Credit:

Credit: By Eiad Asbahi :

We believe Ambarella, Inc. ( AMBA ) will miss the Street's FQ3'14 consensus estimates, resulting in downward revisions to FY'14 and FY'15 estimates. Our channel checks with Ambarella's largest customer Chicony, checks within AMBA's supply chain, and conversations with various analysts indicate that AMBA's fastest growing business segment, selling SoCs to be embedded in GoPro wearable cameras, has significantly weakened.

Based on conversations with the sell-side, current Street estimates for 20% QoQ revenue growth in FQ3'14 are based on extrapolation of FQ3'13 results; FQ3'13 was a boom time for AMBA on the back of a successful GoPro Hero3 product launch. Revenue from GoPro wearable camera SoCs have grown from 4% to 42% of AMBA's consolidated sales in the year spanning FQ1'13 to FQ1'14. Our research, however, indicates that growth in Hero3 sales is currently dwindling and that a GoPro Hero3 refresh cycle will not take place in 2H'2013. While we do expect AMBA's non-GoPro revenue to grow, it is unlikely to provide the kind of growth needed to offset the potential revenue shortfall from the GoPro-related business. Against the backdrop of AMBA's non-GoPro revenue having grown between -25% and +19% QoQ (and actually declining sequentially in three out of the four quarters), current Street estimates appear unachievable.

While AMBA is well positioned in several growing markets, and we like its business for the long term, it has a customer concentration issue. Once a top- or bottom-line miss occurs, fears surrounding the opacity of its end markets, its high customer concentration and the elevated risk of end product cycle delay are likely to reemerge, with the company's multiple contracting toward levels last seen at its 2012 IPO, or 10x EPS.

AMBA currently trades at LTM and forward P/E multiples of 22x and 14x. We believe the stock has an intrinsic worth of $11.40 per share, or 12x our FY15 EPS estimate, indicating 25% downside from current levels.

Business Overview

We began analyzing AMBA as a potential long because we believe it to have an attractive competitive position as a fabless semiconductor manufacturer serving high-growth, niche end markets. The company was founded in 2004 by a group of industry veterans with extensive experience building video processing and encoding semiconductors. It is a leading developer of low-power, high-definition video compression and image processing semiconductors. The company's products are used in a variety of high definition cameras, including security IP-cameras, wearable sports cameras, and automotive video recorders. Ambarella technology is also used in television broadcasting infrastructure systems with video content encoded and transmitted to audiences around the world.

Although the company does not provide a revenue breakdown of sales into its various end markets, the chart below contains our estimates of its FQ1'14 (fiscal quarter ending in April 30, 2013) revenue split based on data from past earnings calls and company filings.

AMBA's wearable camera segment is its largest revenue contributor, making up 42% of consolidated revenue. Almost all of this revenue is generated from the sale of chips embedded into wearable cameras produced by private company GoPro. GoPro camera sales have more than doubled every year since debuting in 2004, and its units are estimated to have accounted for 21.5% of digital camcorder shipments nationwide in the first half of 2012. GoPro's current Hero3 sports camera line was launched in November 2012, and the current flagship model Hero3 Black Edition is powered by AMBA's A7 SoC.

AMBA's primary customer Chicony Electronics Co., Ltd. is the original design manufacturer, or ODM, for GoPro's cameras. Chicony buys AMBA's chips and assembles them into GoPro's cameras.

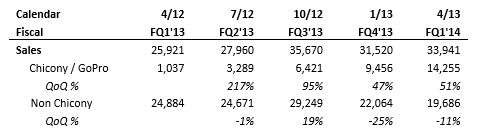

In the figures below, we estimate the amount of AMBA revenue that is the direct result of GoPro Hero3 camera sales (based off AMBA's sales to ODM Chicony), and observe a strong and steady ramp over the past five quarters. AMBA's GoPro-related revenue grew from 4% to 42% of consolidated sales in the year spanning FQ1'13 to FQ1'14.

While revenue contribution from GoPro Hero3-related sales has exhibited rapid growth, non-GoPro Hero3 revenue has been relatively stagnant. In fact, non-GoPro related revenue declined sequentially in three out of the four most recent quarters and grew between -25% to +19% QoQ. In its strongest showing (FQ3'13), this revenue stream grew 18% sequentially.

Channel Checks Indicate GoPro Camera Sales Growth in Decline, AMBA to Miss Street Estimates

Based on our channel checks, we believe that while AMBA has the potential to meet the Street's FQ2'14 consensus estimates, it will miss on FQ3'14 (fiscal quarter ending October 31, 2013) and FY'2014 (fiscal year ending January 31, 2014) estimates. FQ2'14 consensus estimate assumes AMBA's revenue will come in at the midpoint of management guidance, implying QoQ revenue growth of 6% to $35.9 million. Street expectations for FQ3'14 (quarter ending October 31, 2013) - for which AMBA has not issued guidance - assume 20% QoQ revenue growth; we believe this expectation is unachievable and that downward revisions to sell-side estimates will follow AMBA's issuance of FQ3'14 guidance when it reports FQ2'14 results.

Our conversations with sell-side analysts indicate they've based their FQ3'14 estimates on simple extrapolations of previous results, but based on AMBA's very limited history this would seem misguided. Their estimates are grounded on the following assumptions:

- Steady year-over-year growth rate

- Strong seasonality, especially for the wearable camera segment

- Extrapolation of management's qualitative comments

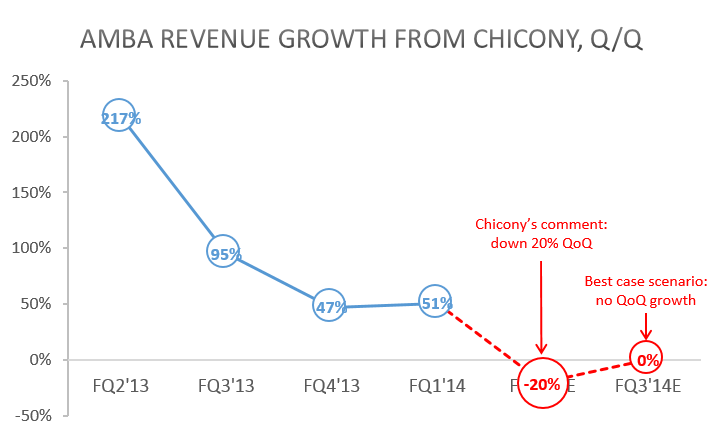

Given AMBA's high concentration of Chicony / GoPro Hero3-related revenue, it is critical GoPro sales continue to grow rapidly for AMBA to meet the FQ3'14 target (20% QoQ revenue growth); based on our channel checks, this is not happening.

Our call with GoPro ODM Chicony last week raises serious concerns regarding GoPro Hero3's sales momentum; it has slowed substantially. According to Chicony, its revenue from GoPro Hero3 peaked in CQ1'13. In CQ2'13, the GoPro revenue was down at least 20% QoQ, and in CQ3'13 GoPro revenue will be down again QoQ. Chicony attributes the sequential decline to 1) a strong product launch in Q4'12 and 2) lack of product refresh for 2013. The same data point was echoed by Citi's Chicony analyst who attended Chicony's analyst meeting Tuesday two weeks ago. At the meeting, the company guided for almost no contribution from GoPro in 2H'2013.

A possible explanation for Chicony's declining GoPro revenue is that the next GoPro product will be manufactured by another ODM, such as Foxconn, which owns 9% stake of GoPro. Chicony, however, denies this, citing that the firmware it developed for Hero3 is not easily duplicable and stating that it does not believe it has lost GoPro's business to another ODM.

Regardless of which company is chosen to manufacture the next generation of GoPro camera, Chicony's guidance implies that GoPro's Hero3 refresh cycle will not take place in 2H'2013, and that it has instead likely been pushed out to 2014. Citi's Chicony analyst has affirmed that no new GoPro product has been defined, corroborating this view. AMBA management's comments also indicate this to be the case. It is widely speculated that AMBA's next generation A9 SoC is the logical choice to power the next generation flagship GoPro camera. However, according to AMBA CEO Fermi Wang on the recent FQ1'14earnings call the A9 chip will not make it into end market products until next year: Upon being asked about the status of the A9 silicon, he responded that, "[t]hat is targeting more on the sports camera side. And we do have design wins that we're working on. Again, I think that those products will not come out until early next year." Further, our conversations with sources in Ambarella's supply chain indicate that the A9 SoC is currently in trial, but not yet in full production.

Accordingly, if we assume AMBA's GoPro Hero3 revenue remains flat in FQ3'14 (rather than assuming the 20% decline as suggested by Chicony), AMBA will need to grow its non-Chicony revenue by 33% QoQ in order to meet consensus revenue estimates. While we do expect non-Chicony revenue to grow, it is unlikely to provide the kind of growth necessary to offset the potential revenue shortfall from the GoPro-related business. Against the backdrop of AMBA's non-Chicony revenue having grown between -25% and +19% QoQ (and again, actually declining sequentially in three out of the four quarters), current Street estimates appear unachievable.

We Believe AMBA Shares have 25% Downside from Current Levels

We believe investors are likely to soon develop a greater appreciation of the lack of predictability in AMBA's quarterly growth patterns. While AMBA's three camera markets are generally growing, it is difficult to estimate the quarterly growth patterns with a great deal of accuracy. AMBA's wearable camera end market is currently dominated by business with private company GoPro, which neither discloses its sales numbers nor offers clues as to the timing of new product launches. AMBA's IP camera end market is fragmented, and concrete data pertaining to this market is hard to come by, as we discovered in conducting primary research: Even though data from third party market research firms and key vendors are directionally consistent, they vary by a large margin. AMBA's automobile camera end market, an Asian and Russian phenomenon, is equally difficult to track; the manufacturers' landscape is similar to that for white-label smartphones in China, in that there are just too many small vendors to track.

We believe that due to concerns regarding AMBA's unpredictable growth profile, investors valued the company at a modest 10x forward P/E multiple at its IPO. Since then, the company has beaten consensus estimates in three consecutive quarters, and the equity was subsequently bid up to reach a recent high of 18x EPS. We believe forgotten concerns could soon be remembered. While AMBA is well positioned in several growing markets, and we like its business, it has a customer concentration issue. Once a top- or bottom-line miss occurs, fears surrounding the opacity of its end markets, its high customer concentration and the high risk of end product cycle delay are likely to reemerge, and the company's multiple is likely to contract toward levels last seen at its IPO.

We believe AMBA is set to miss earnings expectations. The Street currently expects the company's top line to grow at 5% and 20% QoQ in FQ2'14 and FQ3'14, respectively. The data points we have gathered indicate investors will be disappointed. We expect downward revisions of FY'14 and FY'15 estimates to follow, and believe the company can generate EPS of $0.80 and $0.95 in FY'14 and FY'15, respectively (vs. current consensus estimates of $0.85 and $1.10). We believe the stock has an intrinsic worth of $11.40 per share, or 12x our FY15 EPS estimate, indicating 25% downside from current levels.

Disclosure: I am short [[AMBA]]. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

See also Duke Energy Corporation's CEO Presents at Bank of America/Merrill Lynch State of the U.S. Utilities Industry Conference (Transcript) on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}