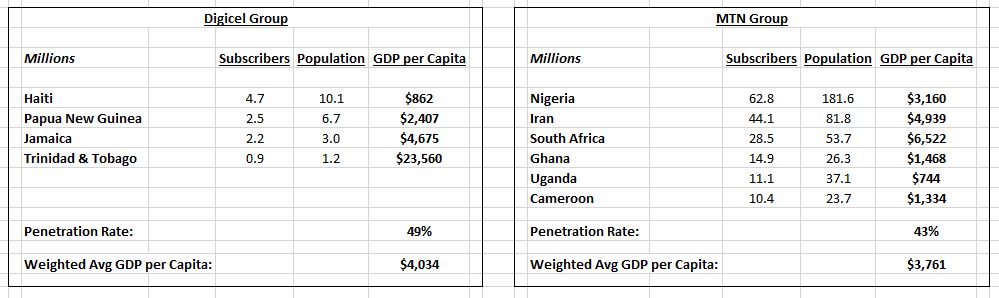

Whereas for the average American, countries like Nigeria, Iran, and Ghana probably seem like dangerous unstable poverty-stricken hell-holes to be avoided at all costs. Except, in reality, they'd probably think the same if they took the time to drill down and survey Digicel's actual subscriber base...in countries like Haiti, Papua New Guinea, and Jamaica! I mean, when has Haiti ever been noted for its wealth, or its stability? And doesn't PNG still have cannibals lurking in its jungles? [Though if they're up for buying smartphones these days, maybe now they just order takeaway..?!] Let's see what the numbers say:

[NB: i) GDP per Capita is calculated (per the Digicel prospectus) as GDP (official exchange rate) divided by population. Minor differences are due to CIA World Fact Book updates - except for Jamaican GDP per Capita, where I'd actually dispute the data in the prospectus. And ii) both tables cover about 75% of each company's subscribers - for simplicity, I'll assume this is representative of their overall subscriber bases.]

Just look how similar their respective penetration rates (49% versus 43%), and their Weighted Average GDP per Capitas ($4K versus $3.8K), actually are...these companies might as well be twins! Except Digicel manages to wring almost quadruple the monthly ARPU (Average Revenue per User of $14.30, per its latest quarterly results) from its subscriber base - despite similar income levels - versus MTN's monthly $3.65 ARPU. [Derived from its latest interim revenue/average subscriber base, and translated using the latest 13.9152 $/ZAR rate]. For O'Brien, this has obviously been a fantastic achievement to date...but arguably, at this point, MTN appears to have far more upside potential in terms of ARPU. And sub-Saharan Africa's still set to be one of the fastest-growing regions in the world, with the IMF expecting it to expand 4.4% in 2015, not much lower than its 5.4% pa average over the last decade...a powerful tail-wind for MTN.

Let's see how the two companies rank financially:

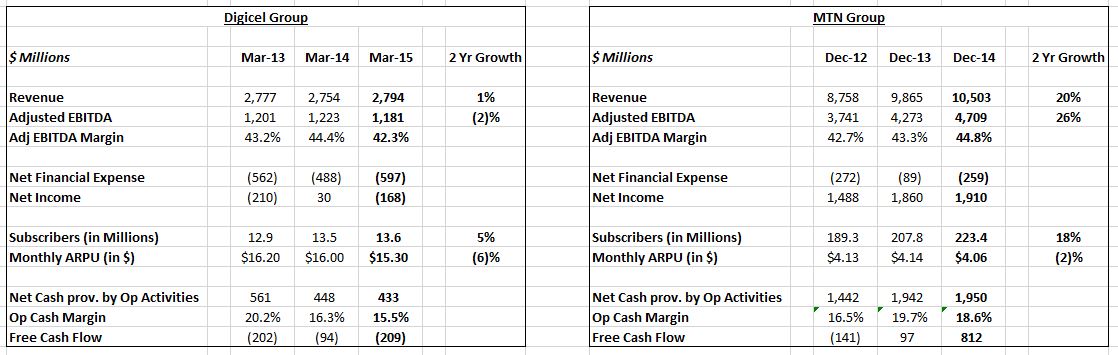

[NB: Again, for simplicity, I'm using data from each company's last 3 financial years - subsequent quarterly/interim results confirm no huge change in terms of revenue/subscribers. For comparability, I've converted MTN's financials across the board at the latest 13.9152 $/ZAR rate...worth noting the rand's lost nearly two thirds of its value since end-2012, and is now trading at all-time lows.]

Yup, that's a horribly unflattering comparison...

In what universe could Digicel justifiably claim to be the better company!? Over the past 2 years, Digicel's minimal 5% subscriber growth was offset by declining ARPU, leaving revenue basically flat - while MTN's 18% subscriber growth powered a 20% increase in revenue (at least in ZAR terms). Adjusted EBITDA margins are relatively similar, but Digicel's drowning in debt and can barely manage two times EBITDA coverage (versus net financial expense), whereas MTN boasts a cumulative 26% EBITDA increase, and is clearly under-levered with a massive 18 times coverage ratio. Of course, Digicel's interest burden is a primary driver of its cumulative losses - a huge contrast to MTN, which has consistently converted 40%+ of its EBITDA margins into steadily increasing net income (a cumulative $5.3 billion in the last 3 years).

And cash flow provides no relief either - with Digicel's net cash from operations (and operating cash margin) declining each year, and cumulative free cash flow negative to the tune of $(0.5) billion. Whereas MTN enjoyed rapidly increasing free cash flow, reporting over $0.8 billion FCF generation last year. [High capex is obviously an ongoing feature of the industry. In light of current prospects, and the constant cycle of required infrastructure upgrades and investment to date, any attempt(s) to identify and exclude specific capex as long term 'discretionary' investment looks foolish to me...]

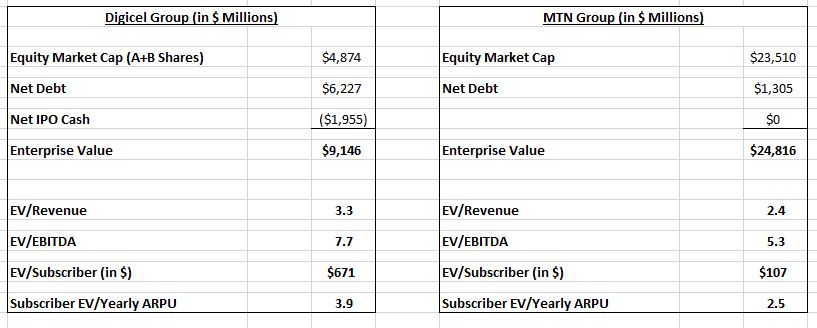

Bearing all that in mind, let's compare respective valuations. For MTN, we'll use the latest market price of ZAR 179.51 per share, a subscriber base of 231 million, $3.65 monthly ARPU, and net debt of $1.3 billion. For Digicel, let's assume a $14.50 IPO price (mid-point of price range) and an exercise of the underwriters' option (as per usual) to purchase 18.6 million shares, a 13.6 million subscriber base, $14.30 monthly ARPU, and net debt of $6.2 billion:

[NB: You'll see Enterprise Value /Subscriber regularly quoted as a ratio, but obviously it's totally dependent on actual ARPU, so Subscriber EV/Yearly ARPU is a more relevant ratio on which to focus.]

No matter if it's EV/Revenue, EV/EBITDA, or Subscriber EV/Yearly ARPU, Digicel's at a premium across the board - in fact, based on an indicative $9.1 billion EV, it's actually being priced at an average near-50% premium to MTN. Just take another look at the tables - again, in terms of revenue, profitability, cash flow, financial (in)stability, or even its subscriber base, there's nothing to suggest Digicel deserves any kind of premium versus MTN. And if you believe otherwise, please call me ASAP...I have a wildly over-priced bridge IPO I want to sell you!

So, what does a sensible Digicel valuation look like? Now there's a question... And in terms of absolute valuation, how would you even go about it?

When we're actually talking about a loss-making/over-indebted company with flat revenues, a relatively static subscriber base, falling ARPU, declining operating cash flows, and consistently negative free cash flow..?!

You could end up going around in circles for hours figuring out/debating such a valuation. And regardless, no matter how large or small the valuation, I can't help but think we're ultimately talking about a share that looks suspiciously like an equity stub to me. In the end, relative valuation is frankly the best/most suitable compromise here...I think it's more than fair if we actually price Digicel in line with MTN's current valuation. [And to also ensure such a valuation's conservatively anchored, we should note MTN's currently trading on a 12.3 P/E (based on FY-14 net income), which looks pretty reasonable to me]:

But do I really see Digicel gravitating to a $5.70 share price in due course?

No, probably not...the outcome will probably far more binary than that. All things considered, at this point in time, I suspect there's no happy medium for the sector (or Digicel) in terms of strategy. I see only two choices really: i) Cash Machine - to maximise revenue/ARPU, retain subscribers, increase margins, conserve cash, and focus on debt pay-down and dividends, or ii) Growth Machine - to pursue hell for leather growth in revenue, services, and subscribers, potentially sacrificing margin, and using cash flow/debt (and perhaps additional equity issuance) to fund the required capex and acquisitions.

I'm presuming (correctly, I believe) that Denis O'Brien and Digicel are opting for a Growth Machine strategy. Which clearly presents attractive long term opportunities, but also substantial risks - not least of which is the company's over-indebtedness (despite any expected use of net IPO proceeds), cumulative net losses, negative free cash flow, poor governance and related-party deals, and possible equity dilution to come. Not to mention potentially adverse regulation & competition...

In effect, my $5.70 Fair Value per share estimate is also an expected value estimate for the range of favourable and/or unfavourable outcomes the Digicel business and share price might actually experience over the near/medium term horizon - as determined by the strategy management chooses to pursue, and the progress and results it manages to deliver...

See also Premarket Biotech Digest: Breast Cancer Therapies, Anavex's Milestone, Praluent EU Approval on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}